- 1

- For interactive plots.

- 2

-

The

fable-compatible interface to Meta’s Prophet algorithm.

Prophet

1 Where We Are

Look at how far our model has come since Module 1:

| Module | What we added | Model |

|---|---|---|

| 1 | Decomposition + benchmark | STL + Drift + SNAIVE |

| 2 | Smarter trend-cycle | STL + ETS / ARIMA |

| 3.1–3.2 | External context | TSLM, dynamic regression with xreg |

| 3.3 | Harmonic regression | ARIMA + Fourier terms |

| 3.4 (now) | Automated, scalable, interpretable | Prophet |

Every previous model required us to make choices manually: how many AR terms? Which regressors? Where do the knots go?

NoteThe knot problem we left open

In Linear Regression, we saw that piecewise TSLM is sensitive to where we place the knots — different choices produce dramatically different forecasts, even with similar in-sample fit. Prophet solves this automatically.

2 What Is Prophet?

Prophet is a forecasting procedure developed by Meta (Facebook) and released as open source in 2017. It was designed for business time series — daily, weekly, and yearly data with strong seasonal effects, holidays, and shifting trends.

“Prophet is a procedure for forecasting time series data based on an additive model where non-linear trends are fit with yearly, weekly, and daily seasonality, plus holiday effects. It works best with time series that have strong seasonal effects and several seasons of historical data.”

2.1 The Prophet model

At its core, Prophet fits a decomposition model:

y(t) = g(t) + s(t) + h(t) + \varepsilon_t

- g(t) — trend: piecewise linear or logistic growth, with changepoints detected automatically.

- s(t) — seasonality: Fourier series approximating yearly, weekly, or daily patterns.

- h(t) — holidays / special events: user-supplied dummy variables with windowed effects.

- \varepsilon_t — noise: assumed i.i.d. normal.

ImportantSound familiar?

This is exactly what we’ve been building all semester — trend + seasonality + external effects. Prophet just automates the specification and fits it in a Bayesian framework using Stan.

2.2 Automatic changepoint detection

The key innovation over piecewise TSLM is automatic changepoint detection. Prophet:

- Places a large number of potential changepoints uniformly in the first

changepoint_rangeproportion of the data (default: 80%). - Uses a sparse prior (Laplace) to shrink most changepoint magnitudes to zero — only genuine structural breaks survive.

- The user can tune

n_changepoints(default 25) andchangepoint_prior_scale(flexibility of trend changes).

No more guessing where the knots go.

2.3 When to use Prophet

| Situation | Use Prophet? |

|---|---|

| Sub-daily data (hourly, daily) with multiple seasonal cycles | ✅ |

| Business data with holidays and known events | ✅ |

| Need interpretable components for stakeholders | ✅ |

| Several seasons of history available | ✅ |

| Short series (< 2 full seasonal cycles) | ❌ |

| Series with no clear trend or seasonality | ❌ |

| Need formal inference on model parameters | ❌ |

| Need prediction intervals from theory, not simulation | ⚠️ |

:::

WarningProphet is not always better than ARIMA

Prophet was designed for at-scale, analyst-friendly forecasting. On many classical monthly or quarterly economic series, a well-specified ARIMA or ETS will outperform it. Always compare on a held-out test set.

3 Setup: fable.prophet

Prophet is available in R through two packages:

prophet— the original package. Works standalone, does not integrate withfable.fable.prophet— afable-compatible wrapper by Mitchell O’Hara-Wild. Lets us use Prophet insidemodel(),forecast(),accuracy(), and all the tools we already know.

NoteDependency: Stan

fable.prophet depends on rstan and prophet. On first install, R will also install Stan and its dependencies. This can take a few minutes — plan accordingly before class.

4 Model Specification

Inside model(), Prophet is specified with the prophet() function. Like ARIMA() and ETS(), it can be fully automatic or manually specified.

Code

# Automatic — Prophet chooses everything

prophet(y)

# Manual — explicit components

prophet(y ~ growth("linear") + season("year", type = "multiplicative"))4.1 Trend: growth()

The growth() term specifies the trend model:

growth("linear")— piecewise linear trend. Best for series that grow or decline without a natural ceiling.growth("logistic")— logistic growth (S-curve). Requires acapacitycolumn in the data specifying the theoretical maximum.

Code

- 1

- Number of potential changepoints to consider (default: 25).

- 2

- Proportion of history where changepoints can occur (default: 0.8).

- 3

- Flexibility of trend changes — larger = more flexible, smaller = more rigid (default: 0.05).

4.2 Seasonality: season()

The season() term adds a Fourier-approximated seasonal pattern:

Code

- 1

- Annual seasonality — 10 Fourier pairs; additive (level of seasonality does not change with the series level).

- 2

- Weekly seasonality — 3 Fourier pairs; multiplicative (seasonality scales with the series level).

- 3

- Daily seasonality — only relevant for sub-daily data.

Tip

order = Fourier K

The order argument in season() is the same K we used in harmonic regression (fourier(K = ...)). Higher K → more flexible seasonal shape, but more parameters. Start with the default and adjust if residuals show seasonal structure.

4.3 Component summary

| Prophet component | Equivalent in previous models |

|---|---|

growth("linear") |

trend(knots = ...) in TSLM |

growth("logistic") |

— (no direct equivalent) |

season("year", type = "additive") |

season() in TSLM / SAR terms in SARIMA |

season("year", type = "multiplicative") |

Multiplicative STL seasonality |

season("year", order = K) |

fourier(K = ...) in harmonic regression |

holiday() |

Spike/shift dummies in TSLM |

| Changepoints (automatic) | trend(knots = c(...)) in TSLM — but manual |

5 Application: LAX Passengers

We’ll apply Prophet to monthly passenger counts at Los Angeles International Airport (LAX), broken down by domestic and international flights — a dataset with a clear piecewise trend, multiplicative seasonality, and a major structural break (the 2001 and 2008 shocks).

5.1 Load and prepare

Code

lax_passengers <- read.csv(

"https://raw.githubusercontent.com/mitchelloharawild/fable.prophet/master/data-raw/lax_passengers.csv"

)

lax_passengers <- lax_passengers |>

1 mutate(datetime = lubridate::mdy_hms(ReportPeriod)) |>

group_by(

month = yearmonth(datetime),

type = Domestic_International

) |>

2 summarise(passengers = sum(Passenger_Count), .groups = "drop") |>

3 as_tsibble(index = month, key = type)

lax_passengers- 1

- Parse the date-time string into a proper datetime object.

- 2

- Sum all passenger categories within each month and travel type.

- 3

-

Convert to

tsibble—type(Domestic / International) is the key variable.

5.2 Exploratory analysis

A few things to note from the plot:

- Piecewise trend: visible drops around 2001 (9/11) and 2008–2009 (financial crisis). The trend clearly changes slope at these points — this is exactly what automatic changepoint detection handles.

- Multiplicative seasonality: the seasonal swings grow proportionally with the series level, suggesting a multiplicative model.

- International < Domestic throughout, but both share a similar seasonal shape.

TipThe meme check

Spending three hours choosing knots manually vs. discovering Prophet does it for you.

5.3 Train / test split

Code

lax_train <- lax_passengers |> filter_index(~ "2017 Dec.")

lax_test <- lax_passengers |> filter_index("2018 Jan." ~ .)The test set covers 2018–2019 (24 months of out-of-sample evaluation). We intentionally stop before 2020 to avoid COVID-19 contaminating the evaluation.

5.4 Fit models

Code

- 1

- Manual Prophet: piecewise linear trend + multiplicative annual seasonality.

- 2

- Automatic Prophet: lets the algorithm decide on all components.

- 3

- Automatic ARIMA — our Module 2 benchmark.

- 4

- Automatic ETS — our other Module 2 benchmark.

- 5

- Harmonic regression: ARIMA errors + Fourier seasonality (Module 3.3).

5.5 Components

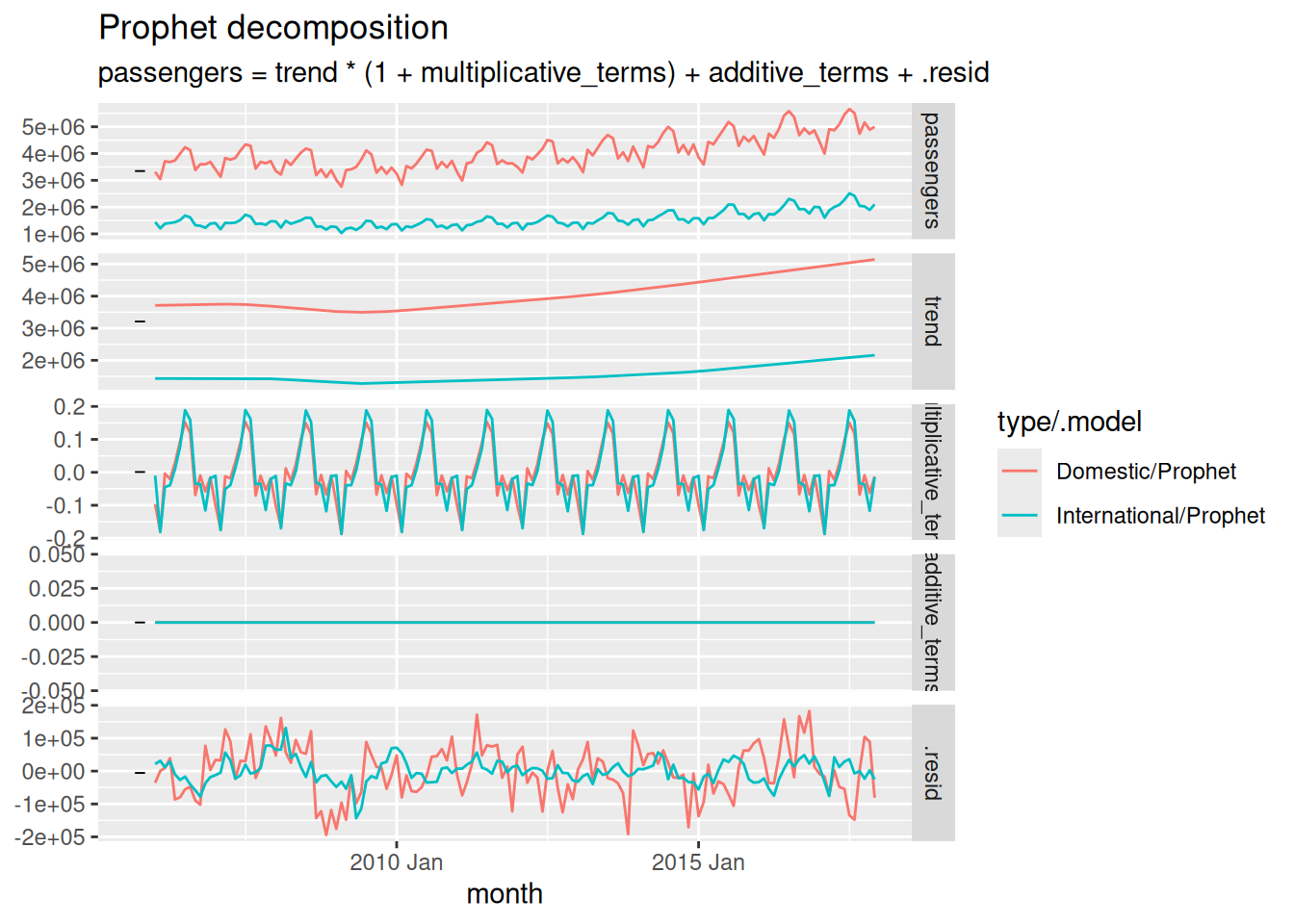

One of Prophet’s biggest advantages in practice: interpretable components that you can show to a non-technical audience.

Code

lax_fit |>

select(type, Prophet) |>

components() |>

autoplot()

The decomposition shows:

- Trend (g(t)): captures the piecewise nature of growth, including the post-2001 and post-2009 recoveries — with no manual knot placement.

- Annual (s(t)): the seasonal pattern for each series. Notice it’s being fitted as a proportion of the level (multiplicative).

- Residuals (\varepsilon_t): should look like white noise if the model is well-specified.

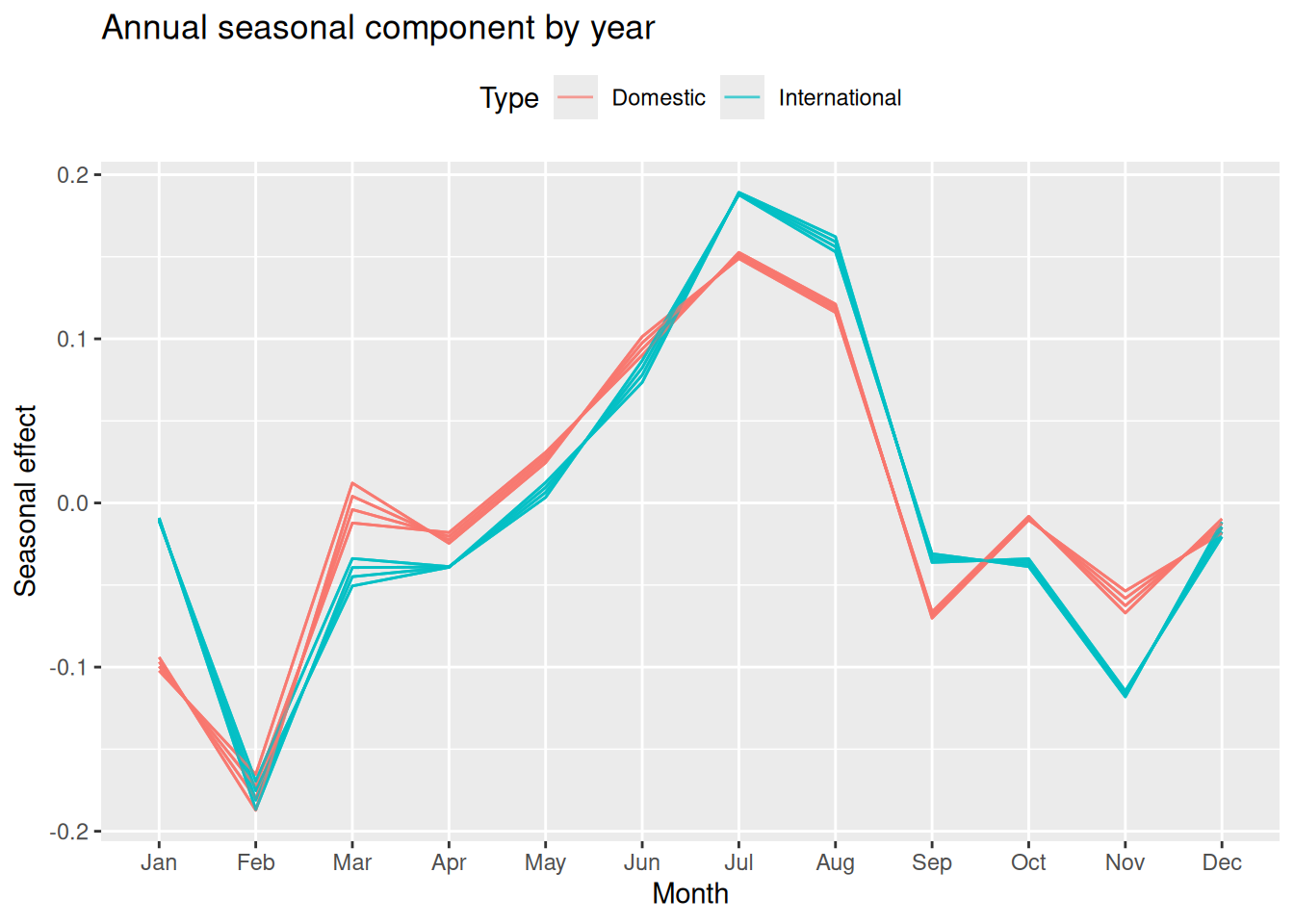

5.6 Seasonal pattern by month

We can also visualize the seasonal component overlaid by year — useful to check if the seasonal shape is stable over time:

Code

lax_fit |>

select(type, Prophet) |>

components() |>

ggplot(aes(

1 x = lubridate::month(month, label = TRUE),

2 y = year,

colour = type,

group = interaction(type, lubridate::year(month))

)) +

geom_line(alpha = 0.7) +

labs(

title = "Annual seasonal component by year",

x = "Month",

y = "Seasonal effect",

color = "Type"

) +

theme(legend.position = "top")- 1

- Extract the month name from the time index for the x-axis.

- 2

-

yearis the name of the annual seasonal component extracted bycomponents().

NoteWhat to look for

If the seasonal lines are stacked consistently, the shape is stable across years — a multiplicative model is appropriate. If lines diverge or change shape dramatically, you may need to reconsider the specification.

5.7 Forecast

Code

lax_fc <- lax_fit |>

forecast(h = "2 years")

lax_fc |>

autoplot(

lax_passengers |> filter_index("2012 Jan." ~ .),

level = 80

) +

facet_wrap(~ type, ncol = 1, scales = "free_y") +

labs(

title = "LAX passenger forecasts — 2018–2019",

y = "Passengers",

x = NULL,

color = "Model"

) +

theme(legend.position = "top")

5.8 Accuracy

Code

lax_accu <- lax_fc |>

accuracy(lax_test) |>

select(.model, type, RMSE, MAE, MAPE) |>

arrange(type, MAPE)Warning: The future dataset is incomplete, incomplete out-of-sample data will be treated as missing.

9 observations are missing between 2019 Apr and 2019 DecCode

lax_accu

WarningCheck accuracy by key

When your tsibble has a key variable (like type here), accuracy() returns one row per model per key. A model that performs best for Domestic passengers may not be best for International — always check both.

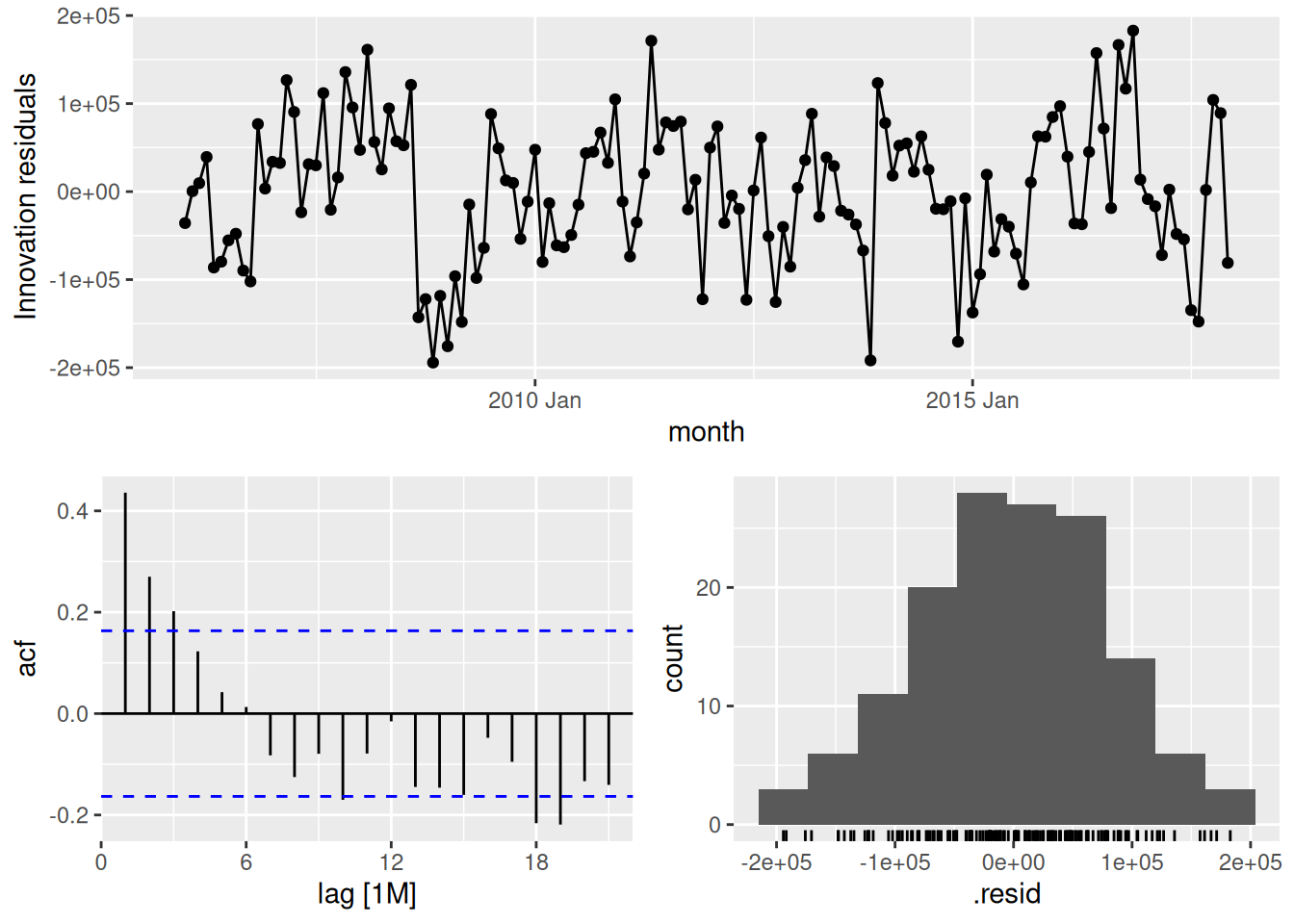

5.9 Residual diagnostics

Code

lax_fit |>

select(type, Prophet) |>

filter(type == "Domestic") |>

gg_tsresiduals()

Check:

- Residuals vs. time: should show no visible trend, seasonality, or heteroscedasticity.

- ACF: if significant spikes remain at seasonal lags, the

orderinseason()may be too low. - Histogram: roughly bell-shaped for valid prediction intervals.

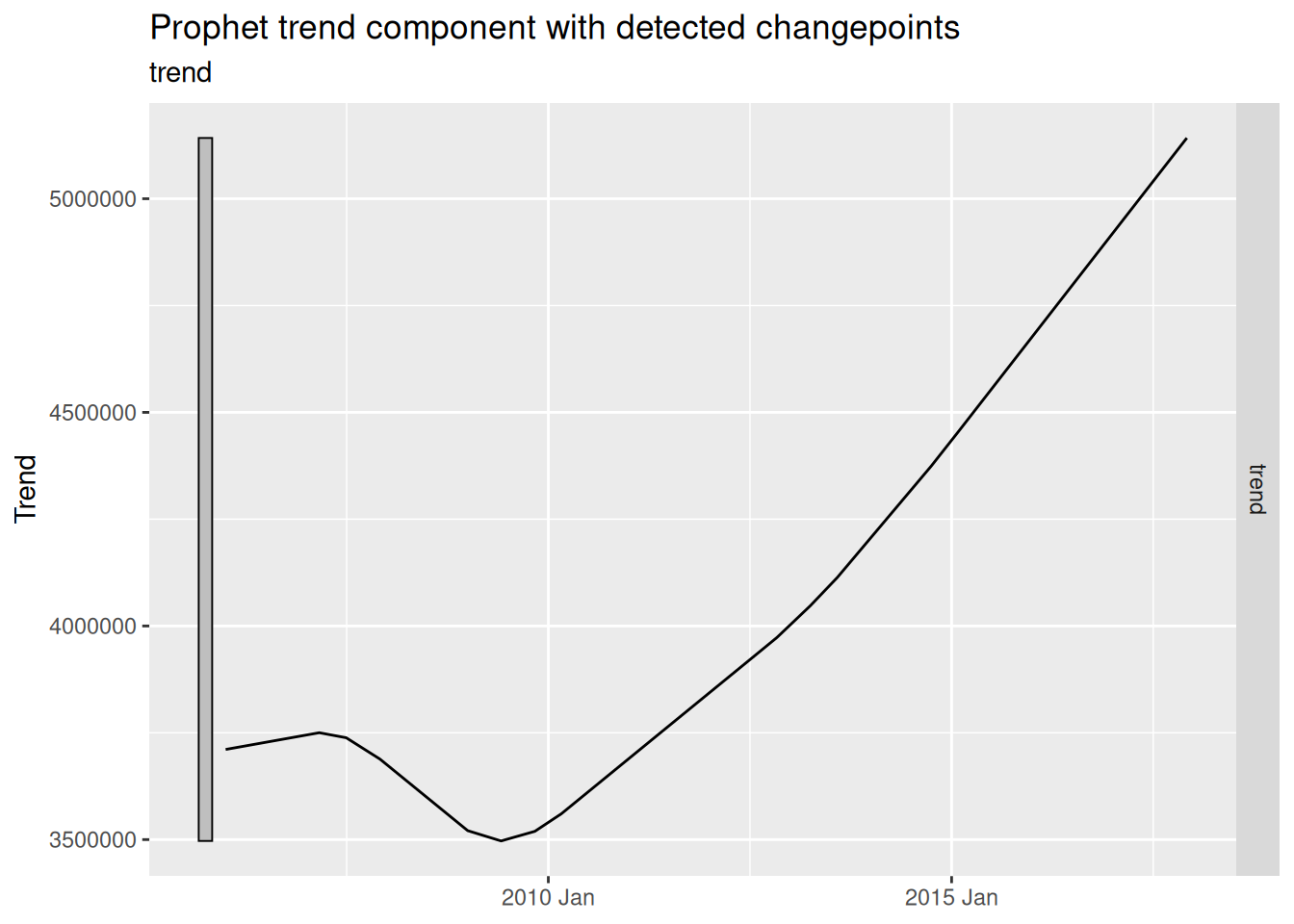

6 Changepoints: Diagnosing the Trend

We can extract the changepoints Prophet detected and plot them against the original series — a powerful diagnostic for communicating with stakeholders.

Code

# Extract trend component to visualize changepoints

lax_fit |>

select(type, Prophet) |>

filter(type == "Domestic") |>

components() |>

autoplot(trend) +

labs(

title = "Prophet trend component with detected changepoints",

y = "Trend",

x = NULL

)

TipComparing to piecewise TSLM

In Linear Regression we saw that different manual knot choices produce dramatically different forecasts. The plot above shows what Prophet automatically detected as genuine structural breaks — no trial and error needed.

7 Model Comparison

7.1 Which model wins?

Let’s put all models side by side — zooming in on the test period:

Code

p <- lax_fc |>

ggplot(aes(x = month, y = .mean, color = .model)) +

geom_line() +

geom_line(

data = lax_passengers |> filter_index("2015 Jan." ~ .),

aes(y = passengers, color = NULL),

color = "grey30",

linewidth = 0.8

) +

facet_wrap(~ type, ncol = 1, scales = "free_y") +

labs(

title = "All models: point forecast comparison",

y = "Passengers",

x = NULL,

color = "Model"

) +

theme(legend.position = "top")

ggplotly(p)

NoteWhat to look for in model comparison

- Does any model consistently over- or under-forecast?

- Do the Prophet variants track the seasonal shape better than ARIMA/ETS?

- Is

Prophet_automeaningfully different from the manualProphet?

These visual checks complement the numeric accuracy table — a model can have good MAPE but systematically miss peaks or troughs.

7.2 When does Prophet shine?

| Scenario | Prophet advantage |

|---|---|

| Daily / hourly data with multiple seasonalities | Handles automatically; ARIMA struggles |

| Known structural breaks (holidays, crises) | holiday() term + changepoints |

| Non-technical audience needs interpretation | Readable component plots |

| Large-scale automated forecasting | Consistent, robust default behavior |

| Short quarterly series (< 4 years) | ARIMA/ETS preferred |

| Stationary series, no trend | ARIMA preferred |

7.3 Prophet vs. the rest

| Feature | ARIMA | ETS | Dynamic Reg. | Prophet |

|---|---|---|---|---|

| Automatic specification | ✅ | ✅ | ❌ | ✅ |

| Multiple seasonalities | ⚠️ | ⚠️ | ✅ (Fourier) | ✅ |

| Changepoints (automatic) | ❌ | ❌ | ❌ | ✅ |

| Holiday effects | ❌ | ❌ | ✅ (manual) | ✅ |

| Interpretable components | ⚠️ | ✅ | ✅ | ✅ |

| Formal inference | ✅ | ✅ | ✅ | ⚠️ |

| Very short series | ✅ | ✅ | ⚠️ | ❌ |

8 Summary

| Component | Syntax | Purpose |

|---|---|---|

| Automatic | prophet(y) |

Let Prophet decide everything |

| Linear trend | growth("linear") |

Piecewise linear with auto changepoints |

| Logistic trend | growth("logistic") |

S-curve growth with capacity |

| Additive season | season("year", type = "additive") |

Fixed seasonal amplitude |

| Multiplicative season | season("year", type = "multiplicative") |

Seasonal amplitude scales with level |

| Fourier order | season("year", order = K) |

Flexibility of seasonal shape |

| Holiday effects | holiday(holidays_df) |

User-supplied event windows |

Key takeaways:

- Prophet is a decomposition model — trend + seasonality + holidays + noise — fitting the same structure we’ve built all semester, but in an automated, Bayesian framework.

- The key innovation is automatic changepoint detection: no manual knot selection required.

- In

fable, Prophet fits into the samemodel()→forecast()→accuracy()workflow — no new syntax to learn. - Prophet is not universally better: on short, classical economic series, ARIMA and ETS often win. Always compare on a held-out test set.

- Components are interpretable and easy to communicate to non-technical stakeholders — a real practical advantage.

Coming up in Module 4: We’ve now seen all the main model families. In Module 4, we tackle what happens when data has multiple seasonal periods simultaneously (daily + weekly + yearly), and how to make our models robust to outliers, missing values, and real-world messiness — including ensembling the models we’ve built throughout the semester.