Code

library(tidyverse)

library(fpp3)

library(plotly)fable

It is recommended to load all the packages at the beginning of your file. We will be using the tidyverts ecosystem for the whole forecasting workflow.

library(tidyverse)

library(fpp3)

library(plotly)Do not load unnecesary packages into your environment. It could lead to conflicts between functions and unwanted results.

We will work with the Real Gross Domestic Product (GDP) for Mexico. The data is downloaded from FRED. The time series id is NGDPRNSAXDCMXQ.

gdp <- tidyquant::tq_get(

x = "NGDPRNSAXDCMXQ",

get = "economic.data",

from = "1997-01-01"

)

gdp# A tibble: 116 × 3

symbol date price

<chr> <date> <dbl>

1 NGDPRNSAXDCMXQ 1997-01-01 3702398.

2 NGDPRNSAXDCMXQ 1997-04-01 3896084.

3 NGDPRNSAXDCMXQ 1997-07-01 3906063

4 NGDPRNSAXDCMXQ 1997-10-01 4038358.

5 NGDPRNSAXDCMXQ 1998-01-01 4084304.

6 NGDPRNSAXDCMXQ 1998-04-01 4134899.

7 NGDPRNSAXDCMXQ 1998-07-01 4138200.

8 NGDPRNSAXDCMXQ 1998-10-01 4146841.

9 NGDPRNSAXDCMXQ 1999-01-01 4176243.

10 NGDPRNSAXDCMXQ 1999-04-01 4232280.

# ℹ 106 more rowsThere are some issues with our data:

tibble object. We need to convert it to a tsibble.We can use as_tsibble() to do so.

YYYY-MM-DD format. We need to change it to a YYYY QQ format.There are some functions that help us achieve this, such as

yearquarter()yearmonth()yearweek()year()depending on the time series’ period.

We will overwrite our data:

gdp <- gdp |>

mutate(date = yearquarter(date)) |>

as_tsibble(

index = date,

key = symbol

)

gdpWe always need to specify the index argument, as it is our date variable.

The key argument is necessary whenever we have more than one time series in our data frame and is made up of one or more columns that uniquely identify each time series .

We will split our data in two sets: a training set, and a test set, in order to evaluate our forecasts’ accuracy.

gdp_train <- gdp |>

filter_index(. ~ "2021 Q4")

gdp_trainFor all our variables, it is strongly recommended to follow the same notation process, and write our code using snake_case. Here, we called our data gdp, therefore, all the following variables will be called starting with gdp_1, such as gdp_train for our training set.

When performing time series analysis/forecasting, one of the first things to do is to create a time series plot.

p <- gdp_train |>

autoplot(price) +

labs(

title = "Time series plot of the Real GDP for Mexico",

y = "GDP"

)

ggplotly(p, dynamicTicks = TRUE) |>

rangeslider()We will explore it further with a season plot.

gdp_train |>

gg_season(price) |>

ggplotly()gdp_train |>

model(stl = STL(price, robust = TRUE)) |>

components() |>

autoplot() |>

ggplotly()gdp_train |>

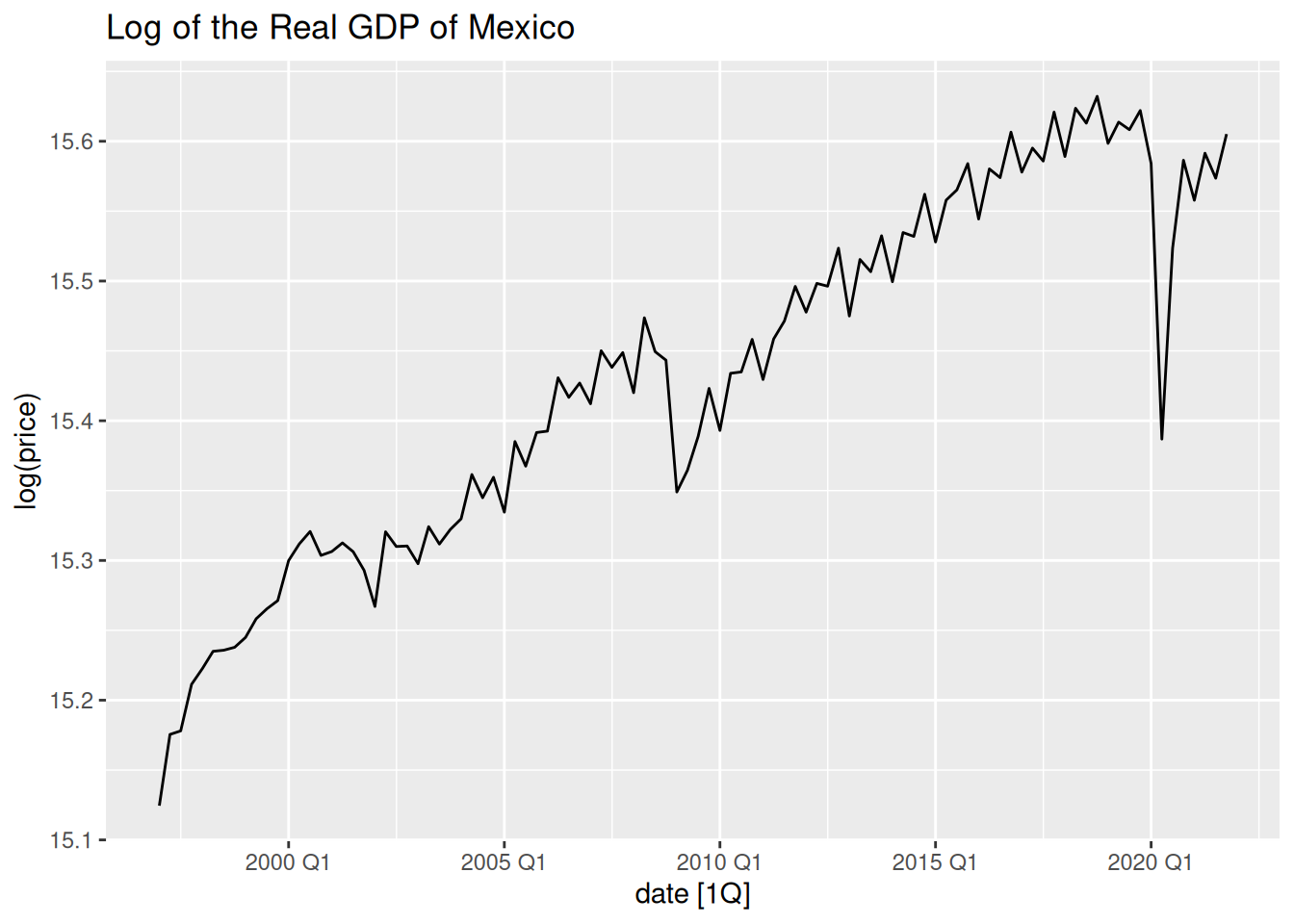

autoplot(log(price)) +

ggtitle("Log of the Real GDP of Mexico")

gdp_train |>

model(stl = STL(log(price) ~ season(window = "periodic"), robust = TRUE)) |>

components() |>

autoplot() |>

ggplotly()We will fit two models to our time series: Seasonal Naïve, and the Drift model. We will also use the log transformation.

gdp_fit <- gdp_train |>

model(

snaive = SNAIVE(log(price)),

drift = RW(log(price) ~ drift())

)We have four different benchmark models that we’ll use to compare against the rest of the more complex models:

MEAN( <.y> ))NAIVE( <.y> ))SNAIVE( <.y> ))RW( <.y> ~ drift()))where <.y> is just a placeholder for the variable to model.

Choose wisely which of these to use in each case, according to the exploratory analysis performed.

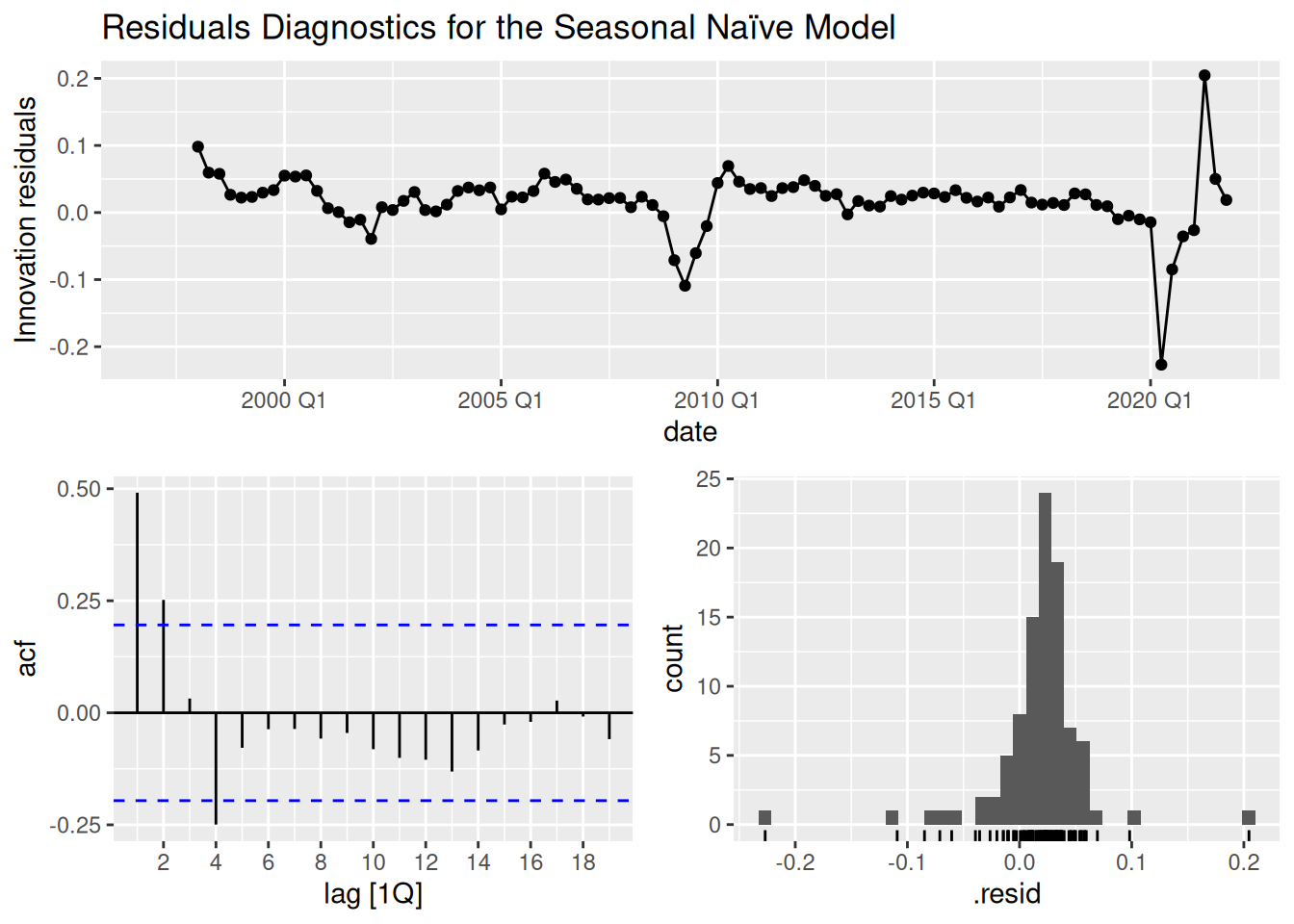

gdp_fit |>

select(snaive) |>

gg_tsresiduals() +

ggtitle("Residuals Diagnostics for the Seasonal Naïve Model")

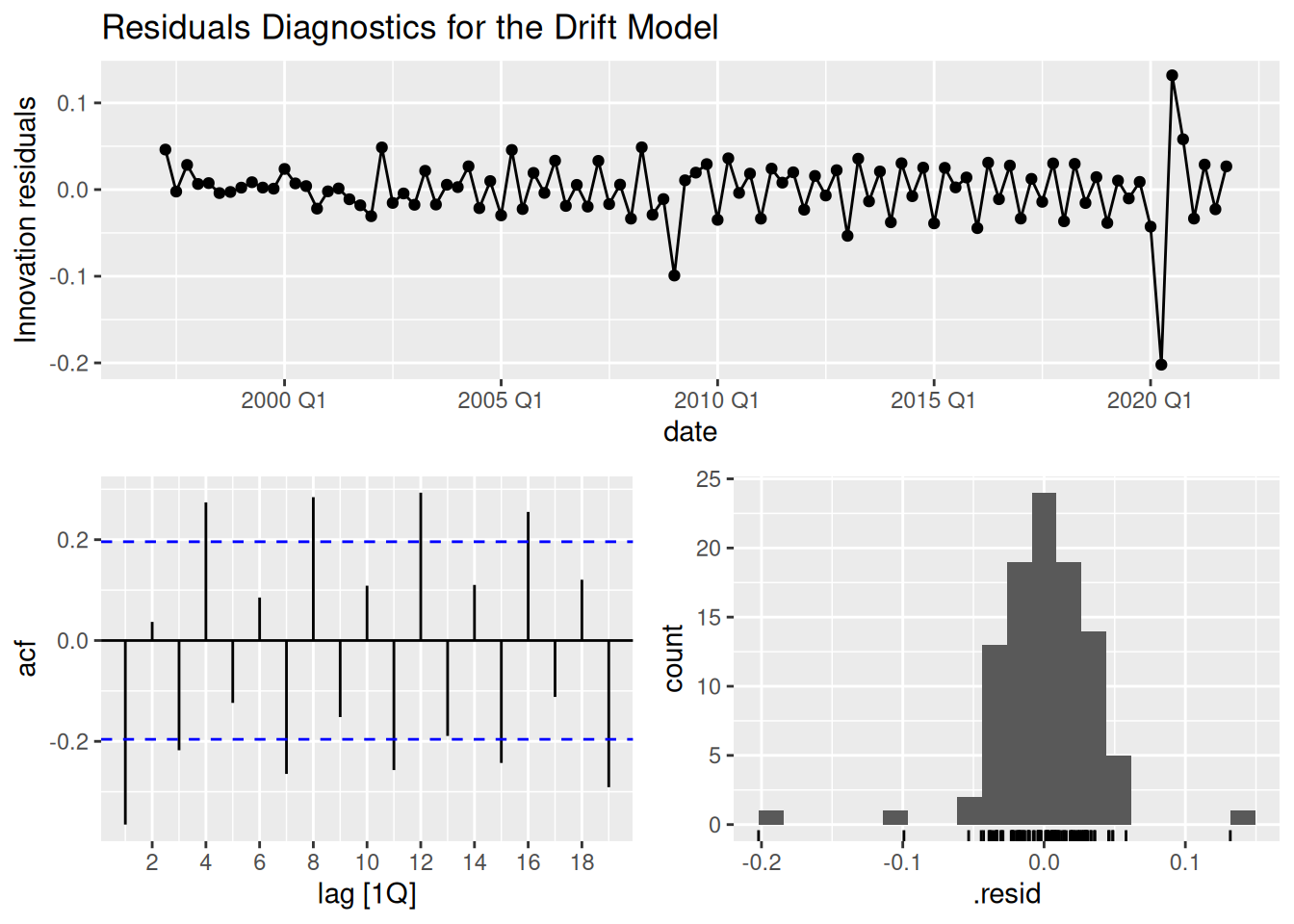

gdp_fit |>

select(drift) |>

gg_tsresiduals() +

ggtitle("Residuals Diagnostics for the Drift Model")

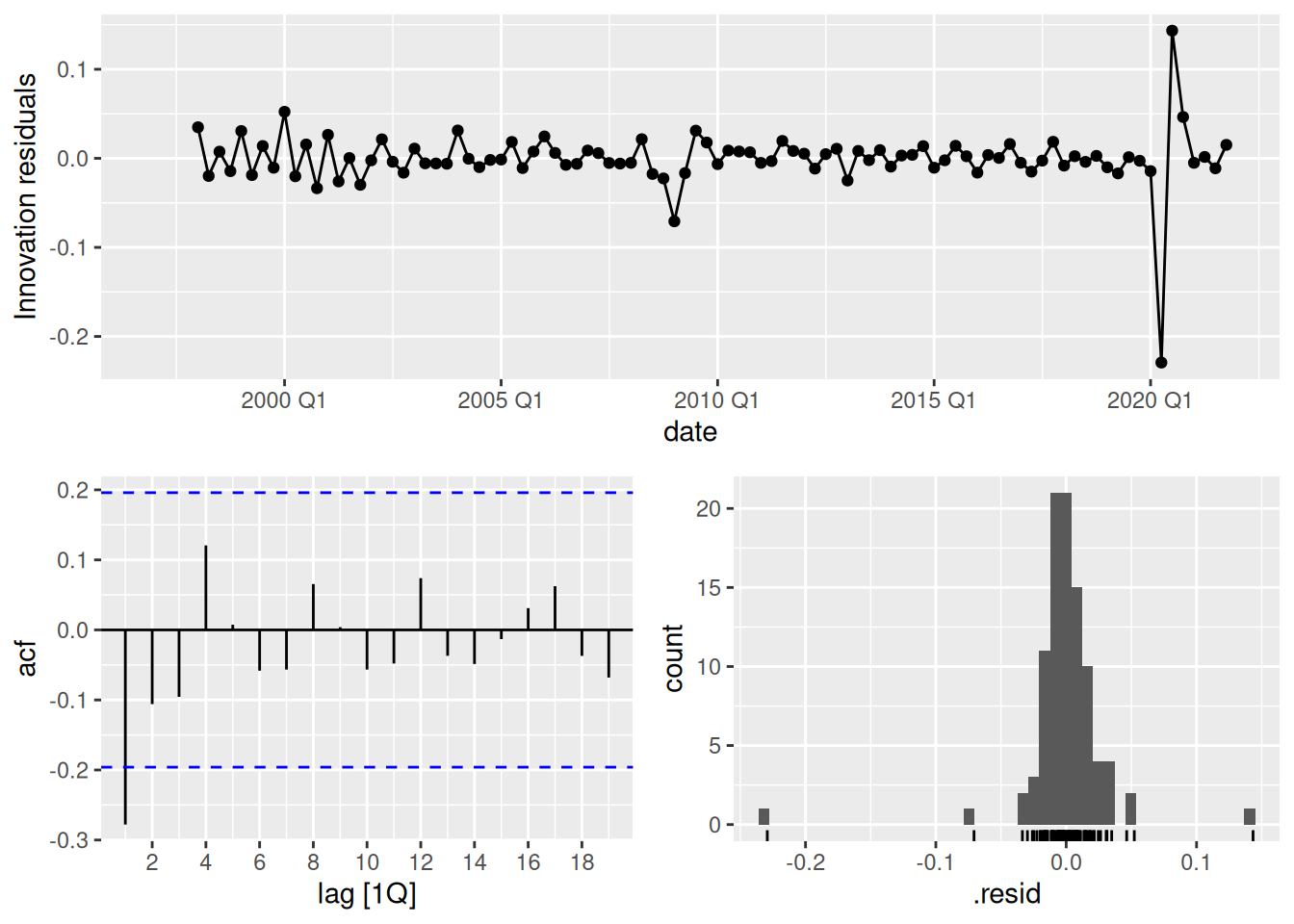

Here we expect to see:

gdp_fit |>

augment() |>

features(.innov, ljung_box, lag = 24, dof = 0)Both models produce sub optimal residuals:

The SNAIVE correctly detects the seasonality, however, its residuals are still autocorrelated. Moreover, the residuals are not normally distributed.

The drift model doesn’t account for the seasonality, and their distribution is a little bit skewed.

Hence, we will perform our forecasts using the bootstrapping method.

We can compute some error metrics on the training set using the accuracy() function:

gdp_train_accu <- accuracy(gdp_fit) |>

arrange(MAPE)

gdp_train_accu |>

select(symbol:.type, MAPE, RMSE, MAE, MASE)accuracy() function

The accuracy() function can be used to compute error metrics in the training data, or in the test set. What differs is the data that is given to it:

For the training metrics, you need to use the mable (the table of models, that we usually store in _fit).

For the forecasting error metrics, we need the fable (the forecasts table, usually stored as _fc or _fcst), and the complete set of data (both the training and test set together).

We will perform a forecast using decomposition, to see if we can improve our results so far.

gdp_fit_dcmp <- gdp_train |>

model(

stlf = decomposition_model(

STL(log(price) ~ season(window = "periodic"), robust = TRUE),

RW(season_adjust ~ drift())

)

)

gdp_fit_dcmpdecomposition_model()

Remember, when using decomposition models, we need to do the following:

Specify what type of decomposition we want to use and customize it as needed.

Fit a model for the seasonally adjusted data; season_adjust.

Fit a model for the seasonal component. R uses a SNAIVE() model by default to model the seasonality. If you wish to model it using a different model, you have specify it.

season_year. It could also be called season_week, season_day, and so on.We can join this new model with the models we trained before. This way we can have them all in the same mable.

gdp_fit <- gdp_fit |>

left_join(gdp_fit_dcmp)Joining with `by = join_by(symbol)`gdp_fit |>

accuracy() |>

select(symbol:.type, MAPE, RMSE, MAE, MASE) |>

arrange(MAPE)gdp_fit |>

select(stlf) |>

gg_tsresiduals()

gdp_fit |>

augment() |>

features(.innov, ljung_box)Once we have our models, we can produce forecasts. We will forecast our test data and check our forecasts’ performance.

gdp_fc <- gdp_fit |>

forecast(h = gdp_h_fc)

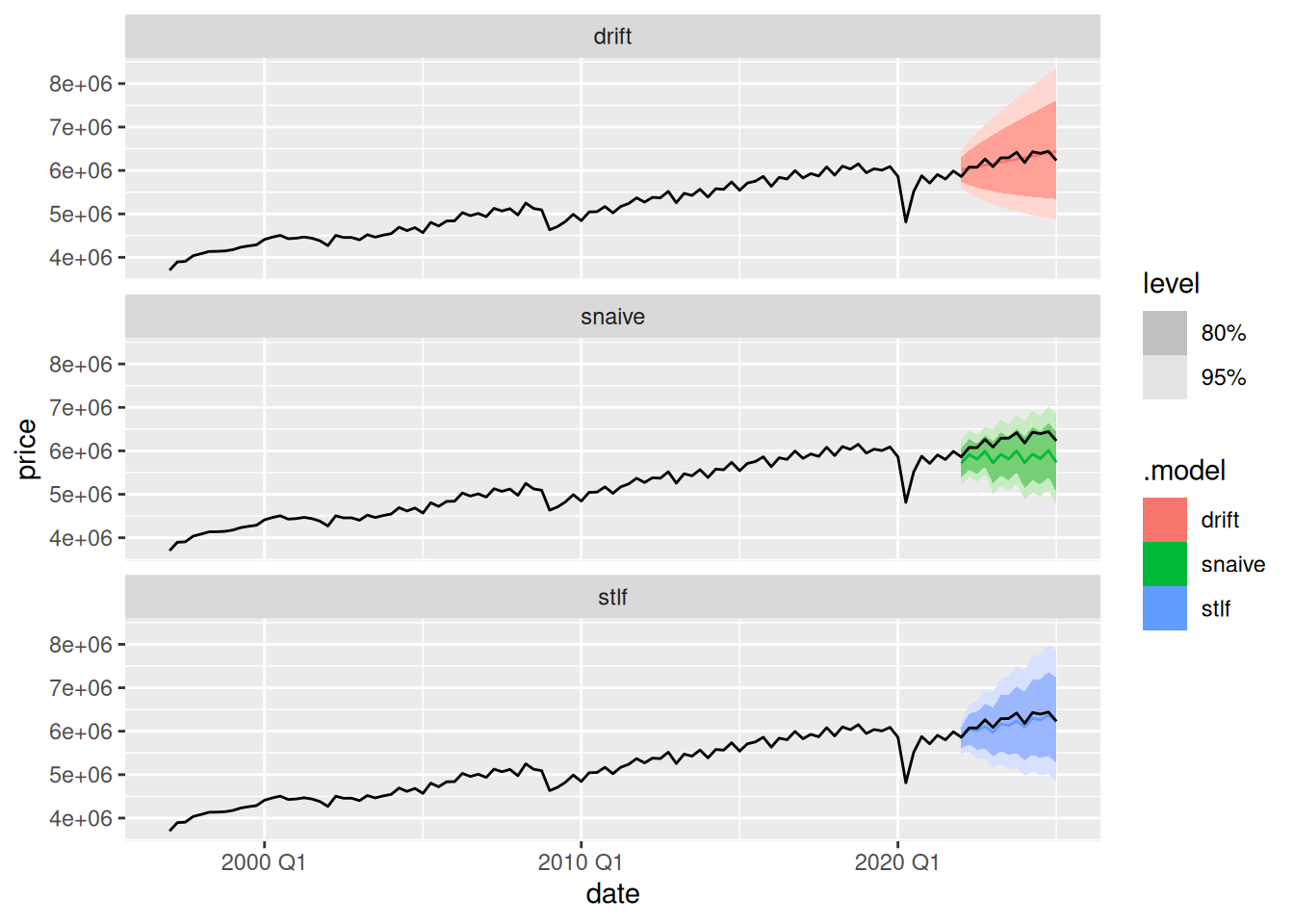

gdp_fcgdp_fc |>

autoplot(gdp) +

facet_wrap(~.model, ncol = 1)

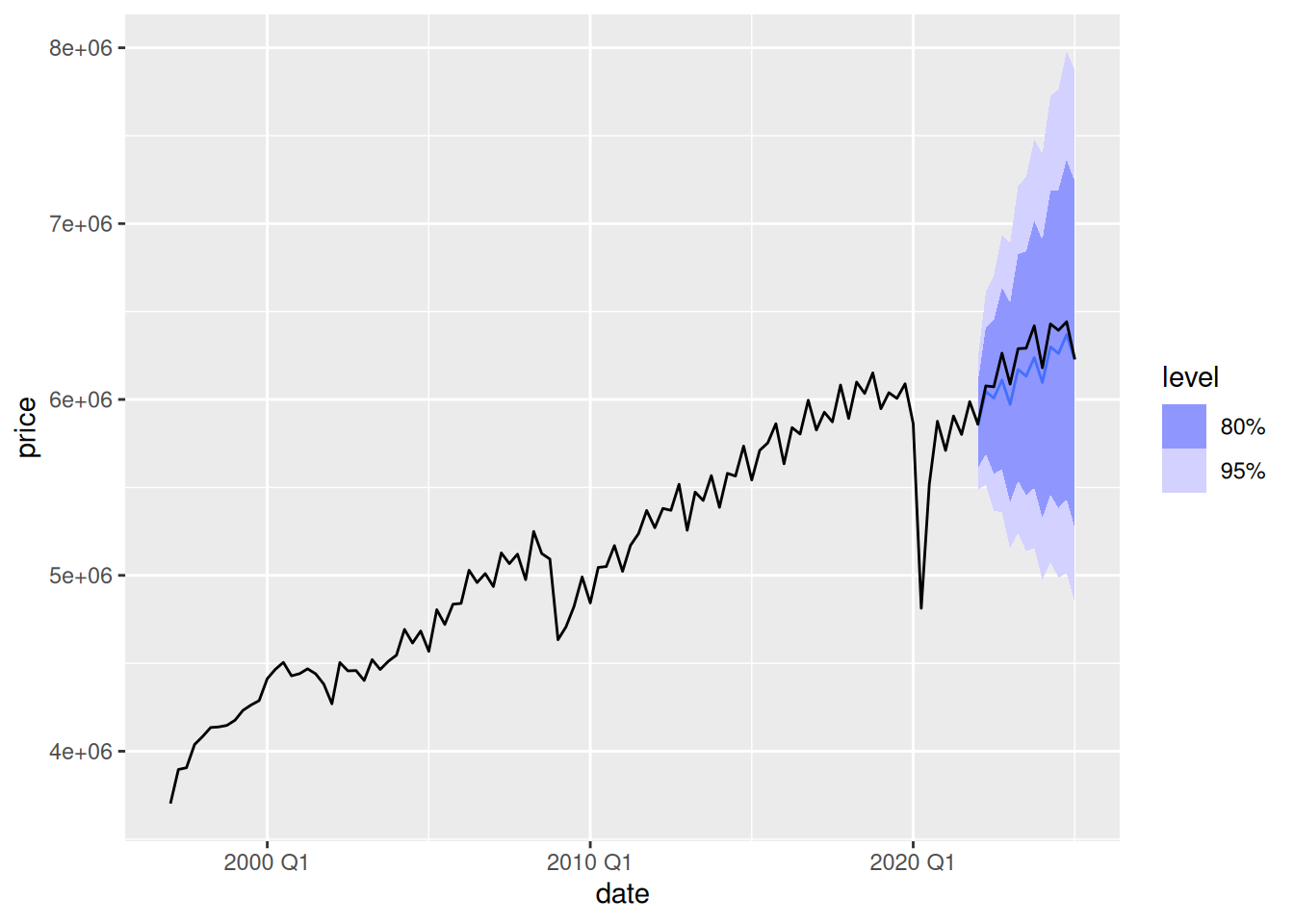

gdp_fc |>

filter(.model == "stlf") |>

autoplot(gdp)

We now estimate the forecast errors:

gdp_fc |>

accuracy(gdp) |>

select(.model:.type, MAPE, RMSE, MAE, MASE) |>

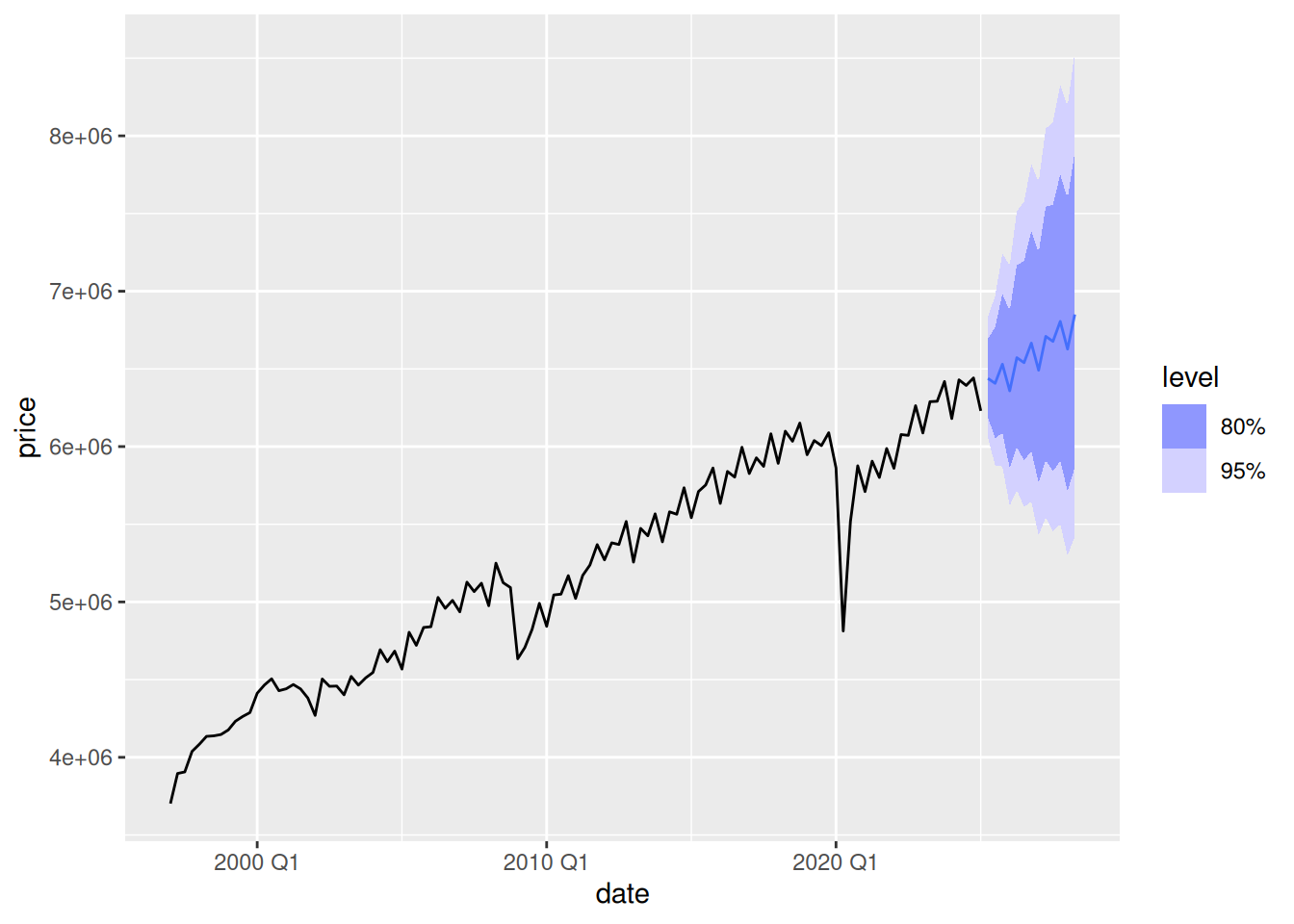

arrange(MAPE)We now refit our model using the whole dataset. We will only model the STL decomposition model, because the other two didn’t get a strong fit.

gdp_fit2 <- gdp |>

model(

stlf = decomposition_model(

STL(log(price) ~ season(window = "periodic"), robust = TRUE),

RW(season_adjust ~ drift())

)

)

gdp_fit2gdp_fc_fut <- gdp_fit2 |>

forecast(h = gdp_h_fc)

gdp_fc_futgdp_fc_fut |>

autoplot(gdp)

# save(gdp_fc_fut, file = "equipo1.RData")This will make it very convenient when calling your variables. RStudio will display all the options starting with gdp_. We will usually use the following suffixes:

_train: training set_fit: the mable (table of models)_aug: the augmented table with fitted values and residuals_dcmp: for the dable (decomposition table), containing the components and the seasonally adjusted series of a TS decomposition._fc or _fcst: for the fable (forecasts table) that has our forecasts.

The Mean Absolute Percentage Error is a percentage error metric widely used in professional environments.

Let

e_t = y_t - \hat{y}_t

be the error or residual.

Then the MAPE would be computed as

MAPE = \frac{1}{T}\sum_{t=1}^T|\frac{e_t}{y_t}| .