Code

1library(tidyquant)

library(plotly)- 1

-

In addition to the regular packages, here we’ll use

tidyquantandplotly.

1library(tidyquant)

library(plotly)tidyquant and plotly.

Have you ever heard the word “stationary” before?

If a time series is “not moving”, what statistical properties would you expect it to have?

A time series is stationary if its statistical properties — primarily its mean and variance — do not change over time.

Which of the following six series are stationary (i.e., which look more stable)?

Key distinction: Seasonality repeats at a fixed, known frequency. Business cycles rise and fall irregularly.

A time series is non-stationary if it exhibits any of the following:

A stationary serie will not have any systematic patterns that change the level or scale of the series over time (no trend, no seasonality, and constant variance).

There is an important family of forecasting models that work by describing the correlation structure between a series and its own past values.

For those correlations to be stable and meaningful, the series needs to be stationary.

If these models require stationarity, does that mean they can only work with series that have no trend, no seasonality, and no changing variance?

Or is there something we can do to a non-stationary series to make it usable?

Recall from Module 1: we can stabilize the variance using mathematical transformations — logarithms, Box-Cox, and so on.

Transformations alone don’t remove a trend or seasonal pattern.

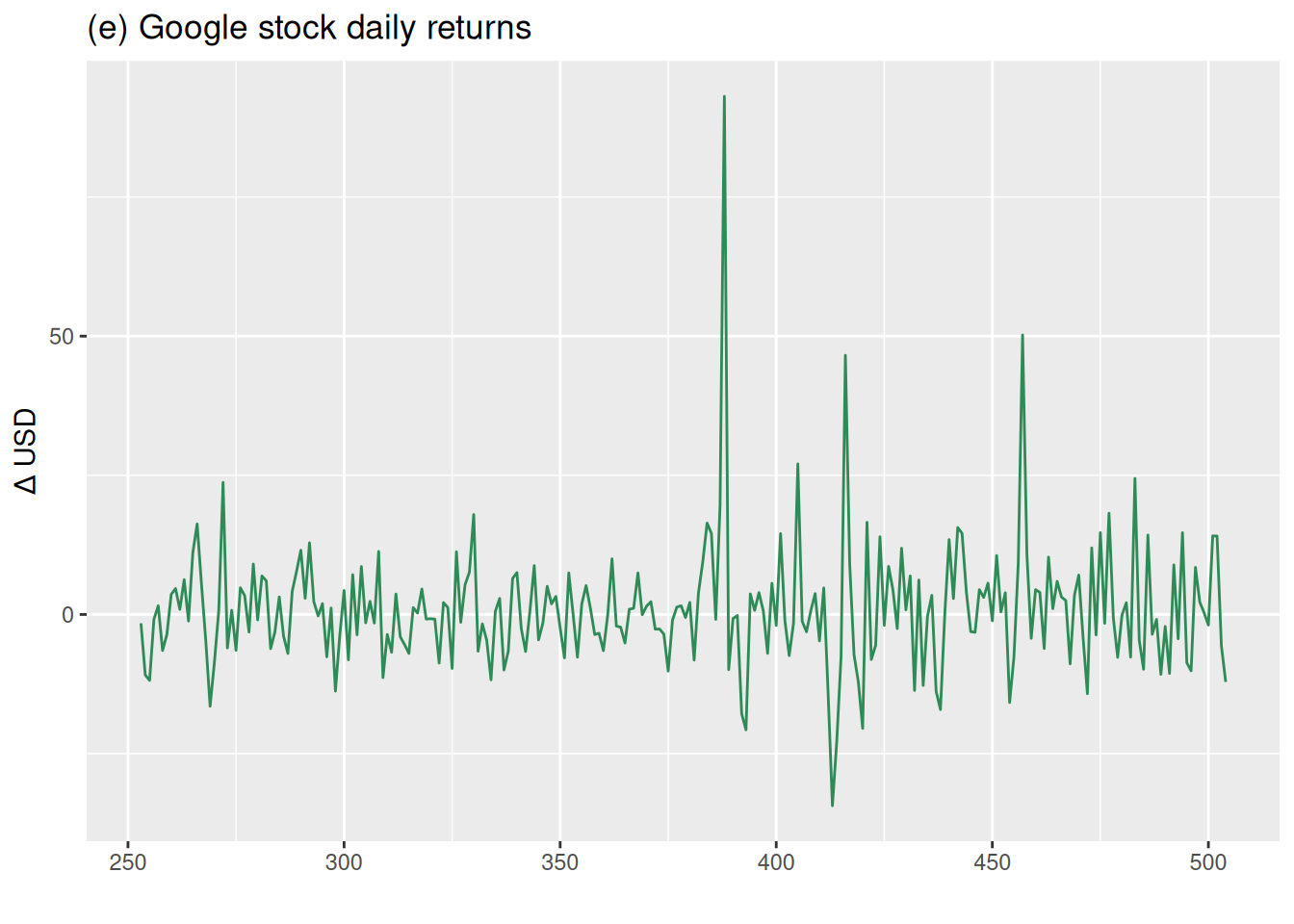

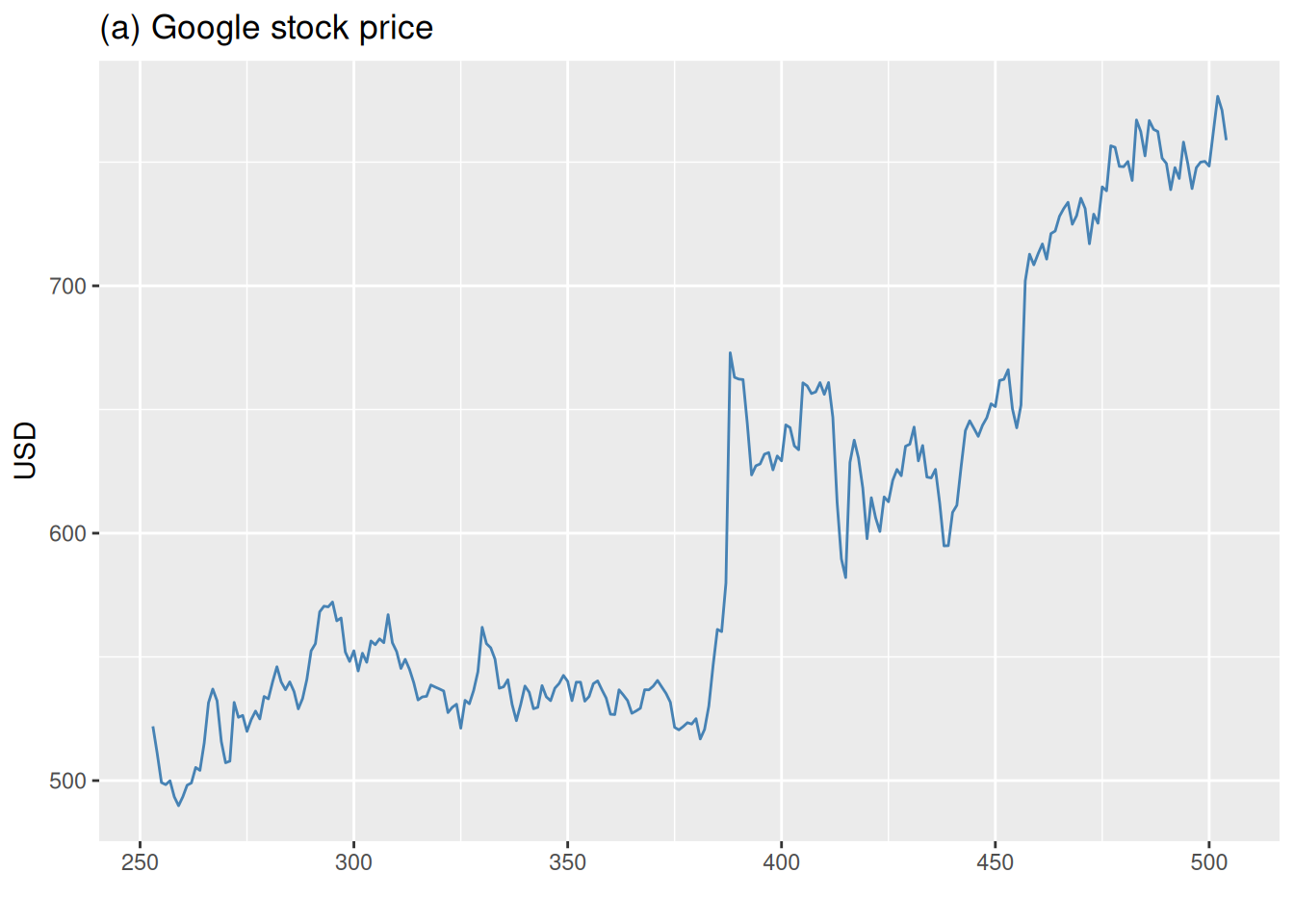

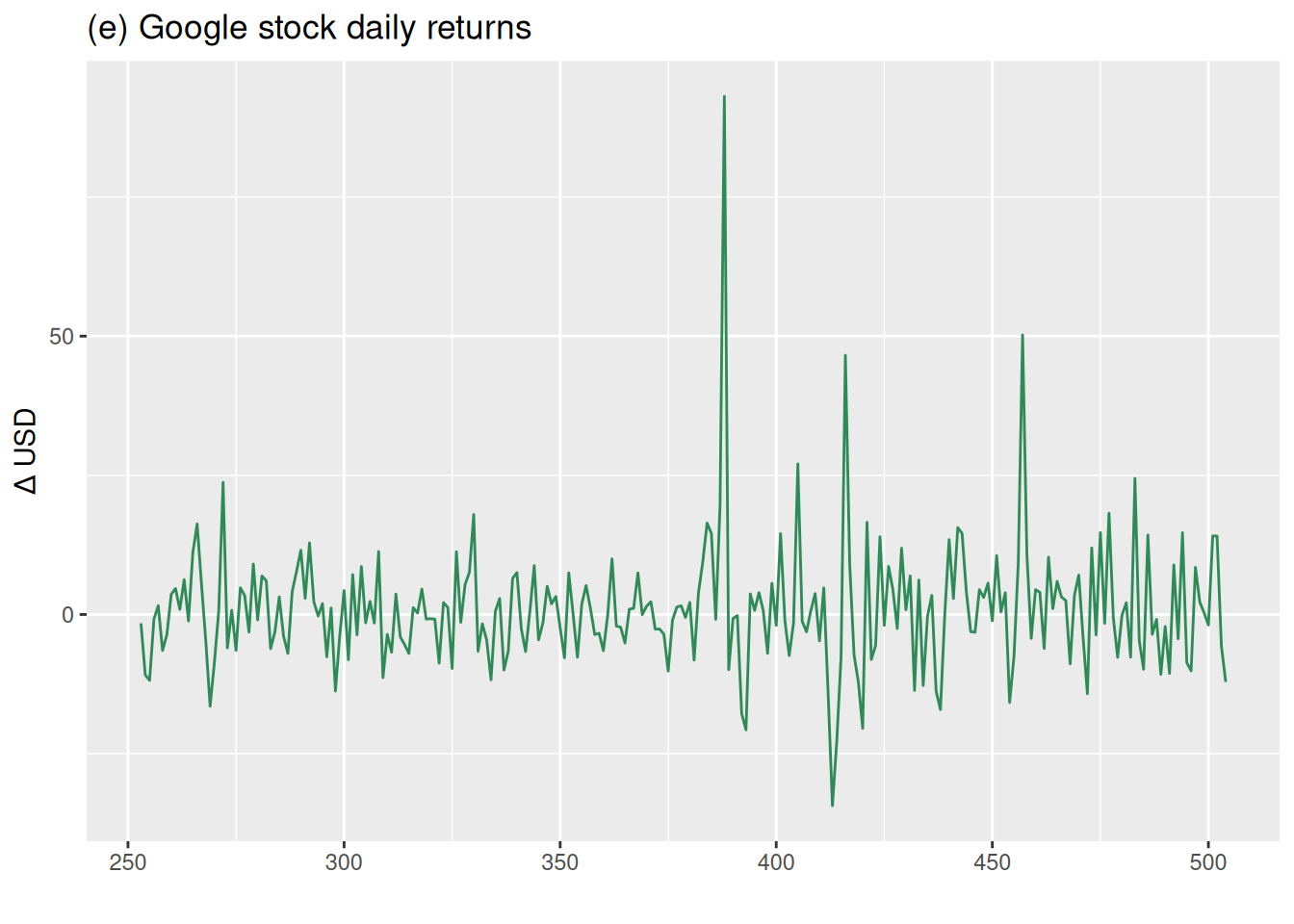

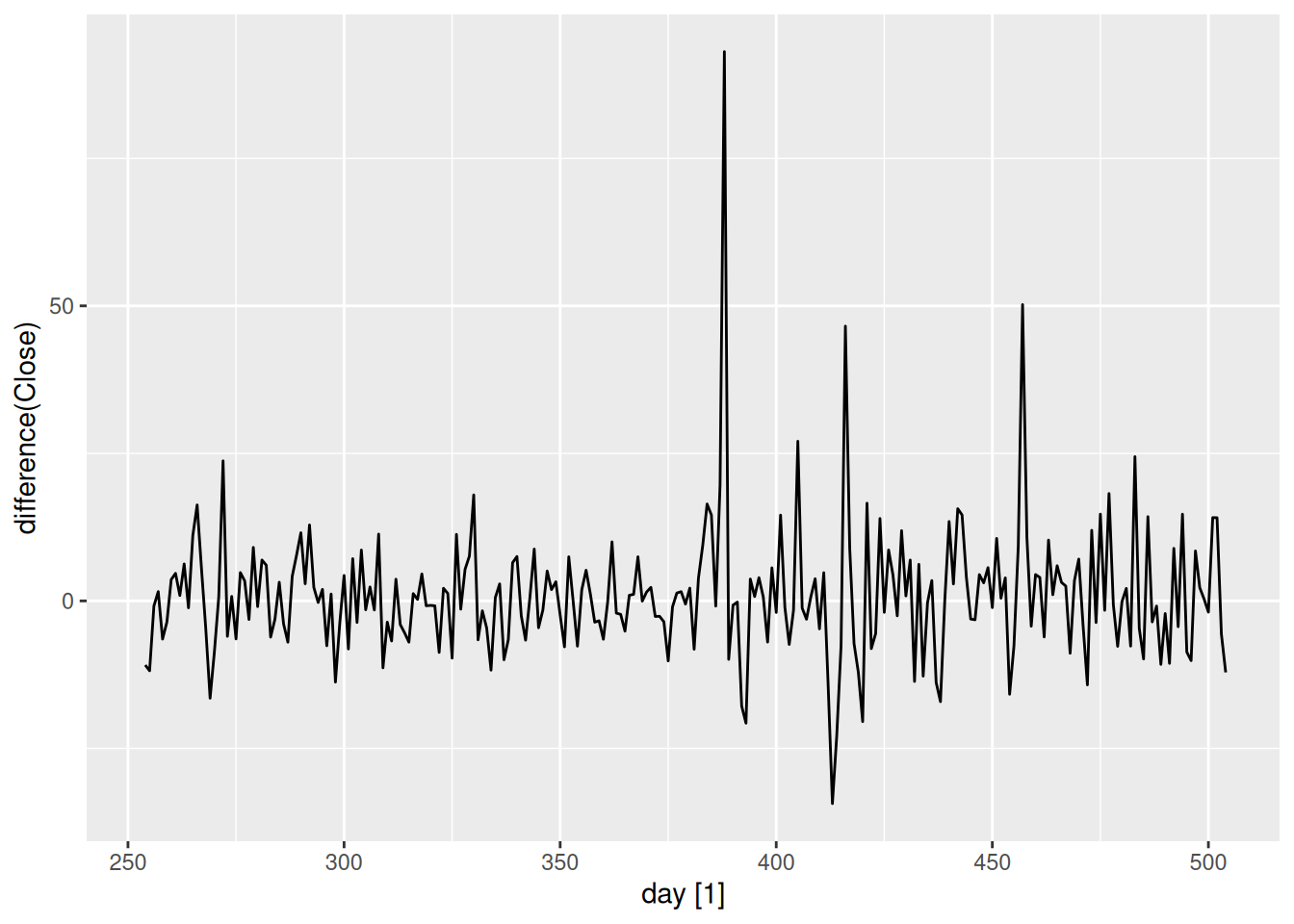

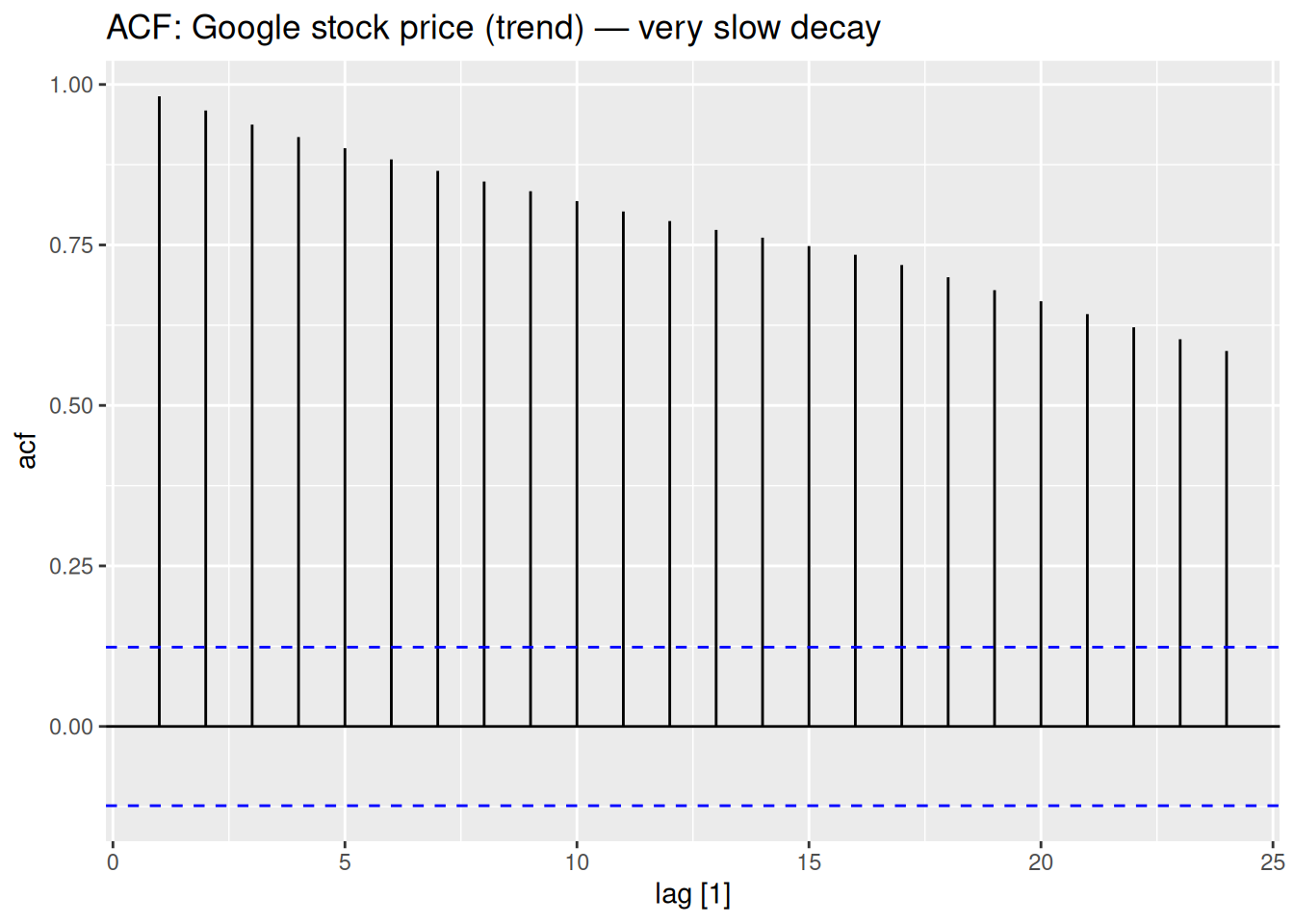

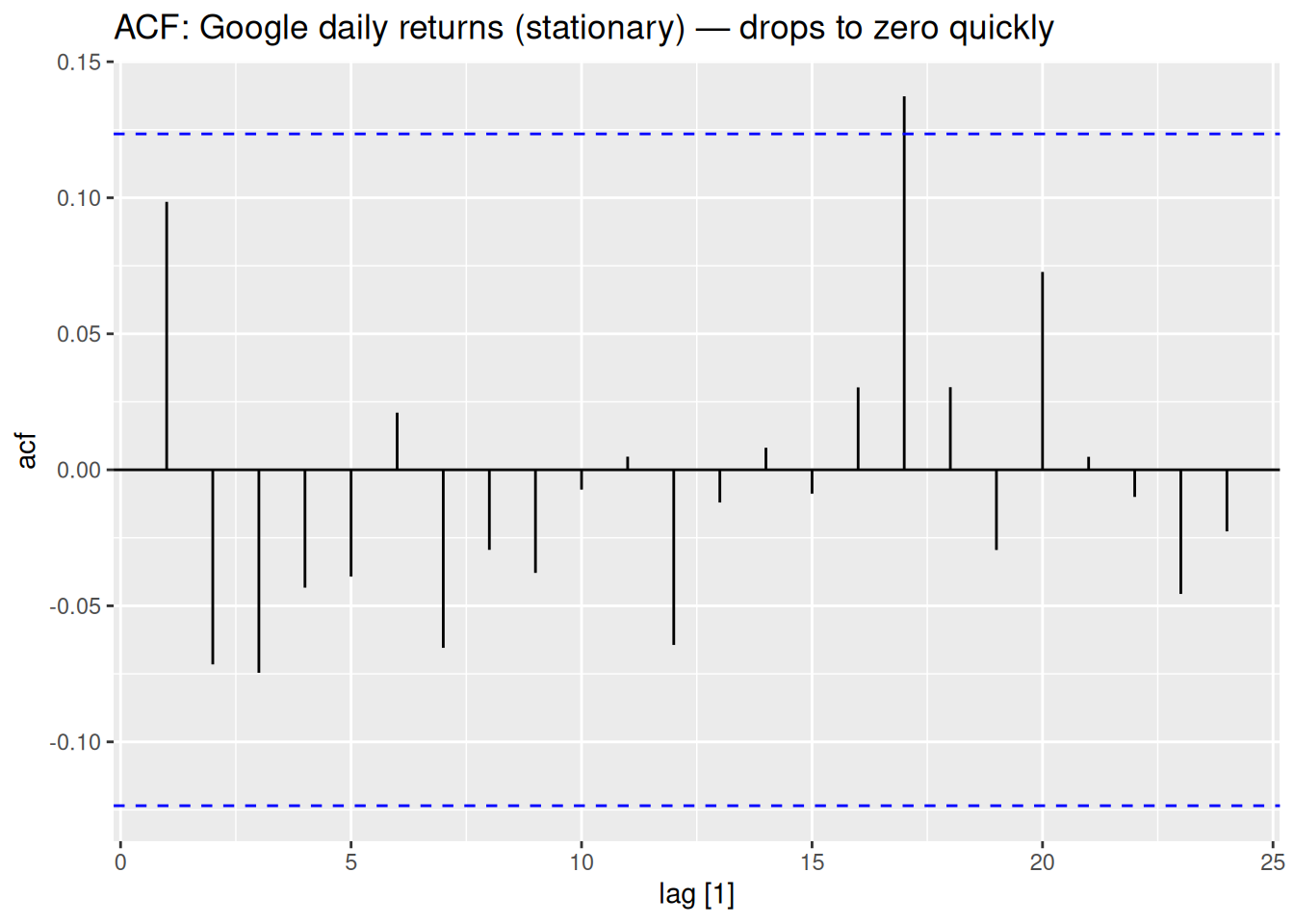

Look at these two series:

The second series was produced directly from the first. Can you figure out how?

The daily return is simply today’s price minus yesterday’s price — the change between consecutive observations. This operation is called differencing, and it is how we stabilize the mean of a non-stationary series.

The first difference of a series y_t is:

y'_t = y_t - y_{t-1}

google_2015 |>

1 autoplot(difference(Close))difference(Close) computes the first difference of the Close variable.

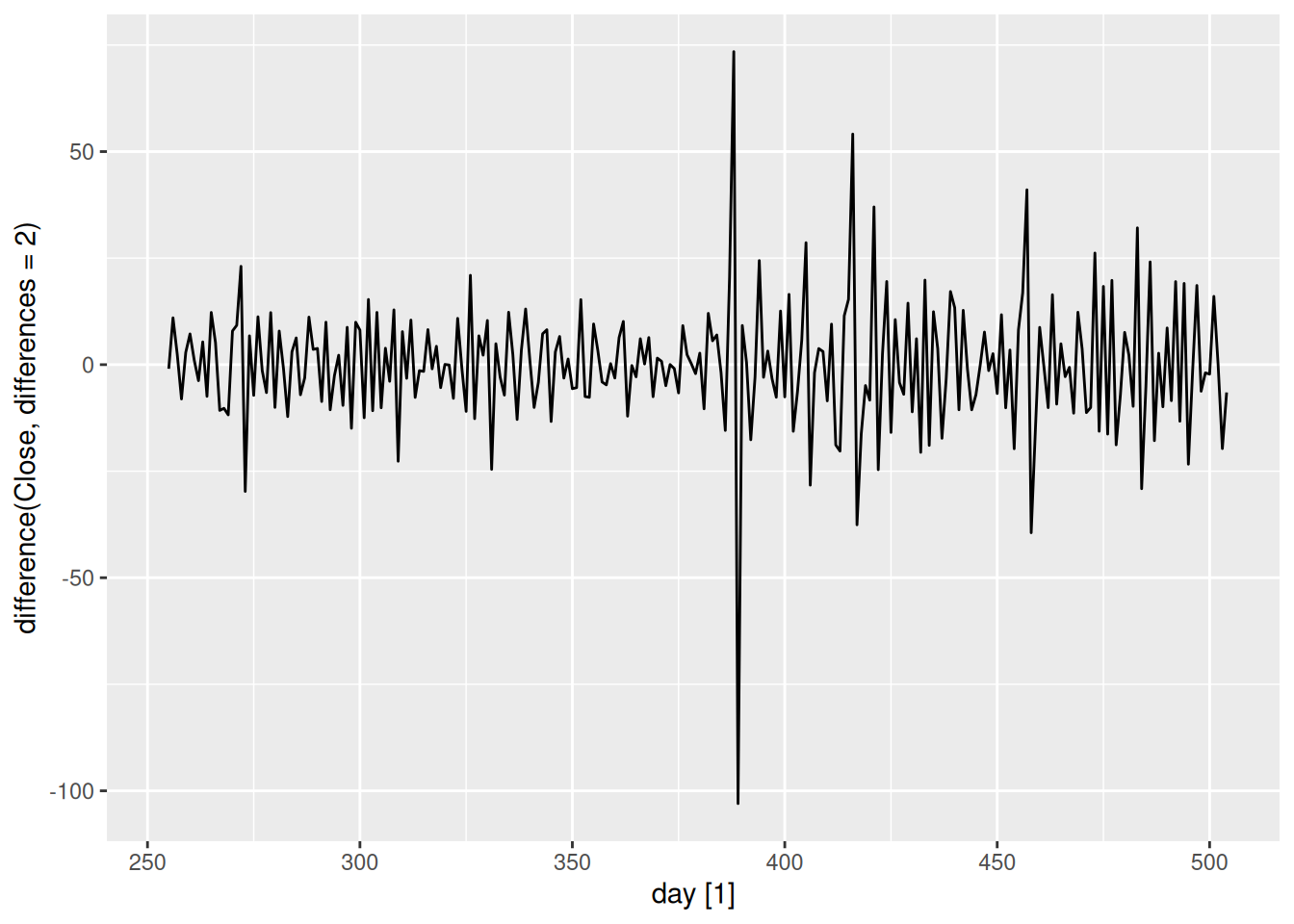

Sometimes the first-differenced series is still non-stationary. We can difference again:

\begin{align*} y''_t &= y'_t - y'_{t-1} \\ &= (y_t-y_{t-1}) - (y_{t-1} - y_{t-2}) \\ &= y_t - 2y_{t-1} + y_{t-2} \end{align*}

Needing three or more differences usually signals something else is wrong — an outlier, a structural break, or a transformation that should have been applied first.

google_2015 |>

1 autoplot(difference(Close, differences = 2))differences = 2 tells difference() to apply the differencing operation twice.

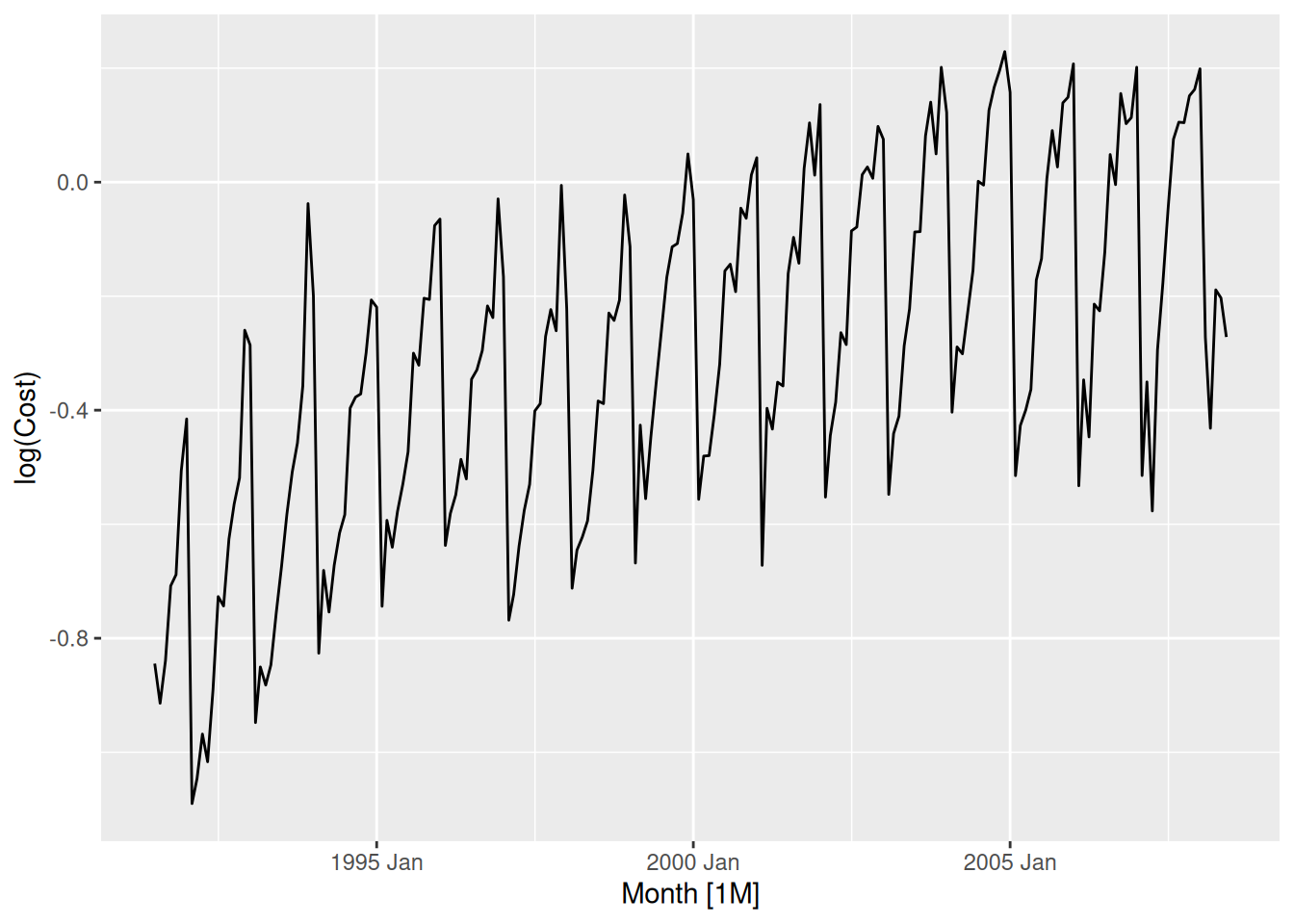

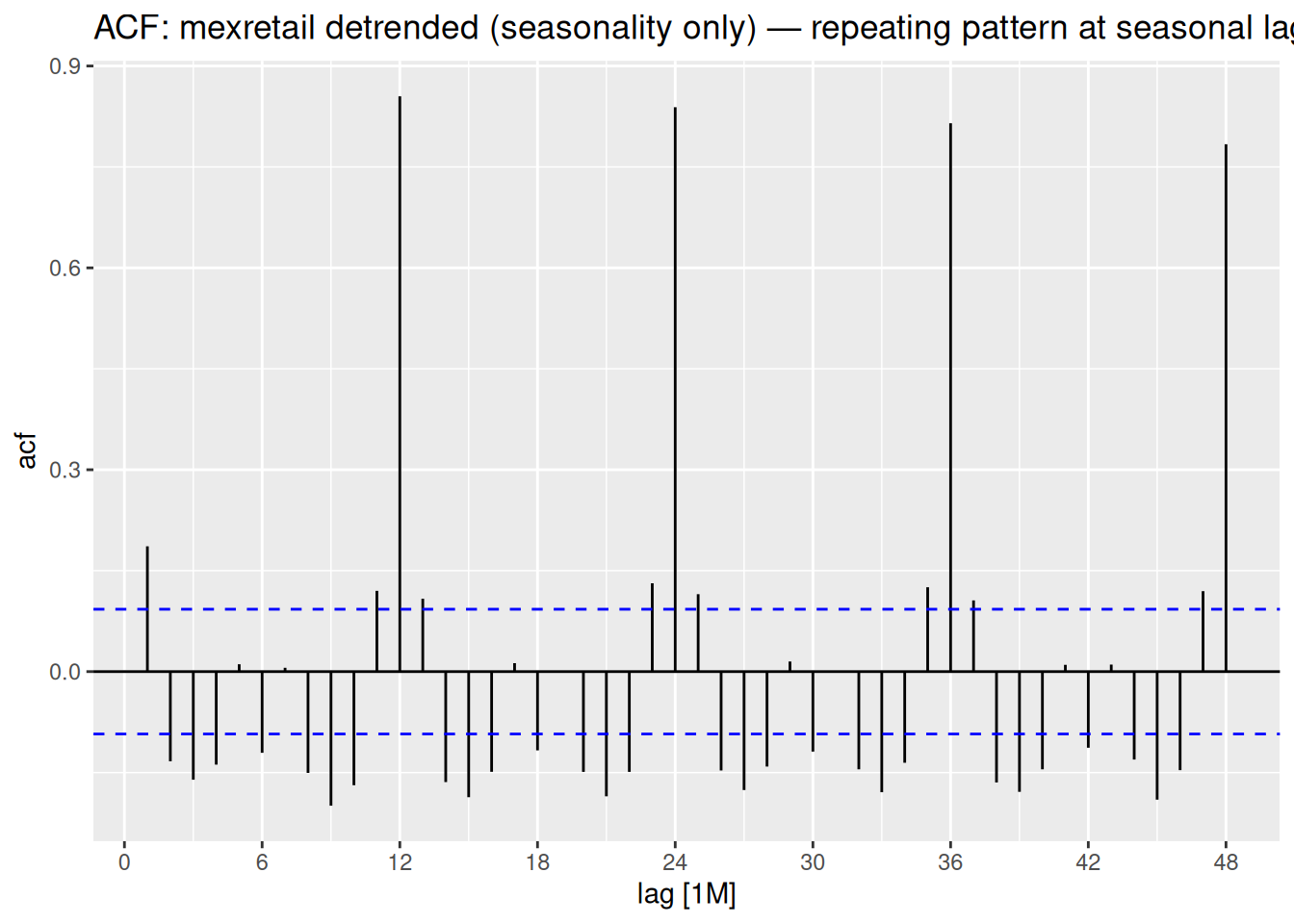

If the series has seasonality, we take a seasonal difference — the change relative to the same period in the previous cycle:

y'_t = y_t - y_{t-m}

where m is the seasonal period (m = 12 for monthly data, m = 4 for quarterly, …).

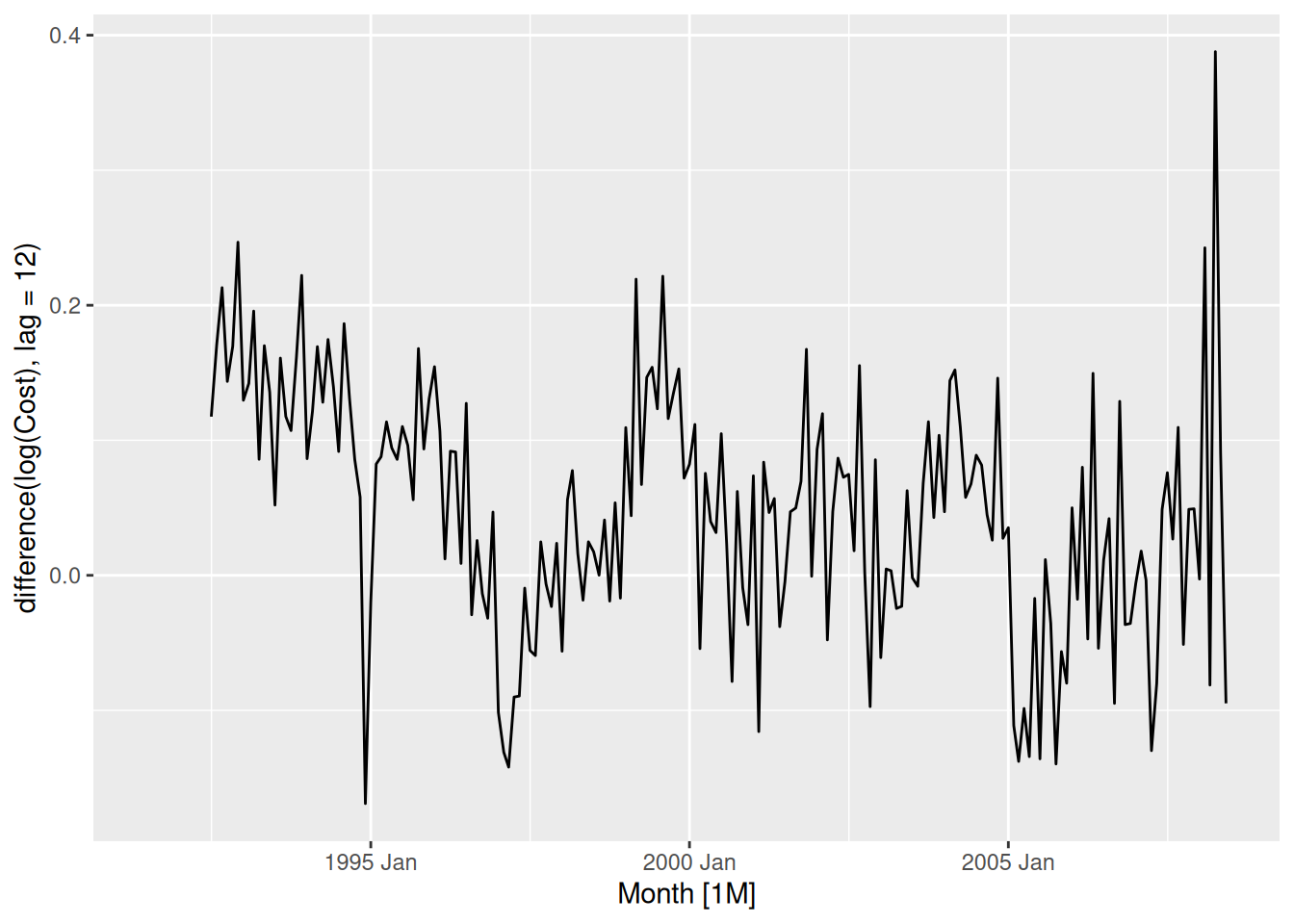

h02 |>

1 autoplot(difference(log(Cost), lag = 12))lag = 12 tells difference() to compute the seasonal difference with a lag of 12 periods (i.e. y_t - y_{t-12}). If no lag is specified, it defaults to 1 (the first difference).

When a series needs both seasonal and regular differencing, does it matter which one we apply first?

Applying seasonal first, then regular:

\begin{align*} (y_t - y_{t-m})' &= (y_t - y_{t-m}) - (y_{t-1} - y_{t-m-1}) \\ &= y_t - y_{t-1} - y_{t-m} + y_{t-m-1} \end{align*}

Applying regular first, then seasonal:

\begin{align*} (y_t - y_{t-1})' &= (y_t - y_{t-1}) - (y_{t-m} - y_{t-m-1}) \\ &= y_t - y_{t-1} - y_{t-m} + y_{t-m-1} \end{align*}

Both routes lead to the same result.

The order does not matter — the result is always identical. In practice, if the seasonal pattern is strong, apply the seasonal difference first: the result may already be stationary without needing the regular difference.

The backshift operator B provides a compact way to write differencing operations — and, as we will see next class, to write out full model equations cleanly.

It is defined simply as:

By_t = y_{t-1} ; B(By_t) = B^2 y_t = y_{t-2}

That is, applying B to a series shifts it back one period.

Recall the first difference:

y'_t = y_t - y_{t-1}

We can rewrite y_{t-1} = By_t, so:

y'_t = y_t - By_t = (1 - B)y_t

Recall:

y''_t = y_t - 2y_{t-1} + y_{t-2}

Using the backshift operator turns to:

y''_t = y_t - 2By_t + B^2 y_t = (1 - 2B + B^2)y_t

which gives a perfect square trinomial2

y''_t = (1-B)^2 y_t

The pattern generalizes naturally:

(1 - B)^d y_t

where d is the number of times we difference the series.

For a general order d, the binomial theorem gives:

(1-B)^d = \sum_{k=0}^{d} \binom{d}{k} (-B)^k = \sum_{k=0}^{d} \binom{d}{k} (-1)^k B^k

So:

(1-B)^d y_t = \sum_{k=0}^{d} \binom{d}{k} (-1)^k y_{t-k}

For d=1: y_t - y_{t-1} ✓

For d=2: y_t - 2y_{t-1} + y_{t-2} ✓

A seasonal difference shifts back m periods:

y_t - y_{t-m} = y_t - B^m y_t = (1 - B^m)y_t

And when both are needed — as with mexretail — the two operators simply multiply:

(1-B)(1-B^m)y_t

which is exactly the expression we expanded by hand in the previous section.

| Operation | Backshift form |

|---|---|

| First difference | (1 - B)\,y_t |

| Second difference | (1 - B)^2\,y_t |

| d-th difference | (1 - B)^d\,y_t |

| Seasonal difference | (1 - B^m)\,y_t |

| Both together | (1 - B)^d(1 - B^m)\,y_t |

Using backshift notation, it becomes trivial to see that the order doesn’t matter. Both orderings produce the same expression, since multiplication is commutative:

(1-B)(1-B^m)y_t = (1-B^m)(1-B)y_t

No algebra needed.

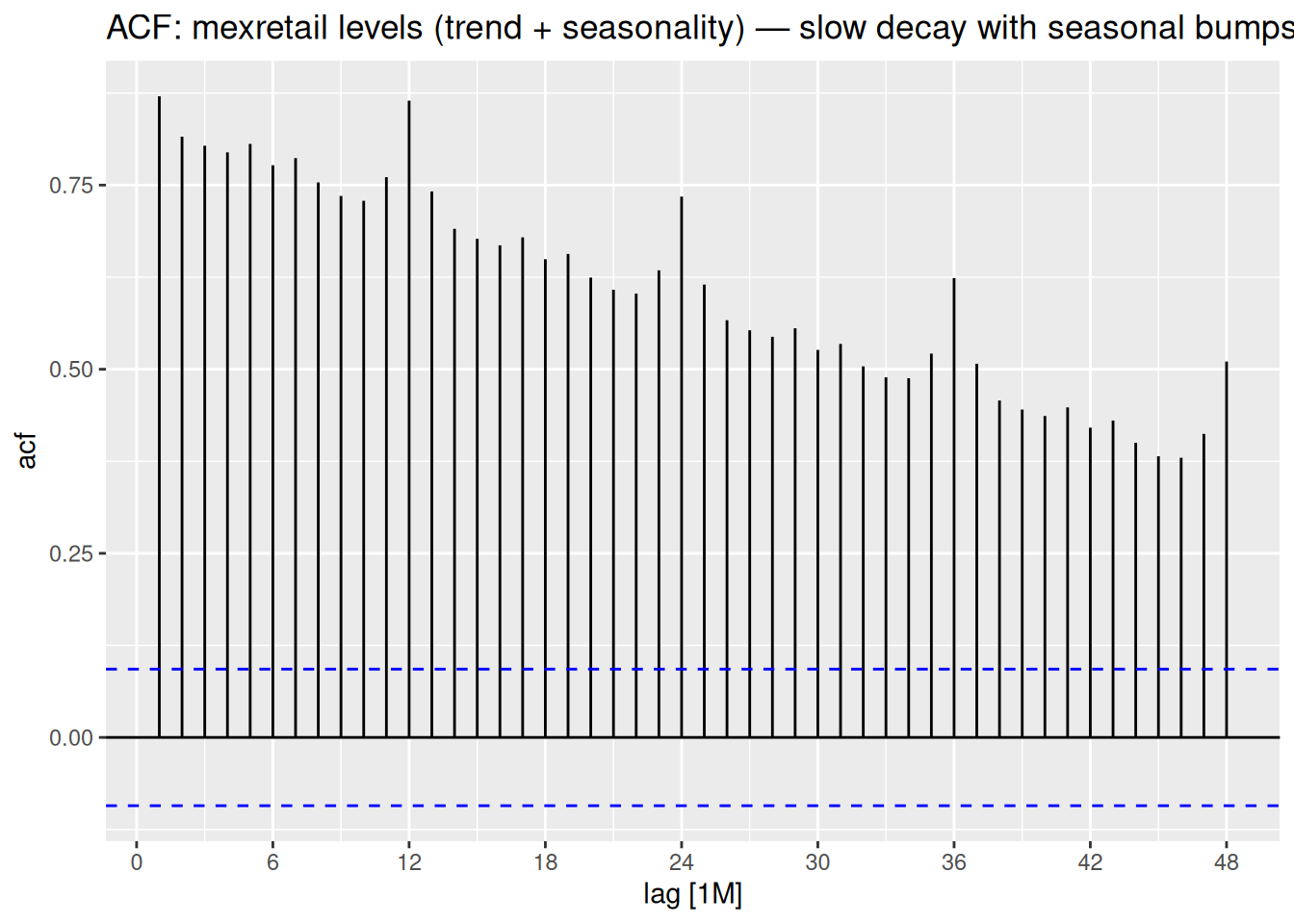

mexretailmexretail has trend, seasonality, and growing variance. The full differencing pipeline:

We have been deciding how many differences to apply by looking at plots. But visual inspection is subjective — two analysts could disagree. Is there a more rigorous, objective way to make this call?

Visual inspection is useful but subjective. Unit root tests formalize the question: is this series stationary?

The test we will use is the KPSS test (Kwiatkowski-Phillips-Schmidt-Shin).

The KPSS test works by regressing y_t on a constant (or a constant + trend), computing the residuals e_t, and then building their cumulative sums S_t = \sum_{i=1}^{t} e_i. The test statistic is:

\text{KPSS} = \frac{1}{T^2} \sum_{t=1}^{T} \frac{S_t^2}{\hat{\sigma}^2}

where \hat{\sigma}^2 is a long-run variance estimate that corrects for autocorrelation in the residuals.

The intuition: if the series is stationary, the residuals e_t fluctuate around zero and their cumulative sums S_t stay bounded. If the series has a unit root (non-stationary), the cumulative sums drift away from zero — making the statistic large and leading to rejection of H_0.

H_0: \text{the series IS stationary} H_1: \text{the series is NOT stationary}

You want a large p-value here.

google_2015 |> features(Close, unitroot_kpss)google_2015 |> features(diff_close, unitroot_kpss)Rather than manually testing each transformation, feasts provides two functions that determine exactly how many differences are needed:

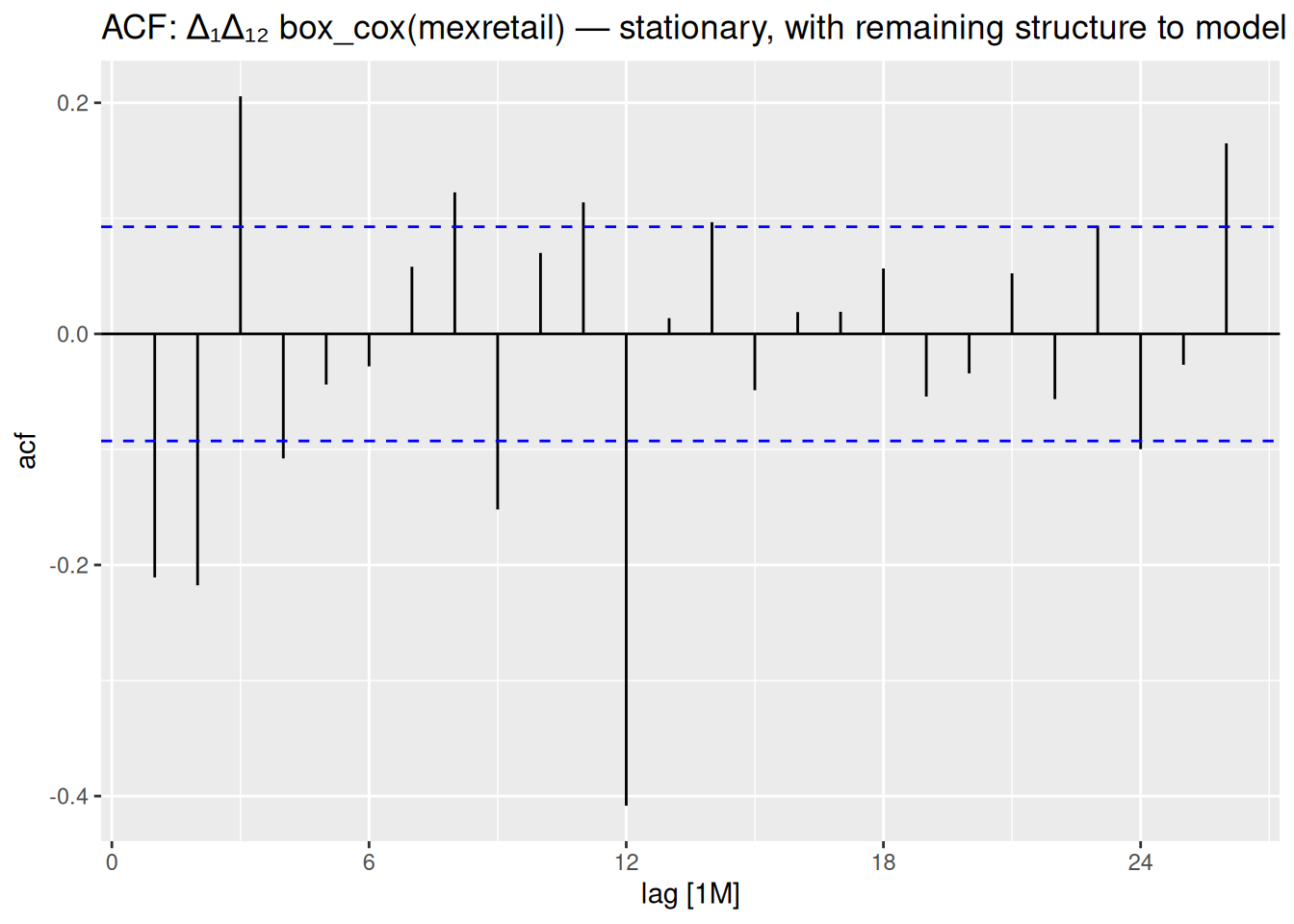

mexretail |> features(box_cox(y, lambda), unitroot_nsdiffs)mexretail |>

features(difference(box_cox(y, lambda), 12), unitroot_ndiffs)mexretail

box_cox(y, lambda)unitroot_nsdiffs() → 1unitroot_ndiffs() → 1difference(box_cox(y, lambda), 12) |> difference(1)We have already encountered the ACF when diagnosing residuals from our benchmark models — checking whether leftover errors looked like white noise. Here we use it for a different but related purpose: understanding the correlation structure of the series itself.

The ACF measures the correlation between a series and its own past values at each lag k:

r_k = \text{Corr}(y_t,\, y_{t-k})

This gives us another way to detect non-stationarity — and, as we will see, it also tells us about the structure of the model to fit.

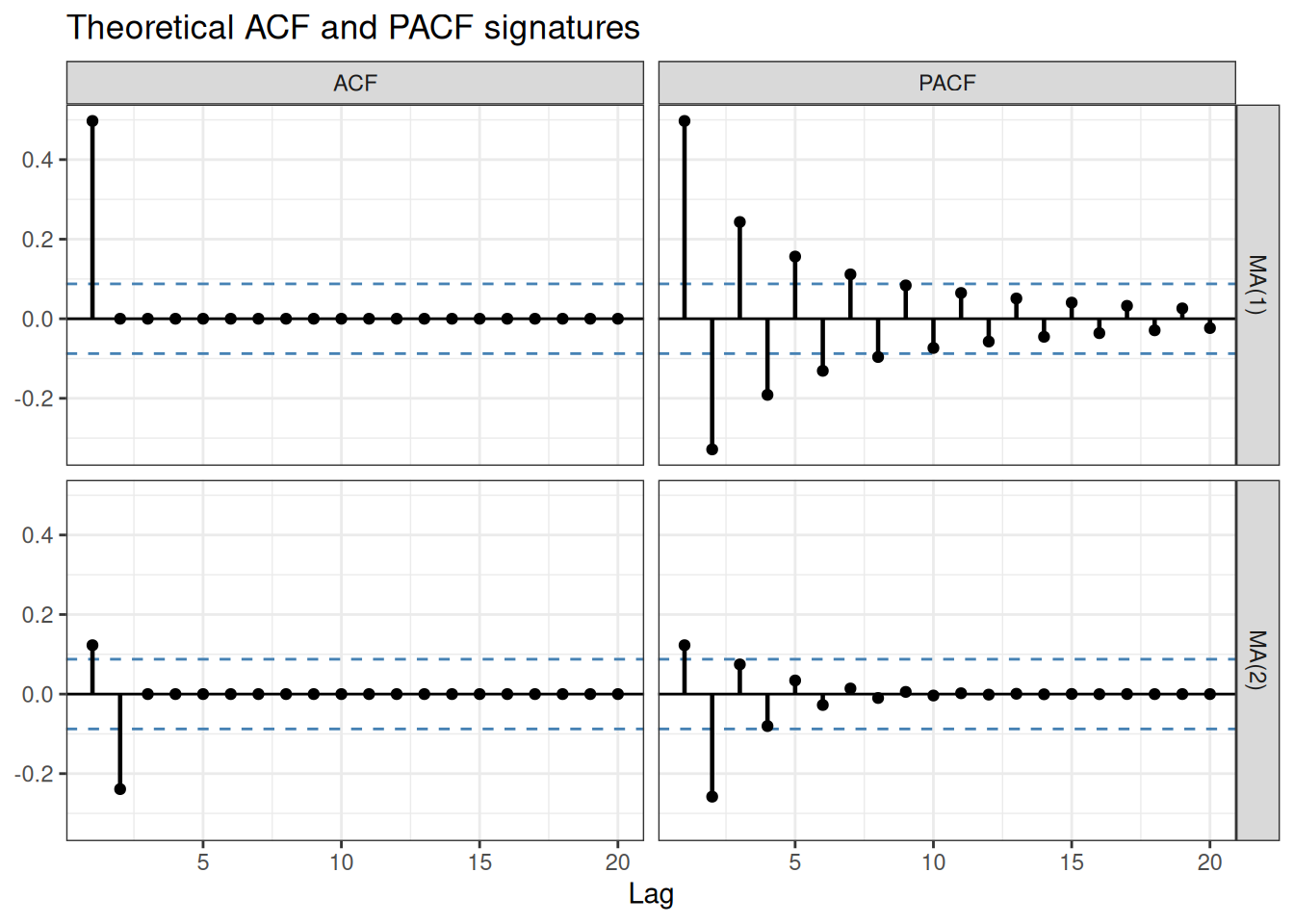

The ACF at lag k captures both the direct relationship between y_t and y_{t-k} and the indirect relationship mediated through intermediate lags. The PACF isolates only the direct part.

The PACF asks: once I already know the effect of all closer lags, does lag k add any new information?

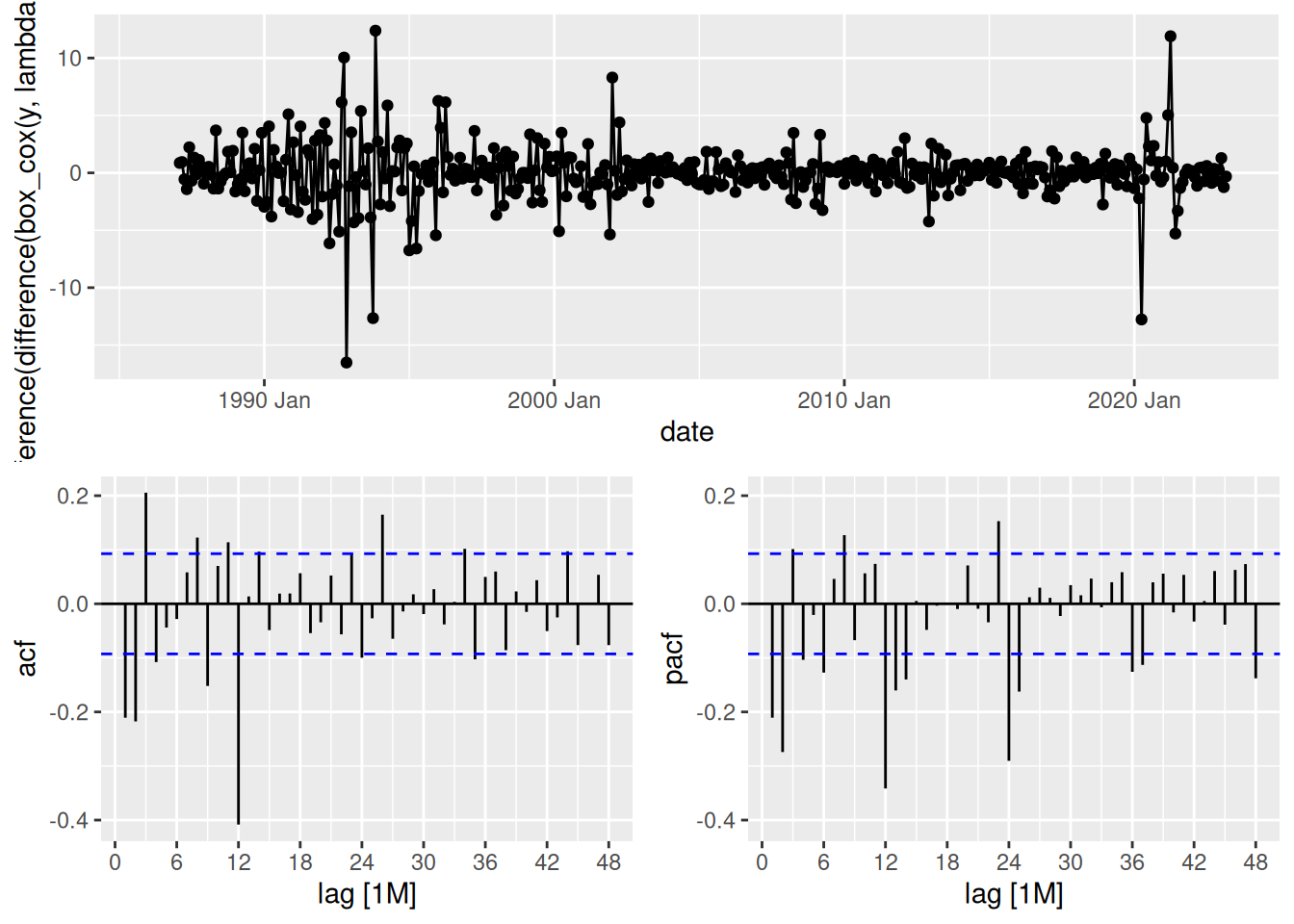

gg_tsdisplay() with plot_type = "partial" shows the time series, ACF, and PACF together — this is the standard diagnostic display for the rest of the module.

mexretail |>

gg_tsdisplay(

difference(box_cox(y, lambda), 12) |> difference(1),

plot_type = "partial",

lag_max = 48

)

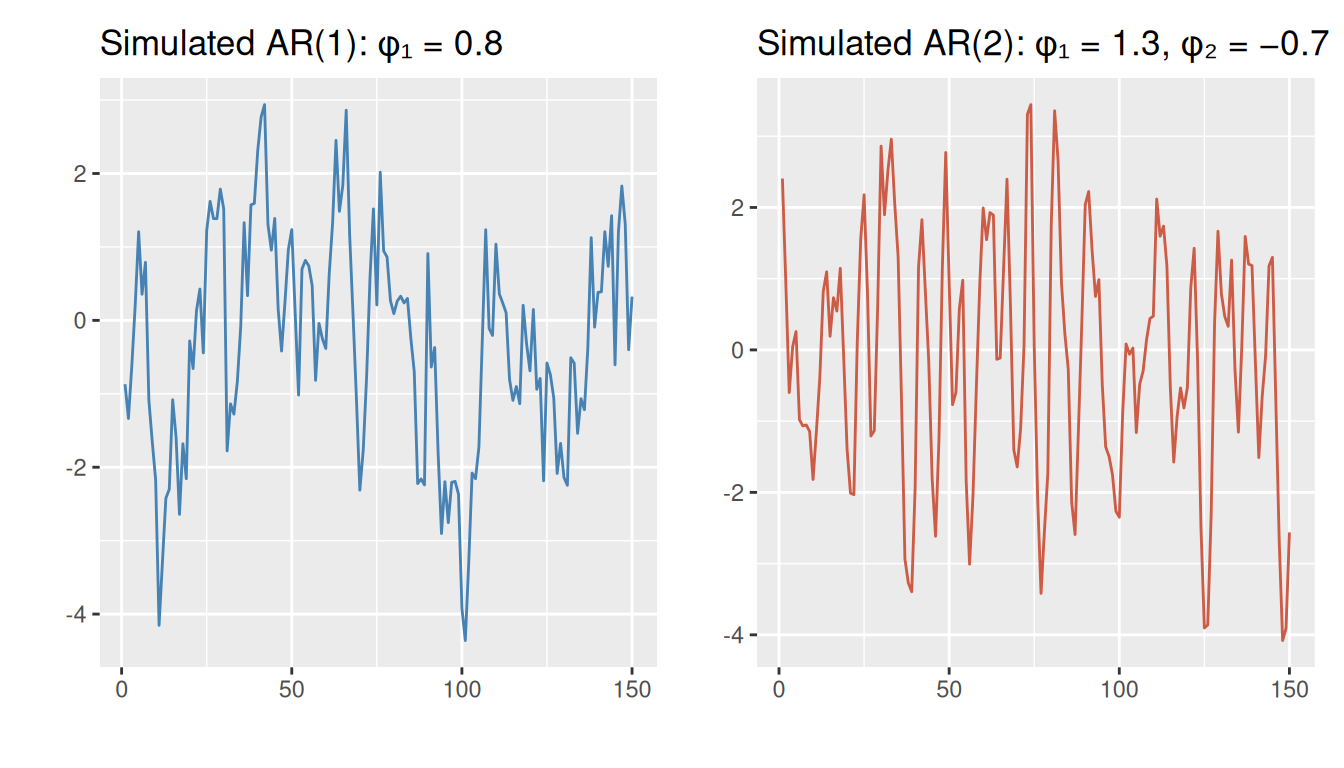

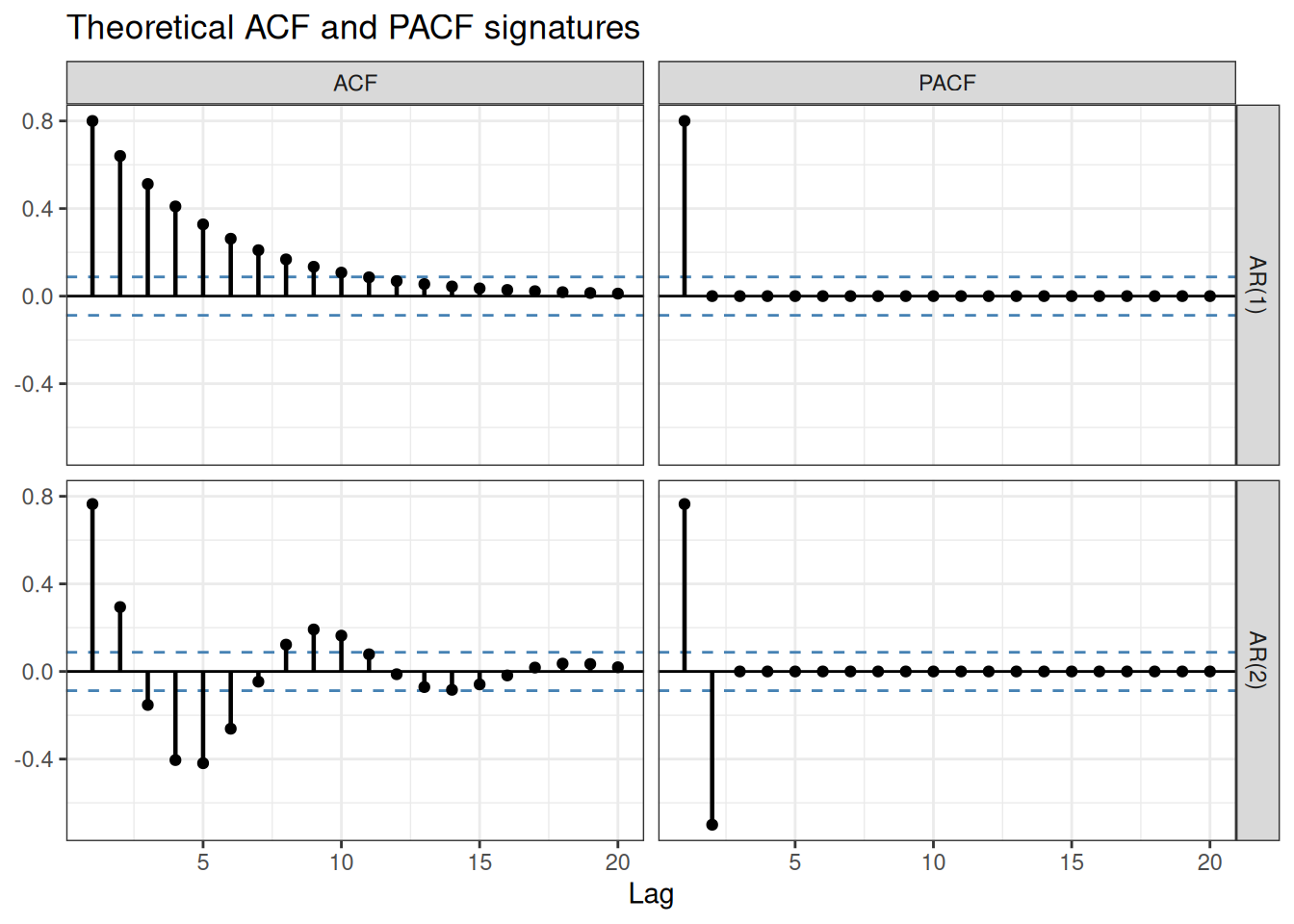

An autoregressive model of order p forecasts y_t as a weighted sum of its own past values:

y_t = c + \phi_1 y_{t-1} + \phi_2 y_{t-2} + \cdots + \phi_p y_{t-p} + \varepsilon_t

A moving average model of order q forecasts y_t as a weighted sum of past forecast errors:

y_t = c + \varepsilon_t + \theta_1 \varepsilon_{t-1} + \theta_2 \varepsilon_{t-2} + \cdots + \theta_q \varepsilon_{t-q}

Do not confuse MA models with the moving average smoothing used in decomposition. Smoothing estimates the trend-cycle from past observed values. MA models use past errors to describe the correlation structure of the series.

Now that you have seen AR and MA models: their time plots can look very similar to each other. The ACF and PACF are what distinguish them. This is fundamentally different from ETS, where the form of trend and seasonality in the time plot directly guides model selection — one of the key differences we will revisit when comparing these two families.

In practice, you will rarely use a pure AR or pure MA model. Real series typically need both. And most real series also need differencing before any of this applies.

Combining differencing, AR terms, and MA terms into a single unified model — and applying it systematically to mexretail — is the subject of the next class.

All the pieces are in place. Time to put them together.