Code

1library(plotly)- 1

-

In addition to the regular packages, here we’ll use

plotlyfor interactive plots.

1library(plotly)plotly for interactive plots.

In the previous session, we built a multiple regression model for US consumption:

y_{t,\text{Cons.}} = \beta_0 + \beta_1 x_{t,\text{Inc.}} + \beta_2 x_{t,\text{Prod.}} + \beta_3 x_{t,\text{Sav.}} + \beta_4 x_{t,\text{Unemp.}} + \varepsilon_t

The model improved substantially over the simple version — \bar{R}^2 went from ~0.15 to ~0.75, and the residuals looked much closer to white noise.

But “much closer” is not the same as “white noise.” Let’s check:

us_change_fit_mult |>

augment() |>

features(.resid, ljung_box, lag = 10, dof = 5)The p-value is not zero, but in practice with real data there is nearly always some residual autocorrelation left after TSLM. And that matters:

If \varepsilon_t is autocorrelated, OLS is still unbiased — but standard errors are wrong, confidence intervals are wrong, and prediction intervals are wrong. The model is leaving structure on the table that could be captured.

The culprit is the white noise assumption on \varepsilon_t:

\varepsilon_t \overset{\text{iid}}{\sim} N(0, \sigma^2)

What if instead of forcing this, we modeled whatever autocorrelation remains?

| Model | Error term |

|---|---|

| TSLM | \varepsilon_t \overset{\text{iid}}{\sim} N(0,\sigma^2) — must be white noise |

| Dynamic regression | \eta_t \sim \text{ARIMA}(p,d,q) — can be autocorrelated |

Same predictors. Same regression structure. One assumption relaxed.

The dynamic regression model replaces the white noise error \varepsilon_t with \eta_t, which is allowed to follow an ARIMA process:

y_t = \beta_0 + \beta_1 x_{1,t} + \cdots + \beta_k x_{k,t} + \eta_t

\eta_t \sim \text{ARIMA}(p, d, q)(P, D, Q)_m

The model still has white noise — it just lives one level deeper. There are now two distinct error terms:

We diagnose the model using \hat{\varepsilon}_t, not \hat{\eta}_t.

Dynamic regression requires that both y_t and all predictors x_{k,t} are stationary. Check each variable with unit root tests before fitting.

When differencing is needed, there are two natural cases:

Model in levels — no variable requires differencing. The regression is fitted directly on the original (or transformed) series. This is the most common case when all variables are already stationary, as in us_change.

Model in differences — one or more variables need differencing to achieve stationarity. In this case, all variables are differenced simultaneously to keep the model internally consistent. Specifying pdq(d = 1) in ARIMA() does this automatically.

A closely related question is whether a trend in the data is deterministic (captured by a trend() term in TSLM — predictable, fixed slope) or stochastic (captured by differencing in ARIMA — the trend wanders randomly over time). In practice, stochastic trends are far more common in economic and business data. See FPP3 §10.1 for a detailed comparison with forecasting implications.

ARIMA() handles dynamic regression by simply adding predictors to the right-hand side of the formula — the same syntax as TSLM():

# TSLM — white noise errors assumed

TSLM(y ~ x1 + x2)

# Dynamic regression — ARIMA errors, order chosen automatically

ARIMA(y ~ x1 + x2)

# Model in differences: force differencing on all variables

ARIMA(y ~ x1 + x2 + pdq(d = 1))ARIMA() selects the error order automatically via AIC_c.

Series: Consumption

Model: LM w/ ARIMA(0,1,2) errors

Coefficients:

ma1 ma2 Income Production Savings Unemployment

-1.0882 0.1118 0.7472 0.0370 -0.0531 -0.2096

s.e. 0.0692 0.0676 0.0403 0.0229 0.0029 0.0986

sigma^2 estimated as 0.09588: log likelihood=-47.13

AIC=108.27 AICc=108.86 BIC=131.25We can extract both error types from the fitted model:

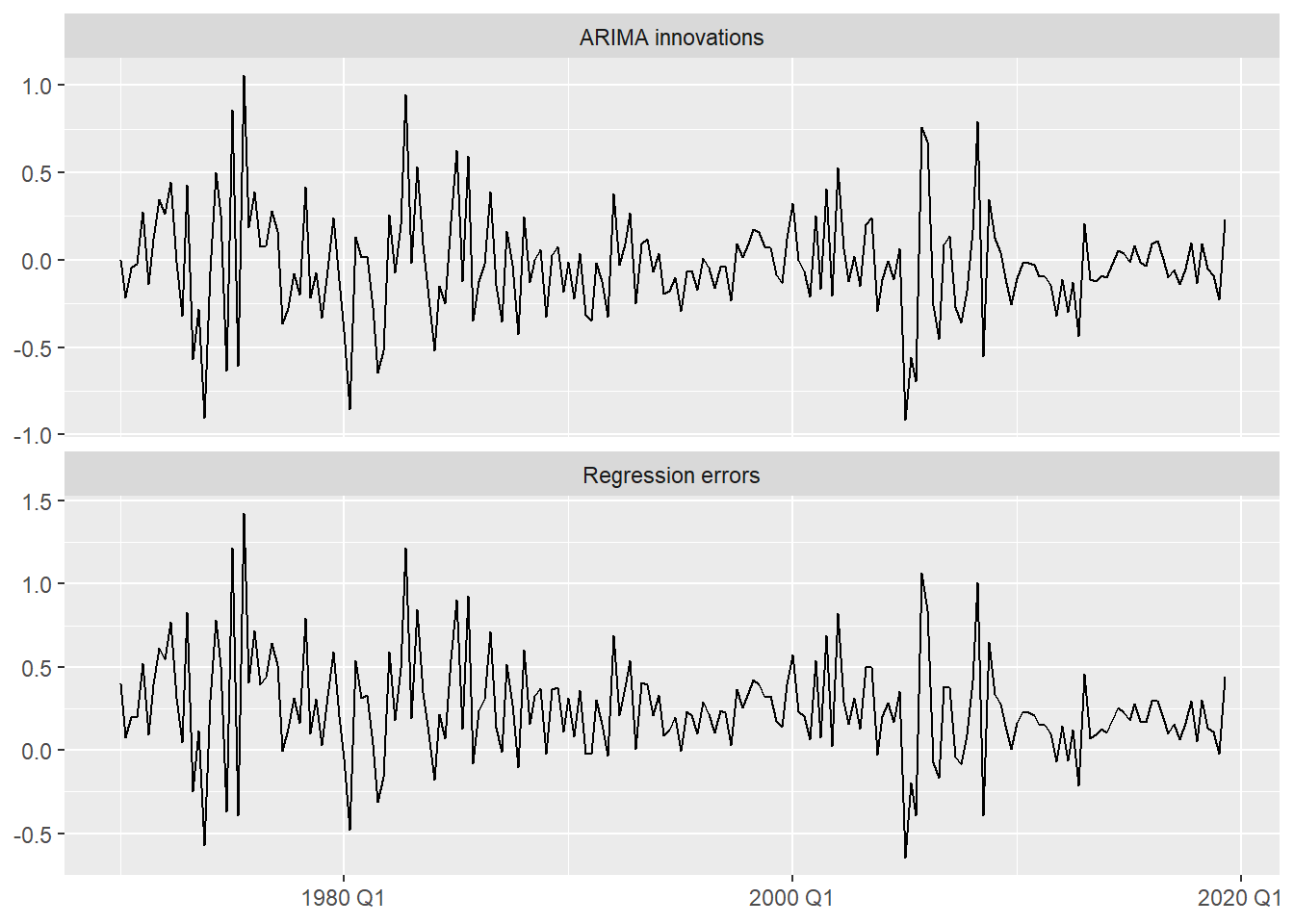

bind_rows(

1 `Regression errors` = as_tibble(

residuals(us_change_fit_dyn |> select(dynamic),

type = "regression")),

2 `ARIMA innovations` = as_tibble(

residuals(us_change_fit_dyn |> select(dynamic),

type = "innovation")),

.id = "type"

) |>

ggplot(aes(x = Quarter, y = .resid)) +

geom_line() +

facet_wrap(~ type, nrow = 2, scales = "free_y") +

labs(y = NULL, x = NULL)type = "regression" → \hat{\eta}_t: the regression residuals. These still have autocorrelation structure, now captured by the ARIMA component.

type = "innovation" → \hat{\varepsilon}_t: what should be white noise. This is what we diagnose.

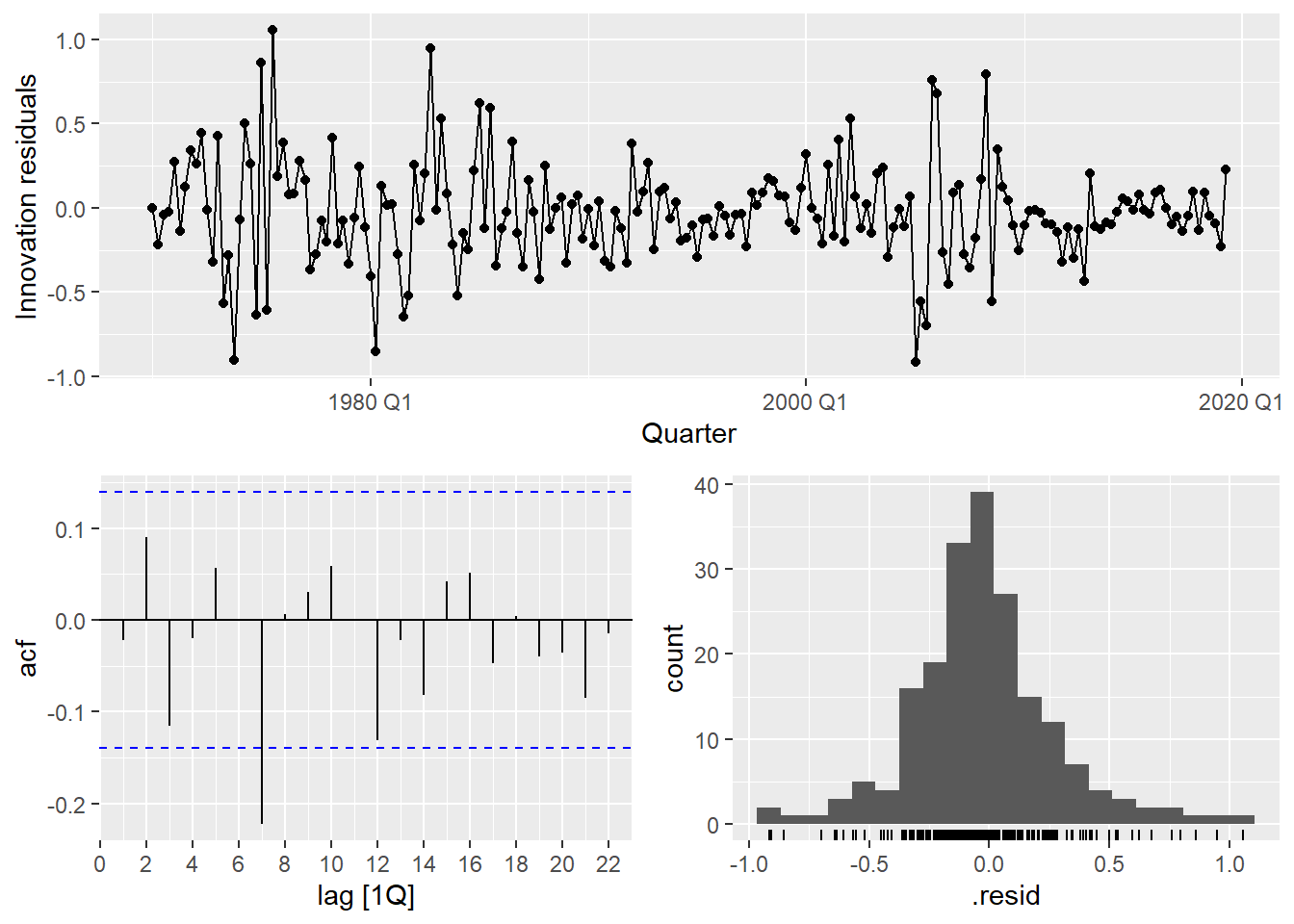

us_change_fit_dyn |>

select(dynamic) |>

gg_tsresiduals()

us_change_fit_dyn |>

select(dynamic) |>

augment() |>

features(.innov, ljung_box,

lag = 10,

1 dof = us_change_fit_dyn |>

select(dynamic) |>

coefficients() |>

filter(str_detect(term, "^ar|^ma")) |>

nrow())dof is computed dynamically as the number of estimated AR and MA coefficients — always matches the fitted model regardless of order selected.

Let’s compare the two models side by side on a held-out test set:

us_change_train <- us_change |> filter_index(. ~ "2015 Q4")

us_change_test <- us_change |> filter_index("2016 Q1" ~ .)

us_change_fit_cv <- us_change_train |>

model(

tslm = TSLM(Consumption ~ Income + Production + Savings + Unemployment),

dynamic = ARIMA(Consumption ~ Income + Production + Savings + Unemployment)

)

us_change_fit_cv |>

forecast(new_data = us_change_test) |>

accuracy(us_change_test) |>

select(.model, RMSE, MAE, MAPE)The dynamic regression model passes the Ljung-Box test — something the TSLM could not. By modeling the residual autocorrelation explicitly with ARIMA, we get valid standard errors, correct prediction intervals, and typically better out-of-sample accuracy.

Forecasting works exactly as in Session 3.2 — you still need future values of the predictors, and the same three strategies apply (ex-ante, ex-post, scenario-based).

The only practical difference: you use new_data() to build the future dataset and pass it to forecast(). The ARIMA component of the errors is projected forward automatically.

us_change_future <- us_change |>

1 pivot_longer(-c(Quarter, Consumption),

names_to = "variable") |>

2 model(MEAN(value)) |>

3 forecast(h = 8) |>

as_tsibble() |>

select(-c(.model, value)) |>

4 pivot_wider(names_from = variable,

values_from = .mean)

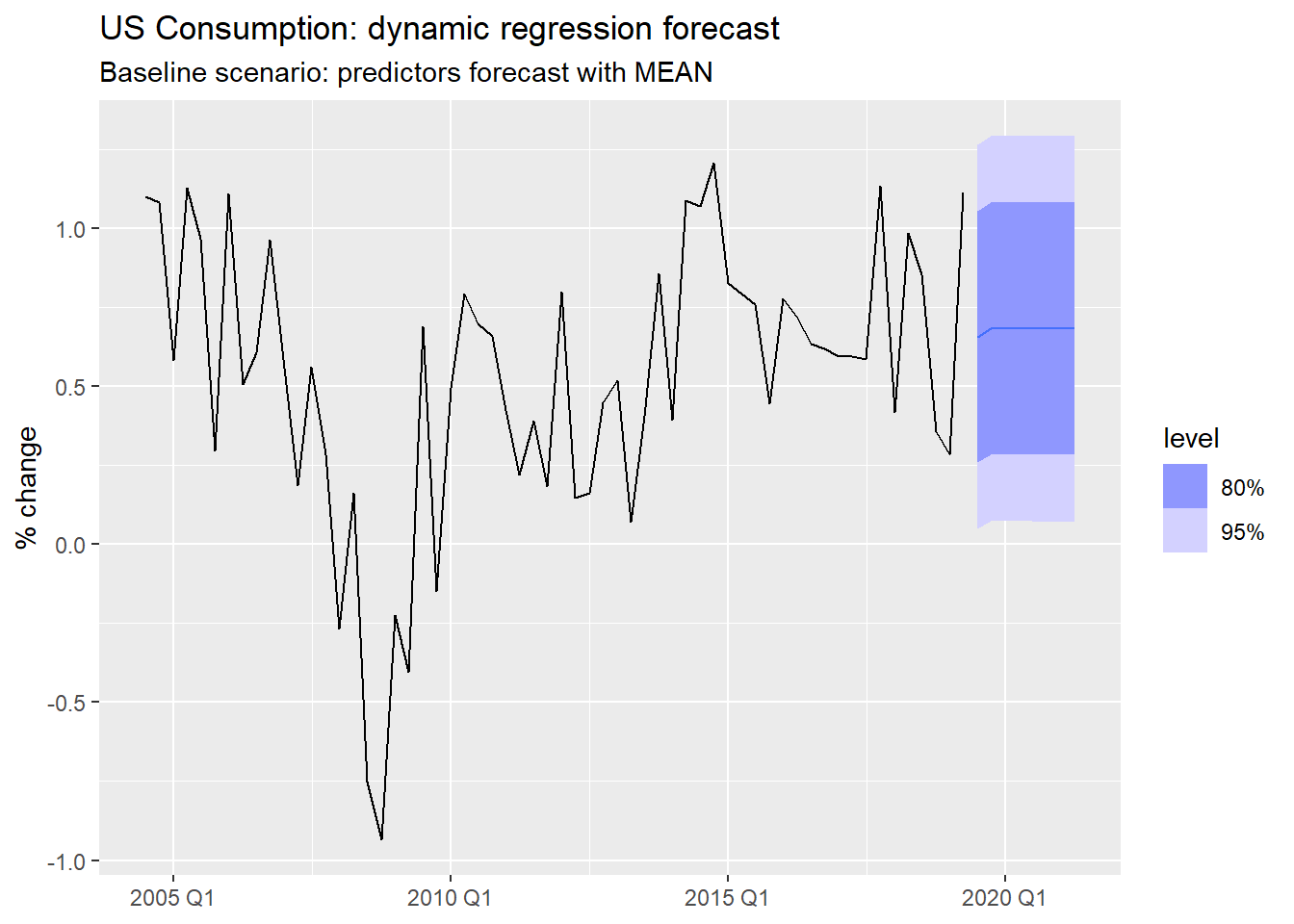

us_change_fit_dyn |>

select(dynamic) |>

forecast(new_data = us_change_future) |>

autoplot(tail(us_change, 60)) +

labs(

title = "US Consumption: dynamic regression forecast",

subtitle = "Baseline scenario: predictors forecast with MEAN",

y = "% change", x = NULL

)variable.

model() call fits MEAN to each predictor simultaneously.

forecast() produces 8-step-ahead forecasts for all predictors at once.

forecast() expects in new_data.

Because the predictors go through a proper model() |> forecast() pipeline, changing the scenario is a one-word edit:

model(MEAN(value)) # flat forecast at the historical mean

model(NAIVE(value)) # last observed value carried forward

model(RW(value ~ drift())) # linear extrapolation of the recent trend

model(ARIMA(value)) # best ARIMA for each predictorMEAN is appropriate here because all us_change variables are stationary percentage changes — the historical mean is a reasonable “neutral” projection. For predictors with trend, RW(drift) or ARIMA would be more honest.

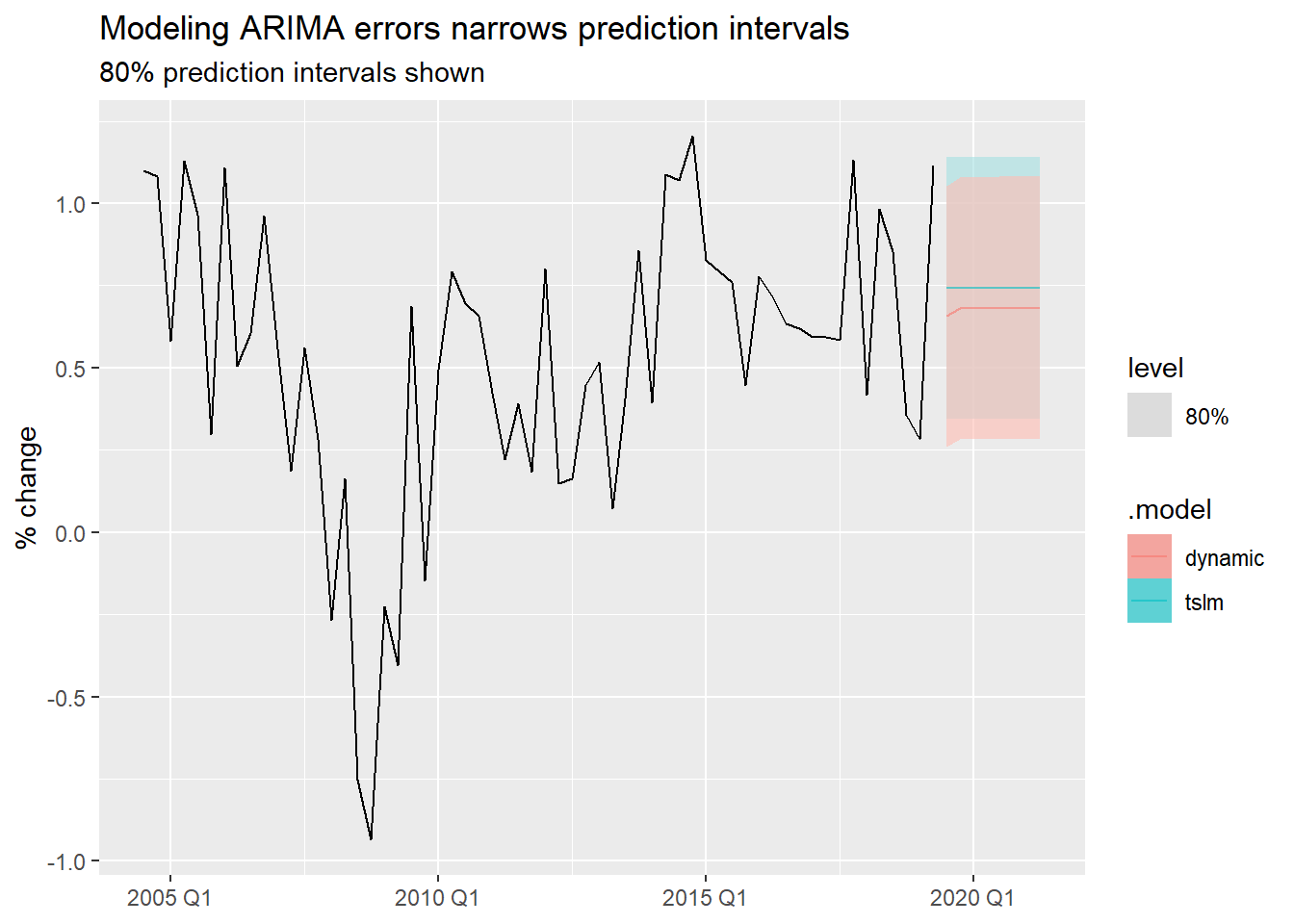

us_change_fit_dyn |>

forecast(new_data = us_change_future) |>

1 autoplot(tail(us_change, 60), level = 80, alpha = 0.6) +

labs(

title = "Modeling ARIMA errors narrows prediction intervals",

subtitle = "80% prediction intervals shown",

y = "% change", x = NULL

)

Dynamic regression intervals assume future predictor values are known exactly. When they are estimated (as in the scenario above), true uncertainty is larger than what the intervals show. This applies equally to TSLM — dynamic regression does not make this problem worse, it just fixes the autocorrelation problem.

The us_change example was clean: stationary series, linear relationship. Electricity demand pushes two things further:

Daily electricity demand in Victoria, Australia (2014):

Two patterns are immediately clear:

This gives us the model:

y_t = \beta_0 + \beta_1 T_t + \beta_2 T_t^2 + \beta_3 D_{\text{day type}} + \eta_t, \quad \eta_t \sim \text{ARIMA}

I(Temperature^2) adds the quadratic term. The I() wrapper is required to protect arithmetic inside the formula.

TRUE (1) for weekdays, FALSE (0) otherwise.

Series: Demand

Model: LM w/ ARIMA(2,1,2)(2,0,0)[7] errors

Coefficients:

ar1 ar2 ma1 ma2 sar1 sar2 Temperature

-0.1093 0.7226 -0.0182 -0.9381 0.1958 0.4175 -7.6135

s.e. 0.0779 0.0739 0.0494 0.0493 0.0525 0.0570 0.4482

I(Temperature^2) Day_Type == "Weekday"TRUE

0.1810 30.4040

s.e. 0.0085 1.3254

sigma^2 estimated as 44.91: log likelihood=-1206.11

AIC=2432.21 AICc=2432.84 BIC=2471.18The choice of how to encode day type depends on the question you want to answer:

Day_Type == "Weekday": distinguishes working days from non-working days (weekends + holidays collapsed together). Simpler, fewer parameters, often sufficient.Day_Type == "Weekday" and Day_Type == "Weekend" (holidays as baseline): allows weekends and holidays to have different demand profiles. Useful if your data shows a meaningful difference between the two.Neither is universally better — let residual diagnostics and AIC_c guide the choice.

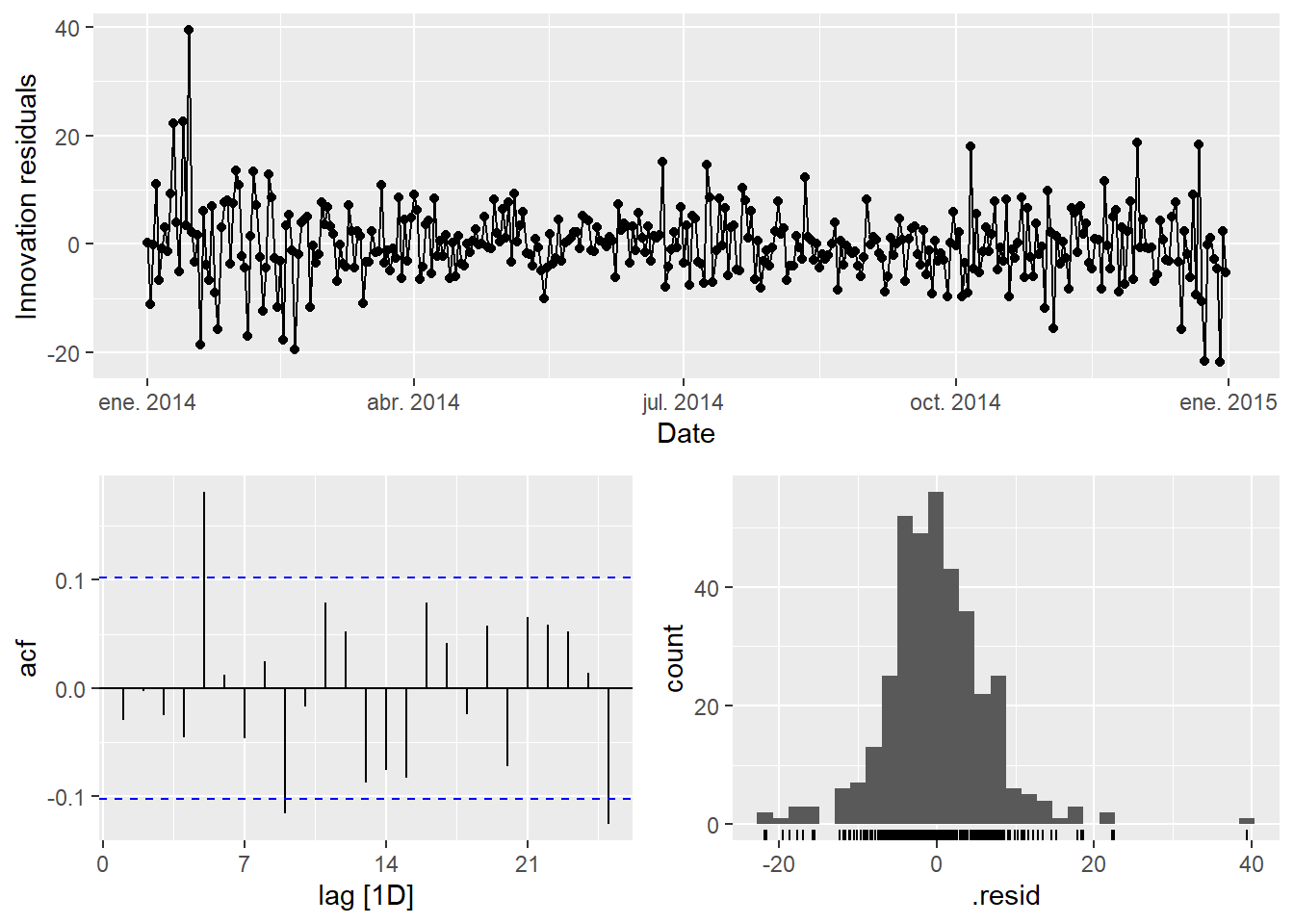

vic_elec_fit |> gg_tsresiduals()

vic_elec_fit |>

augment() |>

features(.innov, ljung_box, dof = 8, lag = 14)Variance is higher during January–February (Australian summer peak). Point estimates remain valid, but prediction intervals may be too narrow for extreme temperature periods.

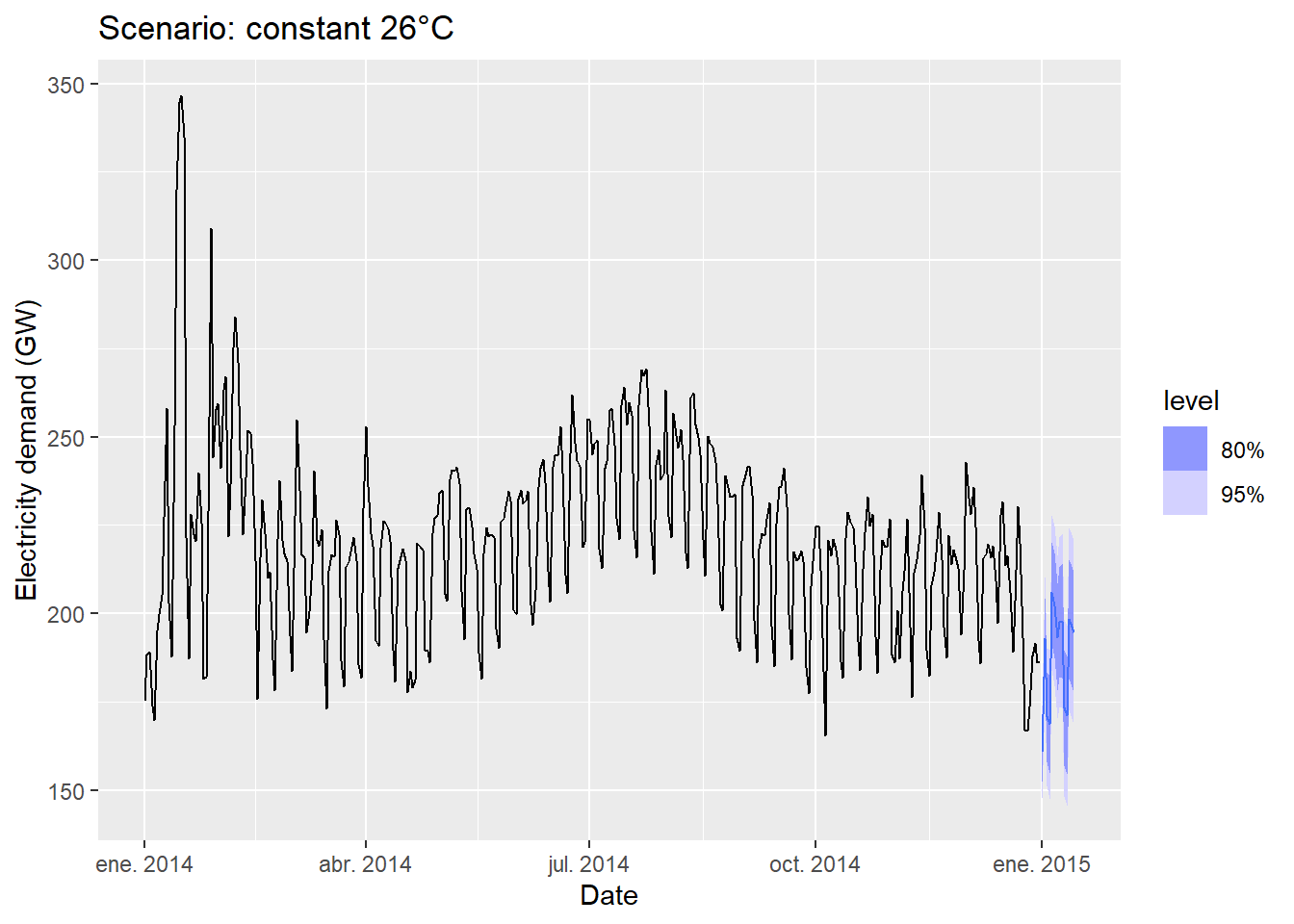

vic_elec_future_26 <- new_data(vic_elec_daily, 14) |>

mutate(

Temperature = 26,

Holiday = c(TRUE, rep(FALSE, 13)),

Day_Type = case_when(

Holiday ~ "Holiday",

wday(Date) %in% 2:6 ~ "Weekday",

TRUE ~ "Weekend"

)

)

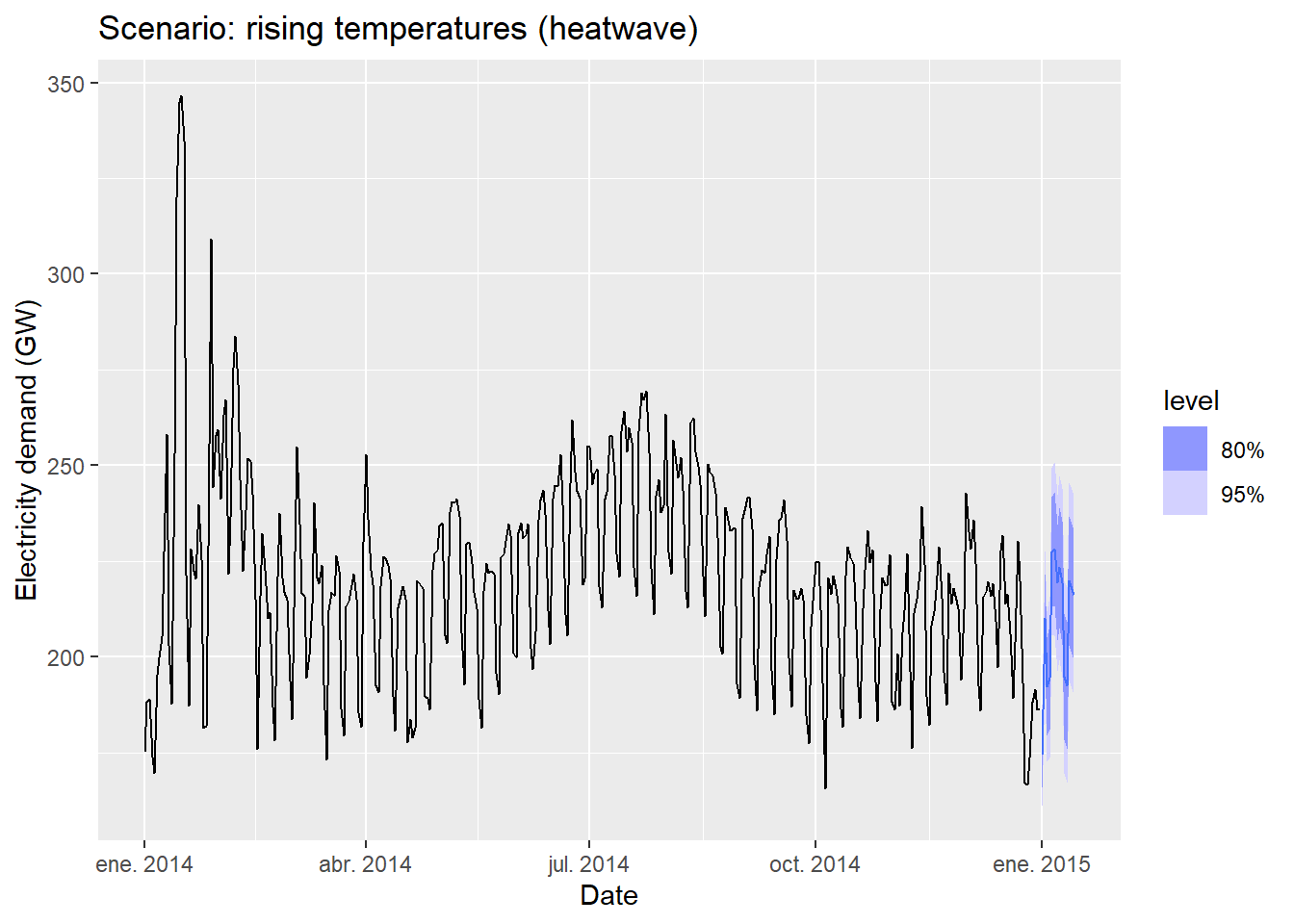

vic_elec_future_hw <- new_data(vic_elec_daily, 14) |>

mutate(

1 Temperature = c(seq(31, 34), 33, rep(34, 3), rep(33, 6)),

Holiday = c(TRUE, rep(FALSE, 13)),

Day_Type = case_when(

Holiday ~ "Holiday",

wday(Date) %in% 2:6 ~ "Weekday",

TRUE ~ "Weekend"

)

)

So far we have assumed that the predictor x_t affects y_t at the same point in time. But many real-world relationships have a delay: the cause happens now, the effect shows up later.

Models that include x_t at multiple lags are called distributed lag models:

y_t = \beta_0 + \delta_0 x_t + \delta_1 x_{t-1} + \delta_2 x_{t-2} + \cdots + \delta_k x_{t-k} + \eta_t

Each \delta_j captures the effect of x that occurs j periods after the predictor.

The fpp3 package includes the insurance dataset: monthly US insurance quotes (a proxy for sales) and TV advertising expenditure:

We fit four models with increasing lag depth to find how long the advertising effect persists:

insurance_fit <- insurance |>

model(

1 lag0 = ARIMA(Quotes ~ pdq(d = 0) +

TVadverts),

lag1 = ARIMA(Quotes ~ pdq(d = 0) +

2 TVadverts + lag(TVadverts)),

lag2 = ARIMA(Quotes ~ pdq(d = 0) +

TVadverts + lag(TVadverts) +

3 lag(TVadverts, 2)),

lag3 = ARIMA(Quotes ~ pdq(d = 0) +

TVadverts + lag(TVadverts) +

lag(TVadverts, 2) + lag(TVadverts, 3))

)

glance(insurance_fit) |>

select(.model, AICc) |>

arrange(AICc)pdq(d = 0) fixes the differencing order to zero — both series are stationary.

lag(TVadverts) is x_{t-1}: advertising from the previous month.

lag(TVadverts, 2) is x_{t-2}: advertising from two months ago.

insurance_fit |>

select(lag1) |>

report()Series: Quotes

Model: LM w/ ARIMA(1,0,2) errors

Coefficients:

ar1 ma1 ma2 TVadverts lag(TVadverts) intercept

0.5123 0.9169 0.4591 1.2527 0.1464 2.1554

s.e. 0.1849 0.2051 0.1895 0.0588 0.0531 0.8595

sigma^2 estimated as 0.2166: log likelihood=-23.94

AIC=61.88 AICc=65.38 BIC=73.7The coefficient on TVadverts (\delta_0) is the immediate effect: one unit increase in advertising this month increases quotes by \delta_0 units this month.

The coefficient on lag(TVadverts) (\delta_1) is the one-period carry-over: the additional effect that arrives one month later.

Together, the total effect of a sustained 1-unit increase in advertising is \delta_0 + \delta_1 + \cdots — the sum of all lag coefficients.

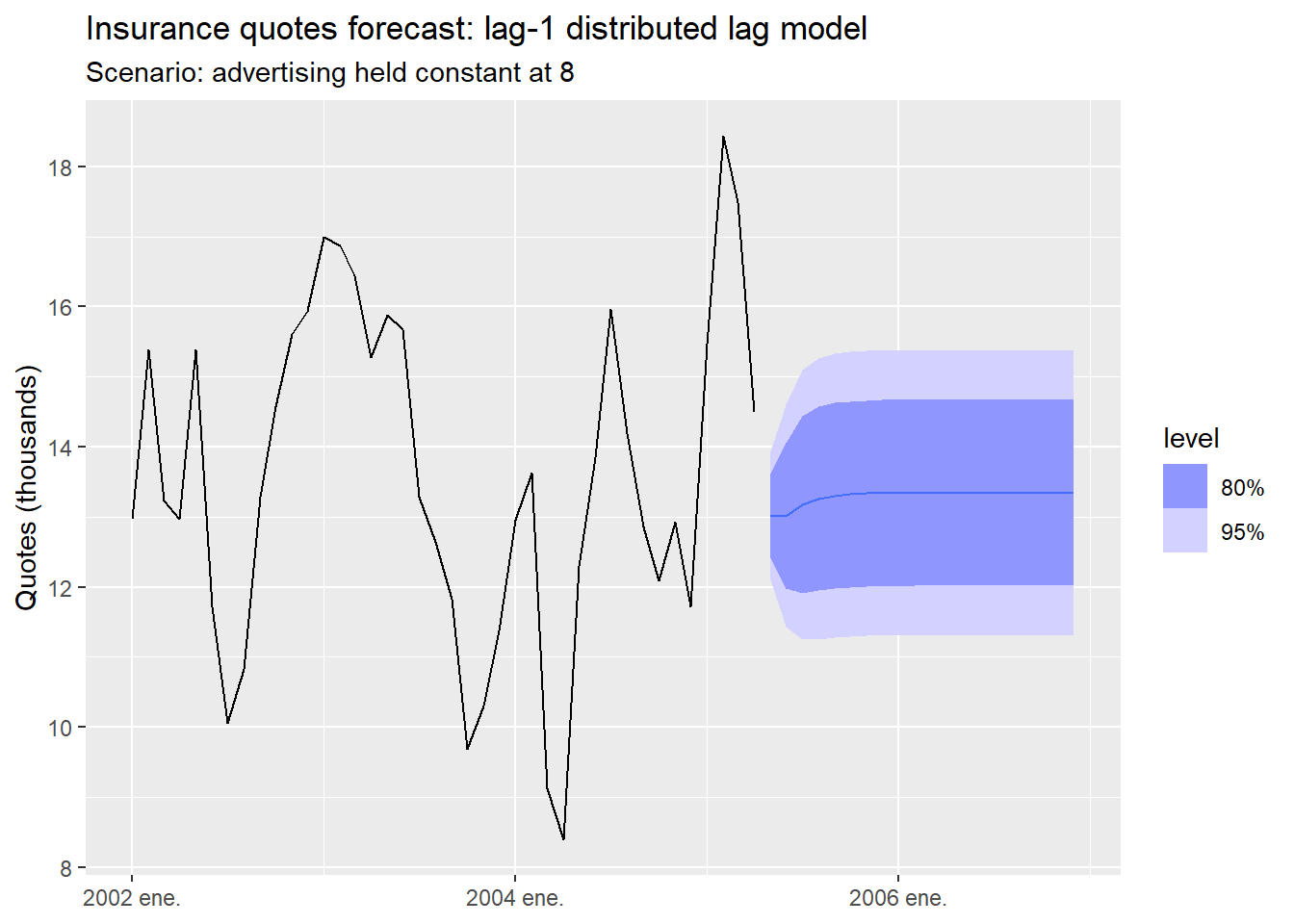

When forecasting, you need future values of x_t and the most recent observed values of x to fill in the lags:

insurance_future <- new_data(insurance, 20) |>

1 mutate(TVadverts = 8)

insurance_fit |>

select(lag1) |>

forecast(new_data = insurance_future) |>

autoplot(insurance) +

labs(title = "Insurance quotes forecast: lag-1 distributed lag model",

subtitle = "Scenario: advertising held constant at 8",

y = "Quotes (thousands)", x = NULL)

| Situation | Prefer |

|---|---|

| Effect is immediate (prices, temperature) | Current x_t |

| Effect has a known delay (advertising, policy) | x_t + lags |

| Delay length is unknown | Fit models with 0, 1, 2, … lags and compare with AIC_c |

| Predictor is hard to forecast | Lags are known at forecast time — a practical advantage |

The last point is important: if x_t is hard to forecast, using x_{t-k} instead means the predictor is already observed when you need to make the forecast. Lags can turn an ex-ante problem into an ex-post one.

The electricity demand example above used daily data. Demand has an obvious annual seasonal pattern (m = 365). If we wanted to capture it with dummy variables, we would need 364 of them.

That is impractical. The same problem appears with:

| Data frequency | Seasonal period |

|---|---|

| Daily (annual cycle) | m = 365 |

| Weekly | m = 52 |

| Half-hourly (daily cycle) | m = 48 |

We first saw Fourier terms mentioned as a footnote in regression.qmd — they were promised as the solution for large m. This is where we deliver on that promise.

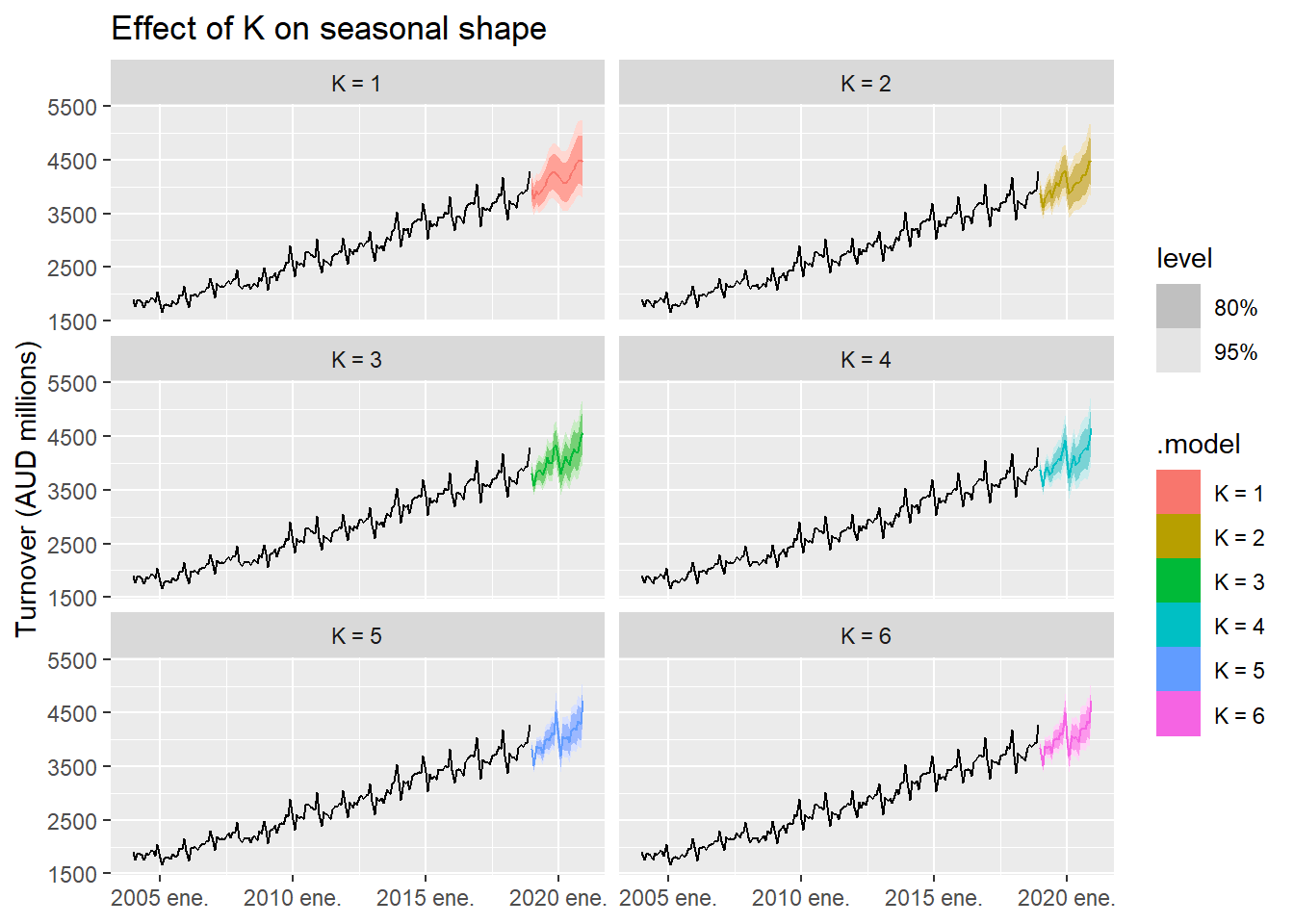

Any periodic pattern can be approximated by a sum of sine and cosine waves:

S_K(t) = \sum_{k=1}^{K} \left[ a_k \cos\!\left(\frac{2\pi k t}{m}\right) + b_k \sin\!\left(\frac{2\pi k t}{m}\right) \right]

Choose K by minimizing AIC_c.

Advantages over seasonal dummies:

Limitations:

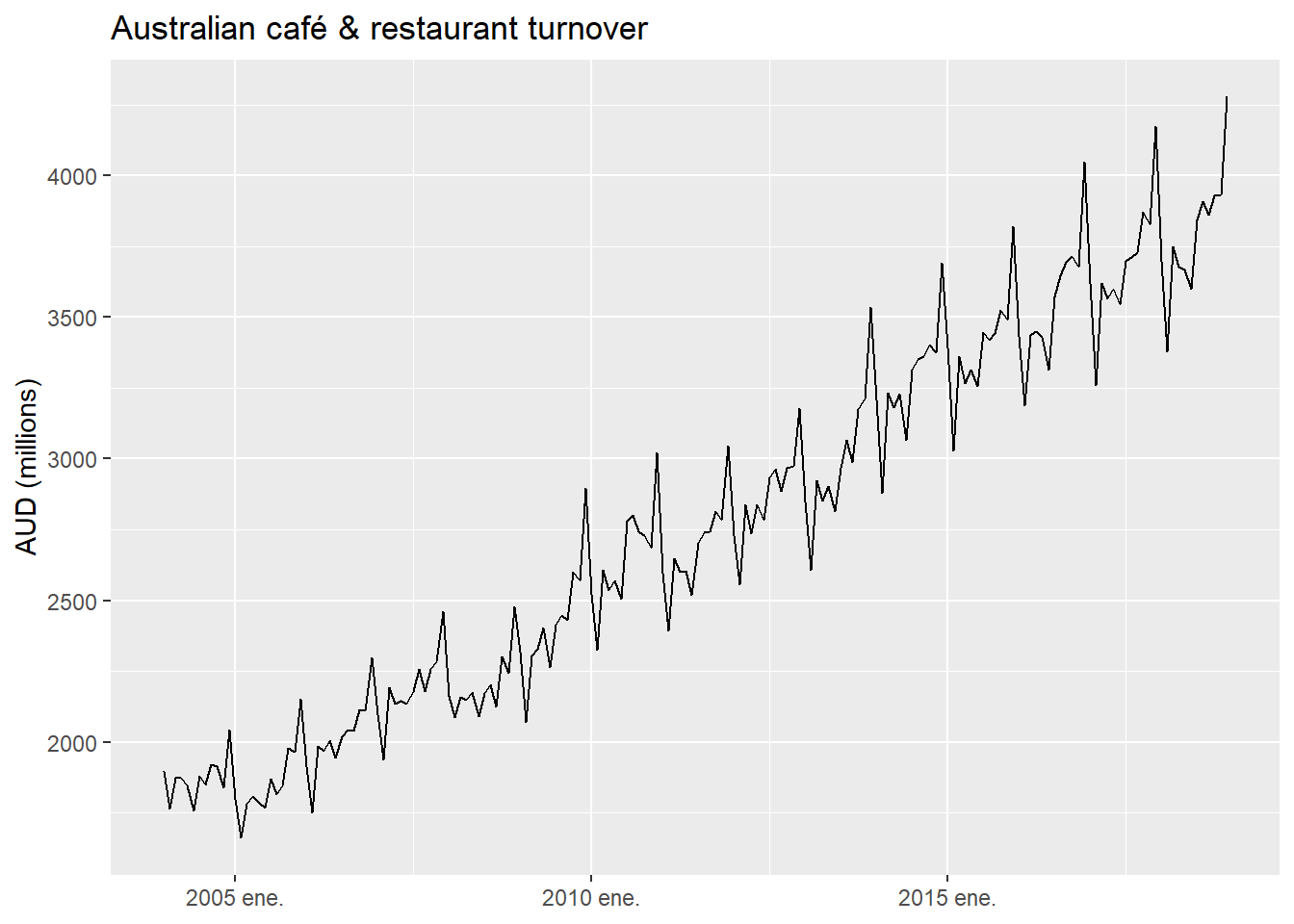

Monthly retail turnover for cafés and restaurants in Australia (2004–2018). A clean example of a monthly series with strong, stable seasonality — ideal for comparing values of K:

aus_cafe <- aus_retail |>

filter(

Industry == "Cafes, restaurants and takeaway food services",

year(Month) %in% 2004:2018

) |>

summarise(Turnover = sum(Turnover))

cafe_fit <- aus_cafe |>

model(

1 `K = 1` = ARIMA(log(Turnover) ~ fourier(K = 1) + PDQ(0, 0, 0)),

`K = 2` = ARIMA(log(Turnover) ~ fourier(K = 2) + PDQ(0, 0, 0)),

`K = 3` = ARIMA(log(Turnover) ~ fourier(K = 3) + PDQ(0, 0, 0)),

`K = 4` = ARIMA(log(Turnover) ~ fourier(K = 4) + PDQ(0, 0, 0)),

`K = 5` = ARIMA(log(Turnover) ~ fourier(K = 5) + PDQ(0, 0, 0)),

2 `K = 6` = ARIMA(log(Turnover) ~ fourier(K = 6) + PDQ(0, 0, 0))

)

glance(cafe_fit) |>

select(.model, AICc, BIC) |>

arrange(AICc)PDQ(0,0,0) suppresses seasonal ARIMA terms — Fourier handles the seasonality entirely.

The café example had one seasonal period (m = 12, monthly). But what if a series has more than one?

Consider electricity demand measured every 30 minutes:

How would you model this series with the tools you have now? What would happen if you tried season() dummies? What about Fourier terms — how many period arguments would you need, and how would you choose K for each one?

We will answer these questions in Module 4.1: Complex Seasonality.

The TSLM from Session 3.2 had one remaining weakness: autocorrelated residuals. Dynamic regression fixes this by letting the error term follow an ARIMA process instead of assuming white noise.

The model has two error terms: regression errors \eta_t (modeled by ARIMA) and innovations \varepsilon_t (white noise). Diagnose using \hat{\varepsilon}_t — the innovations, not the regression residuals.

When differencing is needed, a model in differences applies it to all variables simultaneously. When no differencing is needed, the model is fitted in levels. Stochastic trends are handled by differencing; deterministic trends by trend().

Forecasting still requires future values of the predictors — the same ex-ante / ex-post / scenario strategies from Session 3.2 apply. Lagged predictors are a practical advantage when the predictor is hard to forecast: the lag is already observed at forecast time.

Harmonic regression extends the framework to large or multiple seasonal periods using Fourier terms. Choose K by minimizing AIC_c.

| Session | Model | What was added |

|---|---|---|

| 3.1 | Practical issues | Transformations, outliers, cross-validation |

| 3.2 | TSLM | External predictors; \varepsilon_t white noise (required) |

| 3.3 | ARIMA(y ~ x) | Same predictors; \eta_t \sim ARIMA (relaxed) |

| 3.4 | Prophet | Automatic changepoints, complex seasonality |