Code

1library(plotly)- 1

- For interactive plots with dynamic ticks and range sliders.

1library(plotly)Back in Module 3.3, we modeled electricity demand using daily aggregated data. Temperature explained the U-shaped relationship with demand, and day-type dummies captured the weekday/weekend pattern.

That model worked reasonably well — but it swept a fundamental problem under the rug: by aggregating to daily, we collapsed two distinct intra-day and intra-week cycles into a single, blunt average.

Daily demand is the sum of 48 half-hourly observations. When we aggregate, we lose:

These are not noise — they are real, structured, forecastable signal.

The vic_elec dataset records electricity demand in Victoria, Australia at 30-minute intervals, from 2012 to 2014. We aggregate to hourly to preserve meaningful temporal structure while keeping computation manageable:

floor_date(..., "hour") truncates each timestamp to the nearest hour, creating the grouping key.

WorkDay is TRUE for non-holiday weekdays — our main day-type predictor.

At half-hourly granularity, STL would estimate a “sub-hourly” seasonal component — a systematic difference between, say, 10:00 and 10:30. There is no physical or economic justification for that pattern. Hourly is the minimum granularity with a meaningful interpretation: the hour of the day captures real behavioral patterns (commutes, business hours, sleep cycles).

Key things to point out when exploring this plot:

Use the slider to zoom in on a single week. Two patterns emerge immediately:

Every model we have built so far assumes one seasonal period. STL takes a single season() call. ARIMA() with PDQ() handles one seasonal lag. season() dummies work for one cycle.

With m_1 = 24 and m_2 = 168, we need something different.

We can make both cycles visible using seasonal plots at each period:

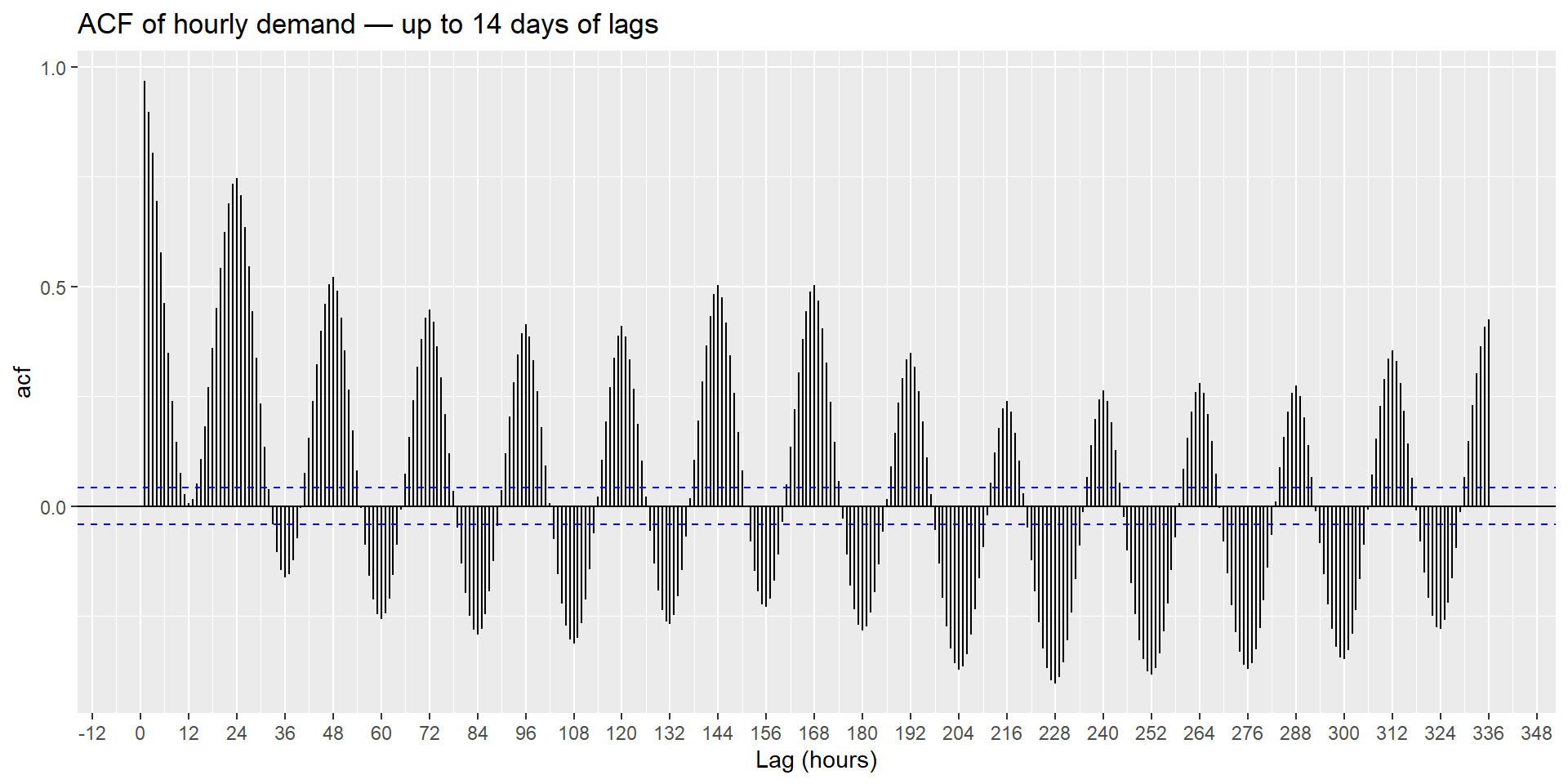

The ACF shows sharp peaks at multiples of 24 (daily cycle) and secondary peaks at multiples of 168 (weekly cycle). Both structures are strong enough to dominate the autocorrelation. A single-period ARIMA would capture at most one of them.

December in Victoria is early summer (Southern Hemisphere), meaning air conditioning load is ramping up — a genuinely challenging period to forecast and a more informative evaluation than a quiet shoulder season.

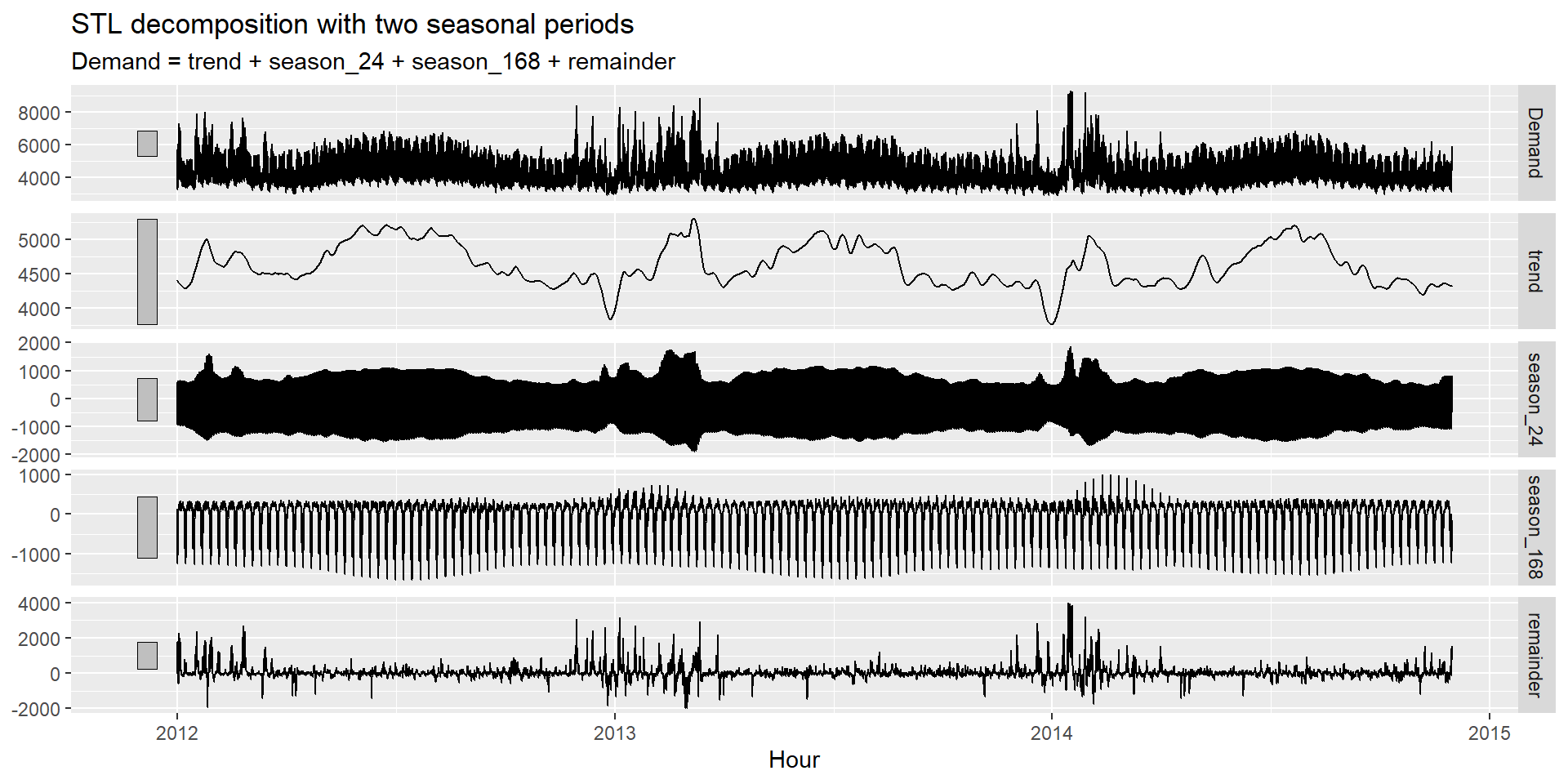

In Module 1, we used STL() to separate a single seasonal component from the trend-cycle. The same function supports multiple seasonal periods by stacking more than one season() call inside the formula:

STL(Demand ~ season(period = 24) + season(period = 168))Each seasonal component is estimated in sequence, holding the others fixed, until all converge. The result is one trend-cycle, one component per period, and a remainder.

STL() — the same function used in Module 1, now with two season() calls.

decomposition_model()Once we have the decomposition, we attach any univariate model to forecast the seasonally adjusted series — exactly as in Module 2:

season("N") suppresses any additional seasonal term — STL already removed both seasonal components.

PDQ(0,0,0) suppresses seasonal ARIMA terms for the same reason.

stl_fc <- stl_fit |>

forecast(h = nrow(vic_elec_test))STL is a powerful univariate tool. But electricity demand has an obvious external driver that STL cannot see: temperature. On hot days, air conditioning pushes demand up. On cold days, heating does the same. The U-shaped relationship we found in Module 3.3 is real and strong.

Harmonic regression (Fourier terms + ARIMA errors) can incorporate external predictors alongside the seasonal patterns. STL cannot. This is the key advantage when meaningful covariates are available.

Recall from Module 3.3 that Fourier terms approximate a seasonal pattern with K pairs of sine and cosine waves. For multiple seasonalities, we add one set per period:

y_t = \underbrace{S_{K_1}(t)}_{\text{daily, } m=24} + \underbrace{S_{K_2}(t)}_{\text{weekly, } m=168} + \beta^\top \mathbf{x}_t + \eta_t, \quad \eta_t \sim \text{ARIMA}

In fable, fourier() accepts a period argument and can be called multiple times in the same formula:

ARIMA(Demand ~

fourier(period = 24, K = K1) +

fourier(period = 168, K = K2) +

PDQ(0, 0, 0))The key parameter for each Fourier term is K — the number of sine/cosine pairs. A larger K produces a more flexible seasonal shape but adds more parameters. The standard approach is to minimize AIC_c.

The principled approach is to search over a grid of (K_1, K_2) combinations. This is computationally expensive for hourly data and is best run offline or with freeze: auto active. The code below illustrates the approach — it is not evaluated during render:

expand_grid(K1 = c(6, 8, 10, 12),

K2 = c(2, 4, 6, 8)) |>

mutate(

fit = map2(K1, K2, \(k1, k2)

vic_elec_train |>

model(ARIMA(Demand ~

fourier(period = 24, K = k1) +

fourier(period = 168, K = k2) +

PDQ(0, 0, 0),

stepwise = TRUE, approximation = TRUE))

),

aicc = map_dbl(fit, \(m) glance(m)$AICc)

) |>

select(K1, K2, aicc) |>

arrange(aicc)For vic_elec hourly data, K_1 = 10 and K_2 = 6 consistently perform well — they capture the main features of both seasonal patterns without overfitting. We use these values throughout.

Following FPP3, we model temperature with a piecewise linear function: a linear term plus a hockey-stick that activates above 18°C:

\text{Temp effect} = \beta_1 T_t + \beta_2 \max(T_t - 18,\; 0)

The intuition: below 18°C, demand increases as temperature falls (heating load). Above 18°C, demand increases as temperature rises (cooling load). The slope changes at the knot at 18°C.

fourier_fit <- vic_elec_train |>

model(

1 fourier_only = ARIMA(

Demand ~

fourier(period = 24, K = 10) +

fourier(period = 168, K = 6) +

PDQ(0, 0, 0),

stepwise = TRUE, approximation = TRUE

),

2 fourier_cov = ARIMA(

Demand ~

fourier(period = 24, K = 10) +

fourier(period = 168, K = 6) +

Temperature +

3 I(pmax(Temperature - 18, 0)) +

4 WorkDay +

PDQ(0, 0, 0),

stepwise = TRUE, approximation = TRUE

)

)pmax(Temperature - 18, 0) equals zero below 18°C and T - 18 above — the hockey-stick knot. I() protects the arithmetic inside the formula.

WorkDay captures the weekday demand premium beyond what the weekly Fourier terms already model.

18°C is a typical thermal comfort threshold for Melbourne’s climate — roughly the temperature above which mechanical cooling becomes widespread. FPP3 uses this same knot. It has a clear physical interpretation and works well empirically.

Adding temperature as a predictor immediately raises the challenge we faced in Module 3.3: to forecast demand, we need future temperature values.

Even with the piecewise linear temperature term, residuals of fourier_cov will show some remaining pattern linked to temperature extremes — particularly during heatwaves. The linear + hockey-stick approximation captures the average relationship but misses nonlinear tail behavior during extreme events.

This is a known limitation acknowledged in FPP3: electricity demand models with temperature covariates rarely achieve white-noise residuals. The residuals still carry information we have not fully captured.

For the forecast we use a scenario approach — constant temperature at 25°C (a mild early-summer day in Victoria):

fourier_fc <- fourier_fit |>

forecast(new_data = vic_elec_future)bind_rows(stl_fc, fourier_fc) |>

accuracy(vic_elec_hourly) |>

select(.model, RMSE, MAE, MAPE, MASE) |>

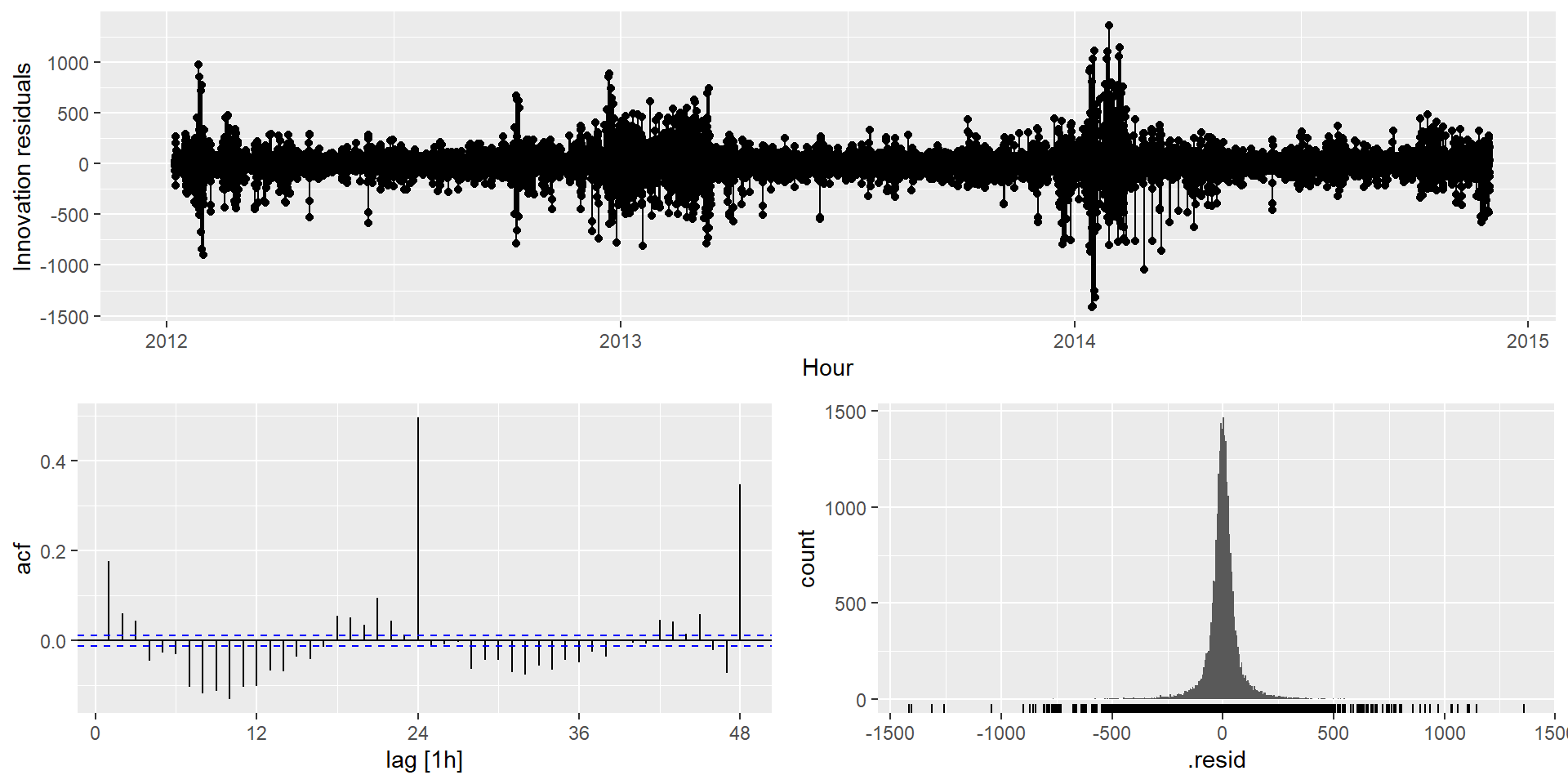

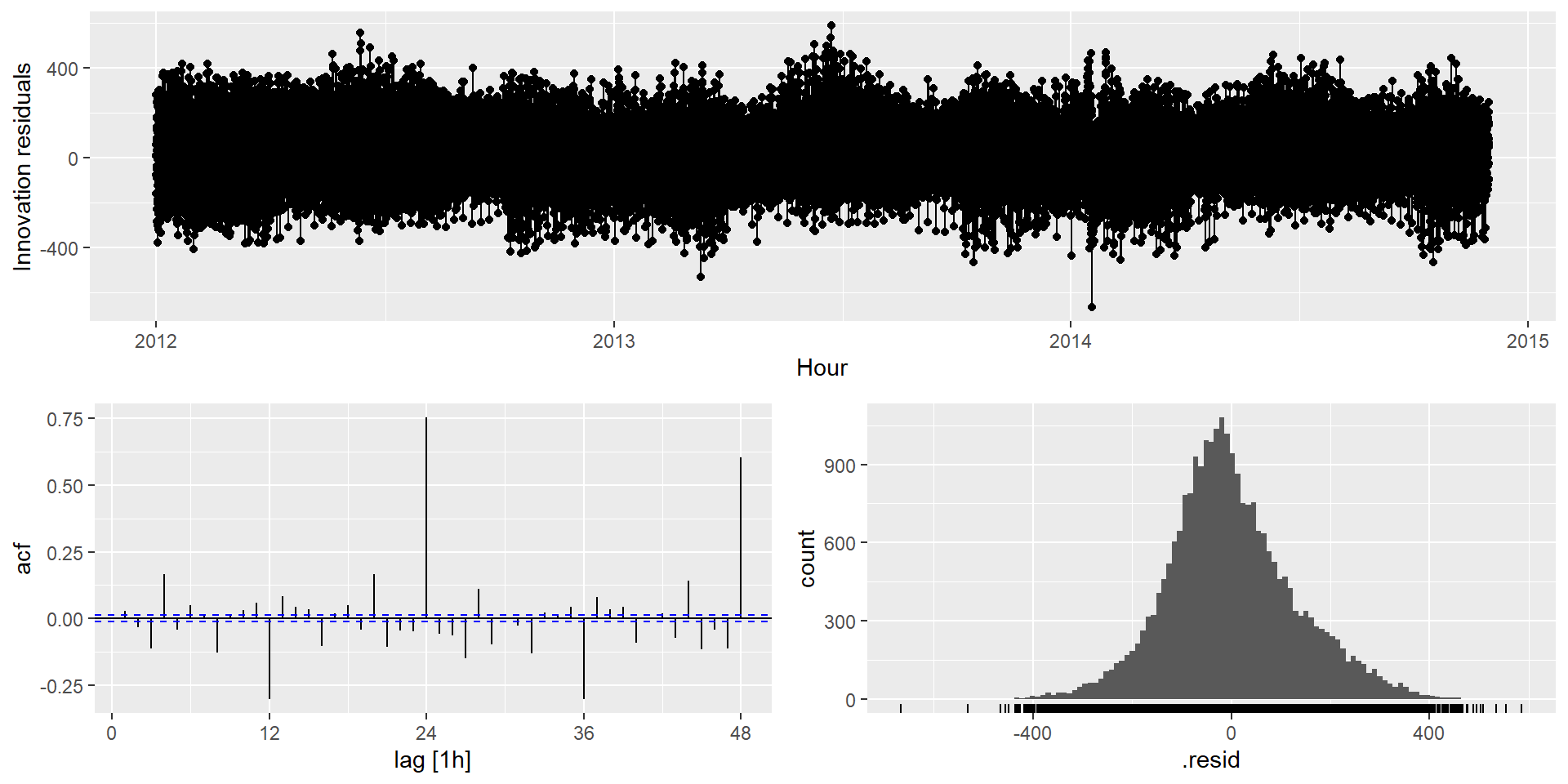

arrange(RMSE)stl_fit |>

select(STL_ETS) |>

gg_tsresiduals(lag_max = 48)

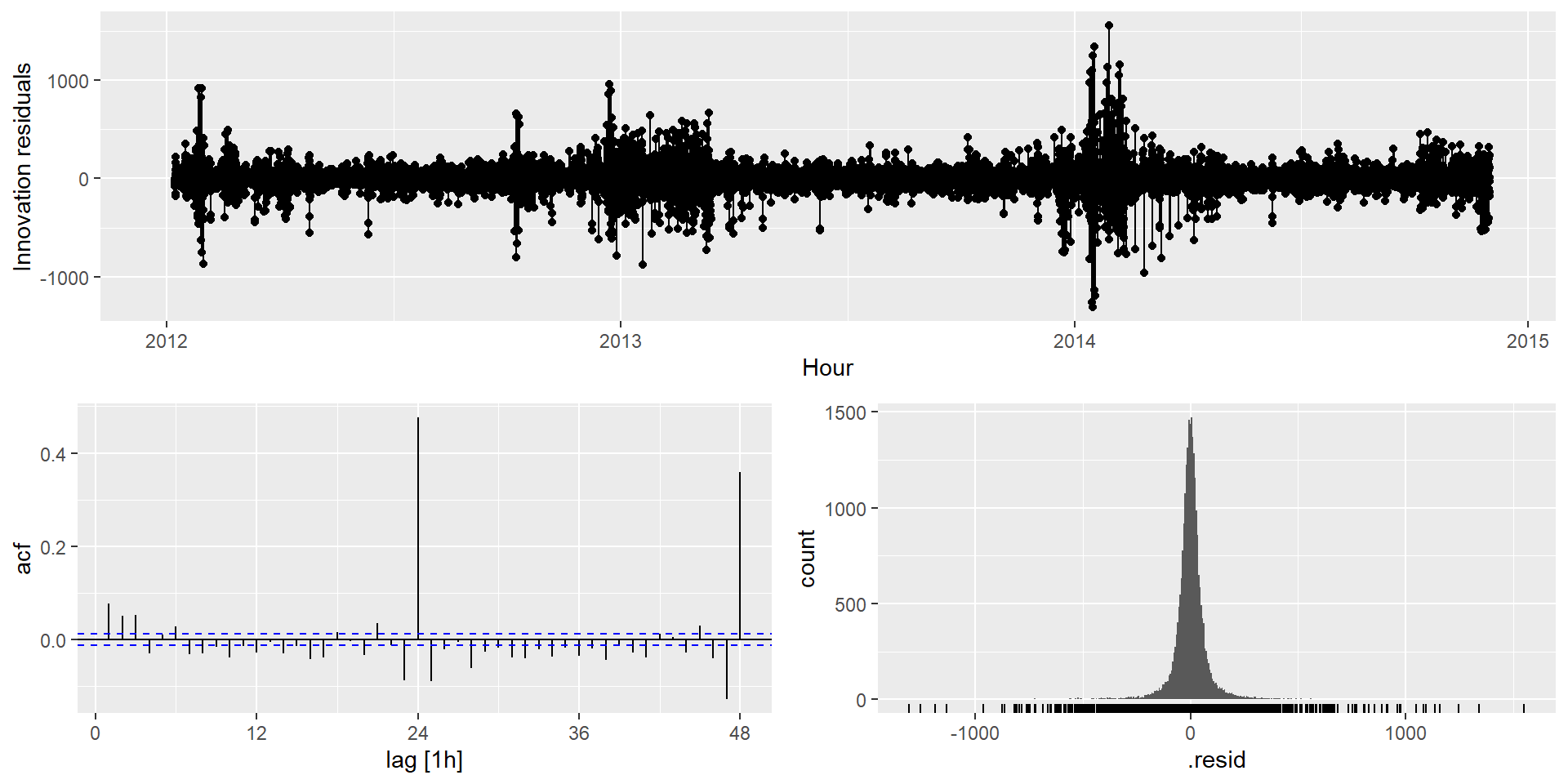

stl_fit |>

select(STL_ARIMA) |>

gg_tsresiduals(lag_max = 48)

fourier_fit |>

select(fourier_cov) |>

gg_tsresiduals(lag_max = 48)

| Situation | Recommended approach |

|---|---|

| No external predictors available | STL — clean, fast, interpretable decomposition |

| External predictors available and forecastable | Fourier + covariates — captures more signal |

| Predictors hard to forecast (e.g., spot temperatures) | STL or Fourier-only — avoid inheriting predictor uncertainty |

| Need interpretable components for stakeholders | STL — the decomposition plot is self-explanatory |

| Complex, irregular seasonality with holiday effects | Consider Prophet (Module 3.4) |

FPP3 mentions TBATS (Trigonometric seasonality, Box-Cox transformation, ARMA errors, Trend, Seasonal components) as another approach for complex seasonality. TBATS handles multiple seasonal periods and non-integer periods automatically.

However, TBATS is implemented in the older forecast package (forecast::tbats()), not in fable. Since we work exclusively within the fable / tidyverts ecosystem, we do not cover it in this course. The STL + Fourier combination achieves comparable results with a more transparent and modular workflow.

Curious? See ?forecast::tbats and FPP3 §12.1 for details.

The bank_calls dataset records the number of calls arriving at a North American commercial bank call centre, measured at 5-minute intervals over 33 weeks. This is a classic complex seasonality dataset with within-day and within-week structure — and an important twist: the call centre is closed overnight and on weekends.

bank_callsBegin by exploring bank_calls visually.

a) Use the plot above — zoom in on a single week and describe what you see in terms of daily and weekly patterns.

b) Create seasonal plots using gg_season() for the daily and weekly periods. What are the dominant features of each?

c) Plot the ACF up to at least 7 days of lags. At which lags do you see the strongest spikes?

At 5-minute intervals, one day has 12 \times 24 = 288 observations and one week has 288 \times 7 = 2{,}016 observations. Both should be visible in the ACF.

Note that the call centre is closed overnight and on weekends — this creates blocks of zeros that will dominate the decomposition if not handled carefully.

The 5-minute granularity is too fine for practical modeling.

a) Aggregate bank_calls to half-hourly frequency using index_by() and summarise(). Use sum() for calls.

b) Handle the overnight and weekend gaps. Are they true zeros (call centre closed) or missing values? Use fill_gaps() if needed and decide how to treat them in the model.

c) Create a train/test split reserving the last 2 weeks as the test set.

bank_calls has implicit gaps for overnight hours and weekends. Use fill_gaps(Calls = 0) before aggregating to make them explicit. Think carefully about whether your model should learn from these zeros or whether filtering them out makes more sense.

Fit at least two models to your training data:

a) An STL-based model with two season() calls for the daily and weekly periods. Use either ETS or ARIMA for the seasonally adjusted component.

b) A harmonic regression model (Fourier terms + ARIMA errors) with both periods. Start with K_1 = 6 for the daily period and K_2 = 3 for the weekly period, adjusting by AIC_c if you want to explore further.

c) Inspect residuals from both models using gg_tsresiduals(). Is there remaining autocorrelation? What does the ACF look like around lags 48 and 336?

For half-hourly data, the daily period is m_1 = 48 and the weekly period is m_2 = 336. Start with small K values and use stepwise = TRUE, approximation = TRUE inside ARIMA() — exact search over periods this large is very slow.

a) Generate 2-week-ahead forecasts from both models and compute accuracy metrics on the test set. Which model performs better?

b) Plot the forecasts overlaid on the test set. Does the model correctly capture the overnight shutdown and weekend pattern? What happens if it does not?

c) Reflection: bank_calls has no obvious external covariate like temperature. Does that make STL the natural choice here, or can you think of predictors that might be useful in a real deployment?

If your model produces non-zero forecasts during overnight and weekend hours, it does not know the call centre is closed. Consider adding an IsOpen binary indicator as a predictor, or filter out closed hours before modeling and evaluate only on open hours.

When a series has multiple seasonal periods, standard STL, ETS, and ARIMA models are not sufficient — they can handle at most one seasonal cycle cleanly.

STL with multiple season() calls extends the decomposition to an arbitrary number of periods, each estimated in sequence. Forecasting uses decomposition_model() with any univariate model for the seasonally adjusted series.

Harmonic regression (Fourier terms + ARIMA errors) handles multiple periods by including one set of Fourier terms per period in the formula. Its key advantage: external predictors can be added directly alongside the Fourier terms — something STL cannot do.

For electricity demand, temperature enters as a piecewise linear function with a knot at 18°C. Residuals may still carry temperature-linked structure near extremes — a known limitation of linear covariate approximations in demand modeling.

Choosing K for each Fourier period is done by AIC_c comparison. For long seasonal periods, use stepwise = TRUE, approximation = TRUE inside ARIMA() to keep computation manageable.

| Session | What we added | Key tool |

|---|---|---|

| 4.1 (now) | Multiple seasonal periods | STL + multiple seasons, Fourier terms |

| 4.2 | Robustness and forecast combinations | Bootstrapping, bagging |

| 4.3 | Robust evaluation | Time series cross-validation |

| 4.4 | Hierarchical structure | Reconciliation |