ARIMA Models

Manual and Automatic Specification

In fable, ARIMA models are specified inside model() using the ARIMA() function. The order is controlled with pdq() for non-seasonal terms and PDQ() for seasonal terms. When pdq() is left unspecified, fable searches for the best order automatically.

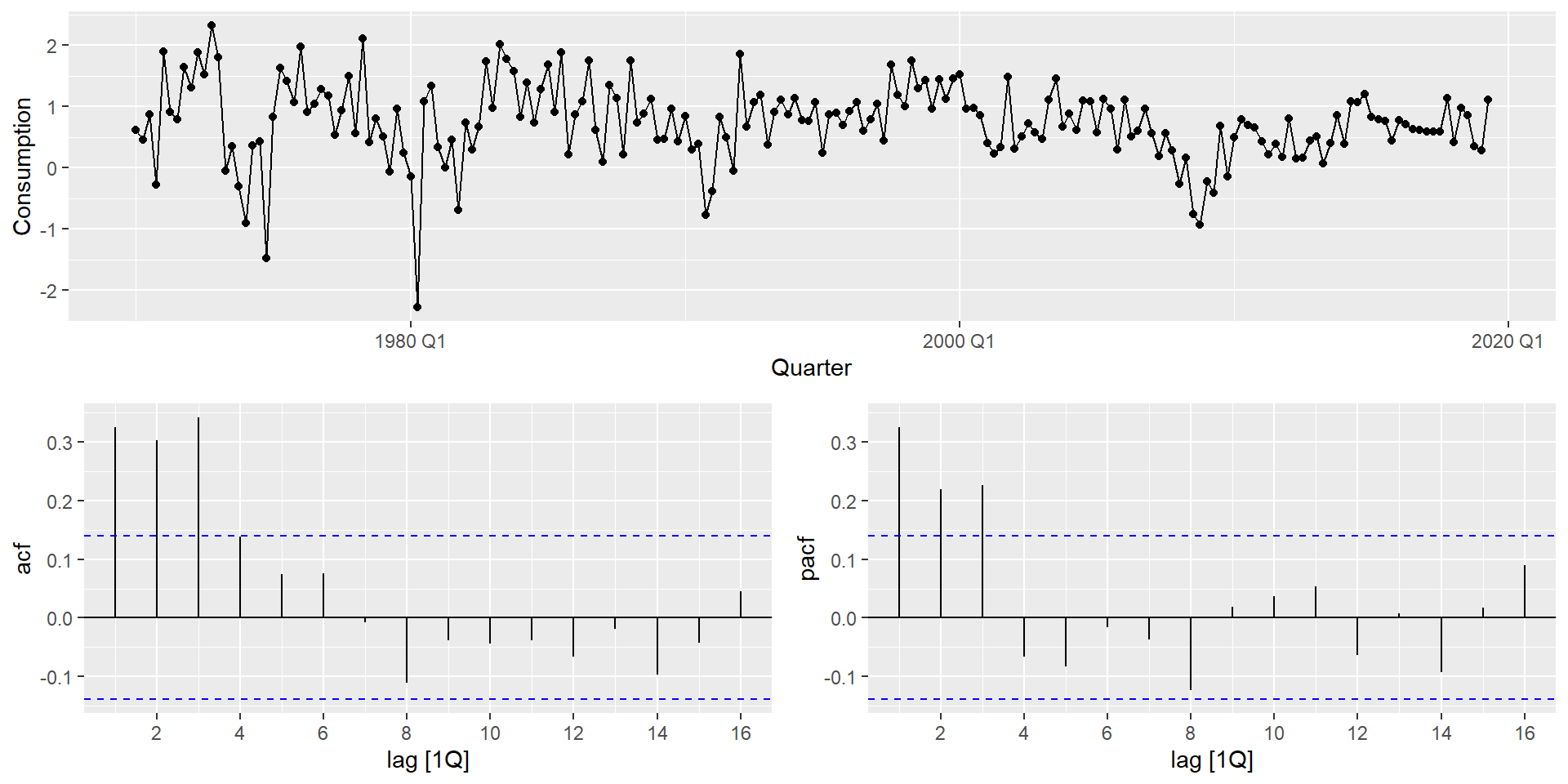

The series appears stationary (d = 0). The PACF shows significant spikes at lags 1–3, suggesting AR(3). We can fit this manually, compare it against automatic selection strategies, and let AIC_c arbitrate — all within a single mable:

us_change_fit <- us_change |>

model(

manual = ARIMA(Consumption ~ pdq(3, 0, 0) + PDQ(0, 0, 0)),

auto = ARIMA(Consumption ~ PDQ(0, 0, 0)),

semi_auto = ARIMA(Consumption ~ pdq(1:3, 0, 0:2) + PDQ(0, 0, 0)),

exhaustive = ARIMA(Consumption ~ PDQ(0, 0, 0),

stepwise = FALSE,

approximation = FALSE)

)

glance(us_change_fit) |>

arrange(AICc) |>

select(.model, AIC, AICc, BIC)- 1

-

Manual specification using

pdq().PDQ(0,0,0)explicitly forces a non-seasonal model. - 2

-

Leaving

pdq()unspecified triggers automatic stepwise order selection. - 3

- Evaluates all combinations of p \in \{1,2,3\} and q \in \{0,1,2\}, returns the lowest AIC_c.

- 4

-

stepwise = FALSEexplores all combinations rather than navigating step by step. - 5

-

approximation = FALSEuses exact likelihood. More accurate but slower on long series.

How does automatic selection work?

fable implements a stepwise search algorithm (Hyndman & Khandakar, 2008) that:

- Determines d using unit root tests.

- Starts from a simple model and navigates through the order space by comparing AIC_c values.

- Stops when no neighboring model improves AIC_c.

Important: this is a heuristic search — it does not evaluate all possible combinations. It is fast and usually good, but not guaranteed to find the global optimum.

For exploratory work, automatic selection is fine. For a final model, use stepwise = FALSE, approximation = FALSE and compare the result with your manually identified candidate.

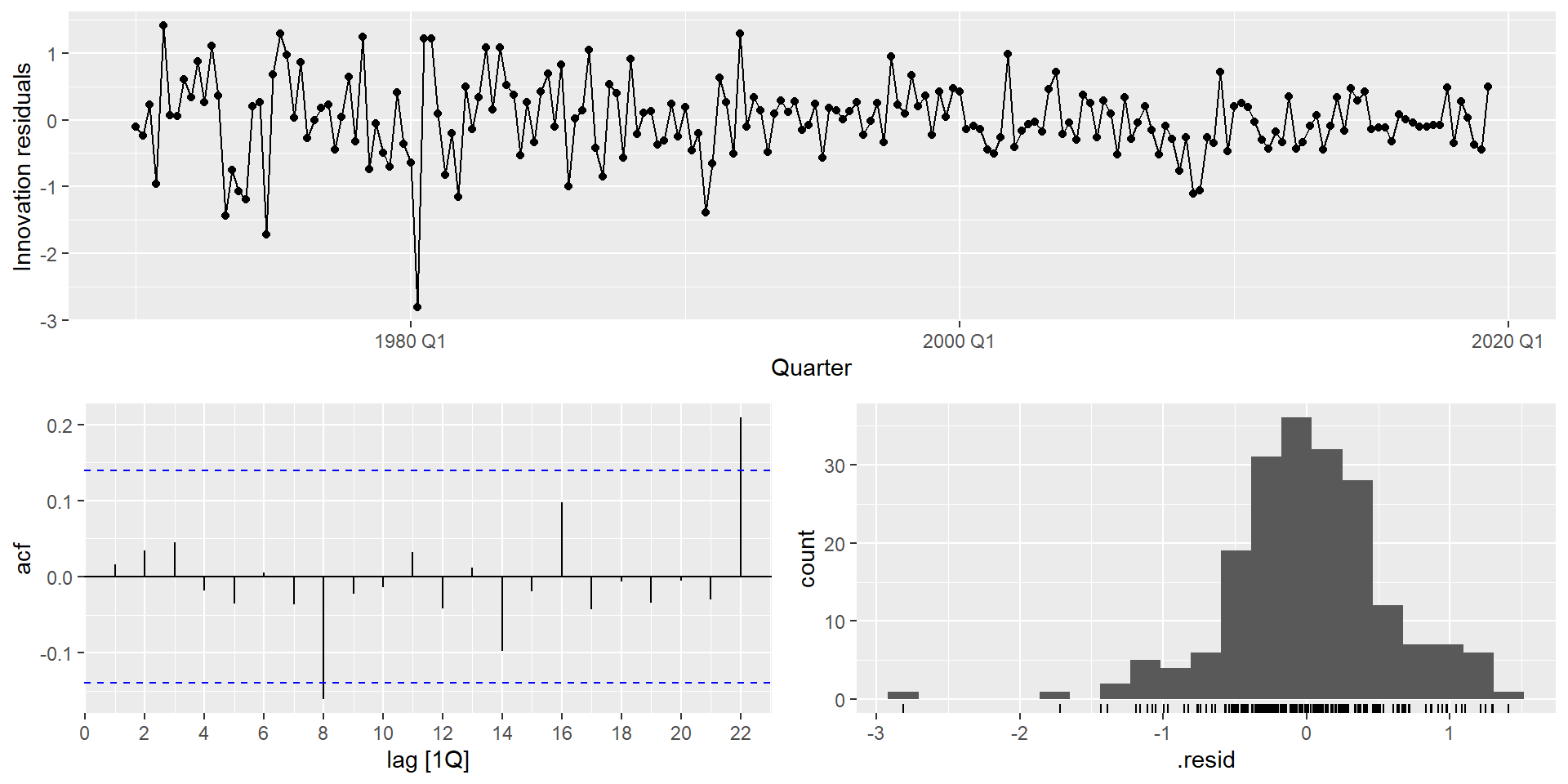

Residual Diagnostics

We have already used the Ljung-Box test to check residuals from benchmark models. When applying it to ARIMA models, there is one important adjustment: you must account for the degrees of freedom consumed by the estimated AR and MA parameters.

- 1

-

dofis computed dynamically as the number of estimated AR and MA coefficients, so it always matches the fitted model regardless of order.

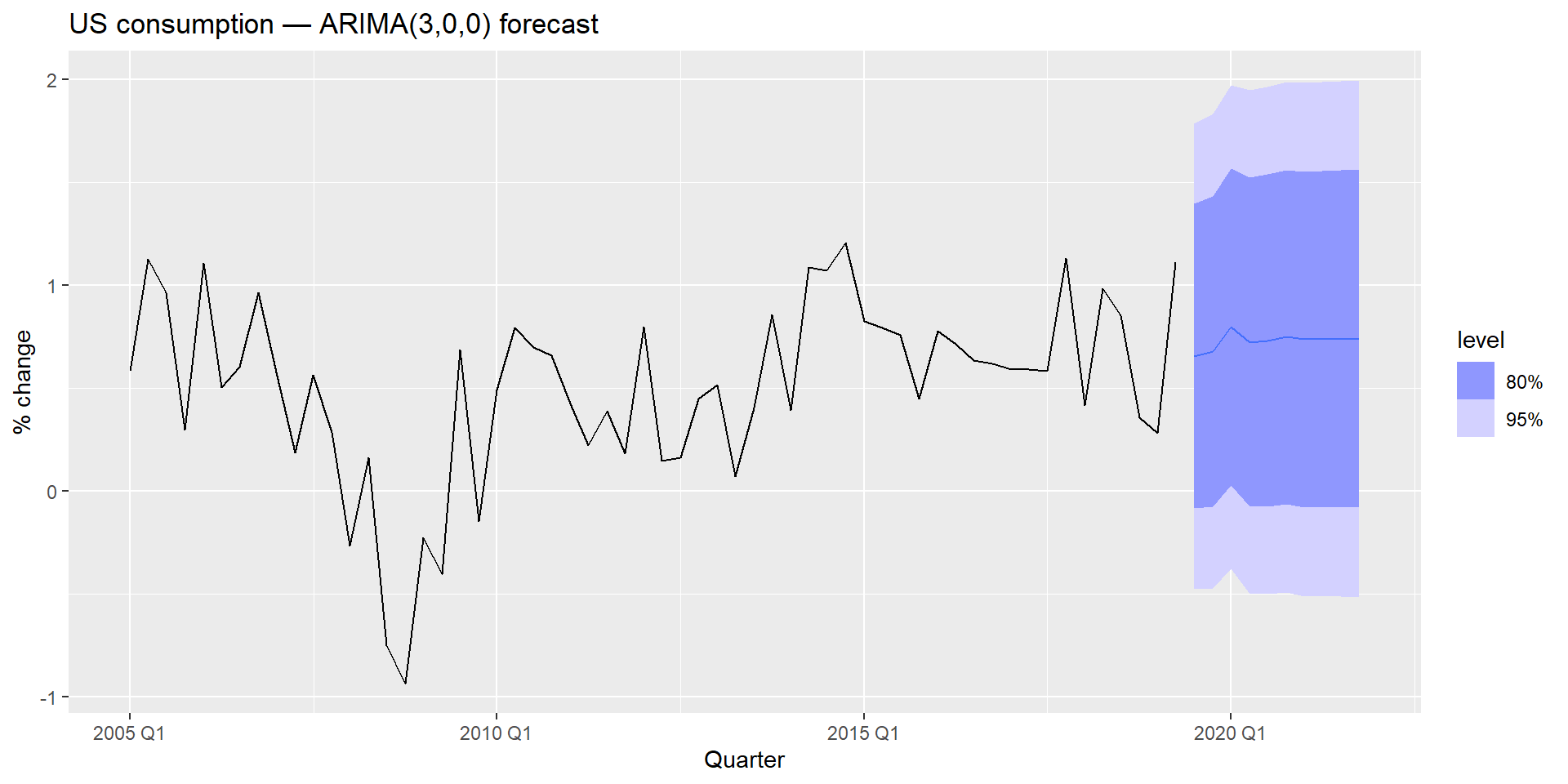

Forecasting

Once the model passes residual diagnostics, forecasting uses the same forecast() workflow as all other fable models:

Prediction intervals

ARIMA prediction intervals are derived analytically from the model’s MA representation. Their width grows with the forecast horizon, and grows faster as d increases — a direct consequence of accumulated uncertainty from differencing. For a random walk (d = 1), intervals widen at rate \sqrt{h}; for d = 2, they widen even faster.

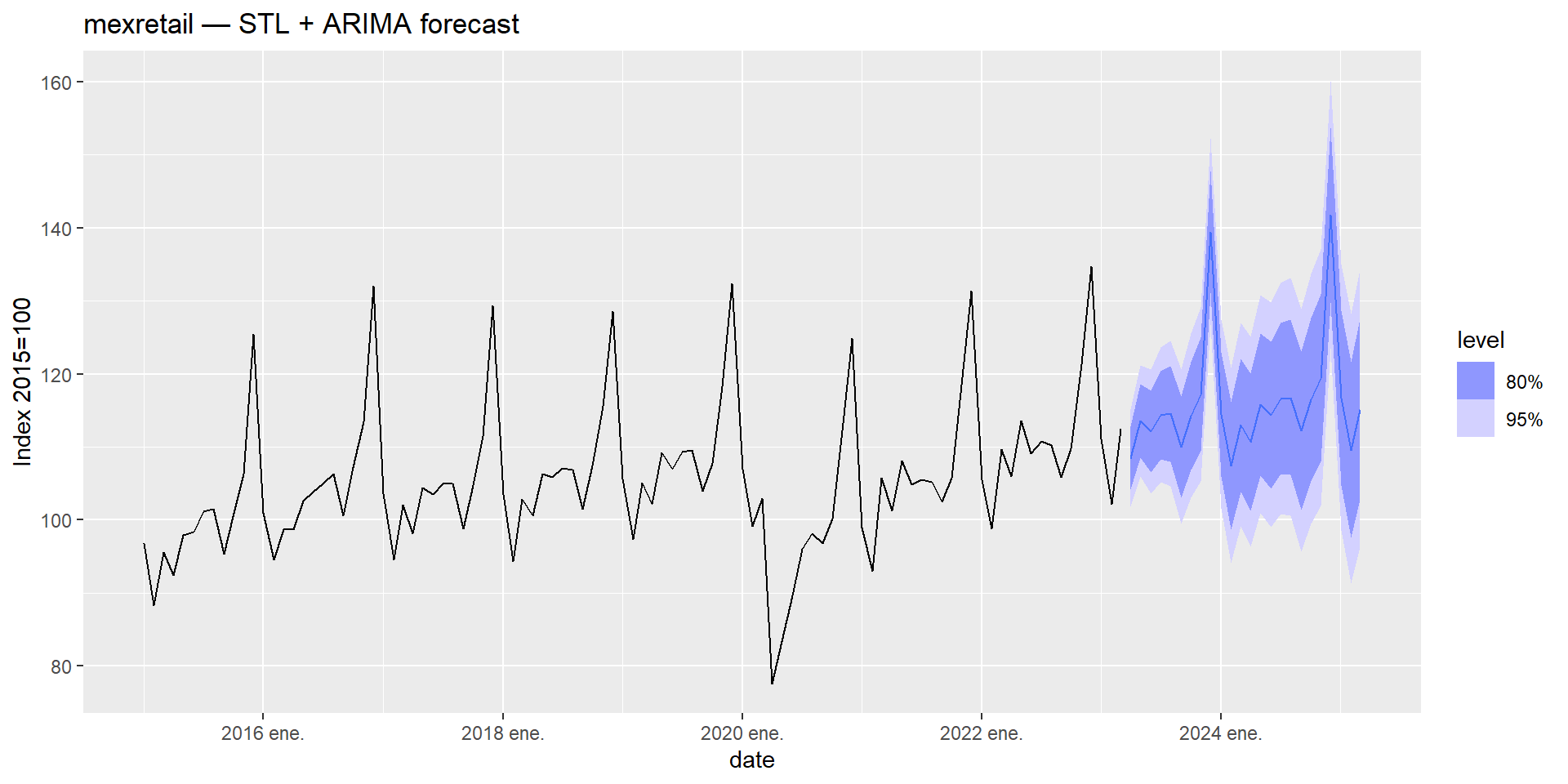

STL + ARIMA

mexretail is a monthly series with strong trend and seasonality. We already know how to handle it with STL decomposition. In Module 1 we combined STL with SNAIVE; in Module 2 we replaced SNAIVE with ETS. The natural next step is to replace it with ARIMA.

The idea is the same: use STL to handle the seasonal pattern, and let ARIMA model the trend-cycle on the seasonally adjusted series.

- 1

-

decomposition_model()combines a decomposition method with a model for one or more of its components. - 2

- STL decomposes the Box-Cox-transformed series. The seasonal component is handled implicitly by the decomposition.

- 3

-

ARIMA(season_adjust)fits an ARIMA model automatically to the seasonally adjusted component. The seasonal part is re-added when generating forecasts.

Series: y

Model: STL decomposition model

Transformation: box_cox(y, lambda)

Combination: season_adjust + season_year

========================================

Series: season_adjust

Model: ARIMA(0,1,1) w/ drift

Coefficients:

ma1 constant

-0.4500 0.1007

s.e. 0.0433 0.0491

sigma^2 estimated as 3.553: log likelihood=-914.69

AIC=1835.38 AICc=1835.43 BIC=1847.68

Series: season_year

Model: SNAIVE

sigma^2: 0

SARIMA for mexretail

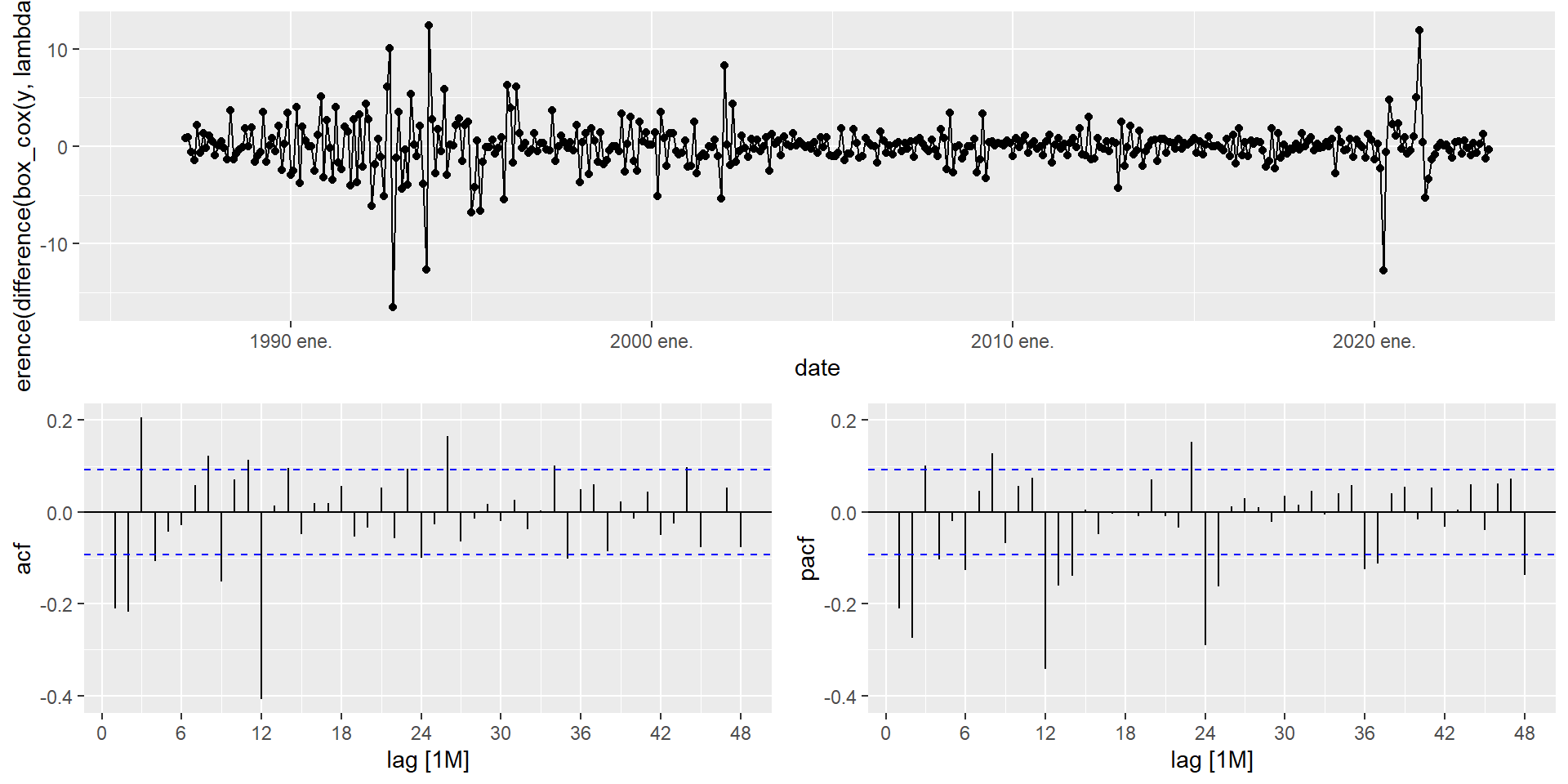

The stationarity protocol for mexretail established that we need D = 1 and d = 1 applied to the Box-Cox-transformed series. Let’s inspect the ACF/PACF to choose p, q, P, Q:

Reading the plot

- Non-seasonal lags (1–11):

- ACF: spike at lag 1, and up to lag 4 → try q = 1 up to q = 4.

- PACF: spikes at lags 1 and 2, borderline at lag 3 → try p = 2 or p = 3.

- Seasonal lags (12, 24, 36, 48):

- ACF: spike at lag 12, barely at lag 24 → try Q = 1 or Q = 2.

- PACF: spikes at lags 12, 24, and slightly at 36 and 48 → try P = 2, P = 3, or even P = 4.

When ACF/PACF suggest large orders, start simple

A strict reading of the ACF/PACF above could justify orders as large as AR(3), MA(4), SAR(4), SMA(2) — a model with over a dozen parameters. In practice, this is rarely a good starting point: high-order models are harder to estimate, more prone to overfitting, and — if specified manually — can fail to converge or return non-invertible roots altogether.

A better strategy: start with a parsimonious candidate like \text{ARIMA}(0,1,1)(0,1,1)_{12} or \text{ARIMA}(1,1,1)(1,1,1)_{12}, fit a few of the larger candidates suggested by the plots, and let AIC_c arbitrate. You will often find that the simpler model performs comparably or better — and it will always be more stable.

mexretail_fit_sarima <- mexretail |>

model(

sarima_011_110 = ARIMA(box_cox(y, lambda) ~

pdq(0, 1, 1) + PDQ(1, 1, 0)),

sarima_011_011 = ARIMA(box_cox(y, lambda) ~

pdq(0, 1, 1) + PDQ(0, 1, 1)),

sarima_auto = ARIMA(box_cox(y, lambda),

stepwise = FALSE,

approximation = FALSE)

)

glance(mexretail_fit_sarima) |>

arrange(AICc) |>

select(.model, AIC, AICc, BIC)- 1

- First candidate from ACF/PACF: non-seasonal MA(1), seasonal AR(1).

- 2

- Second candidate: non-seasonal MA(1), seasonal MA(1) — a very common structure for monthly economic data.

- 3

- Exhaustive automatic search for comparison.

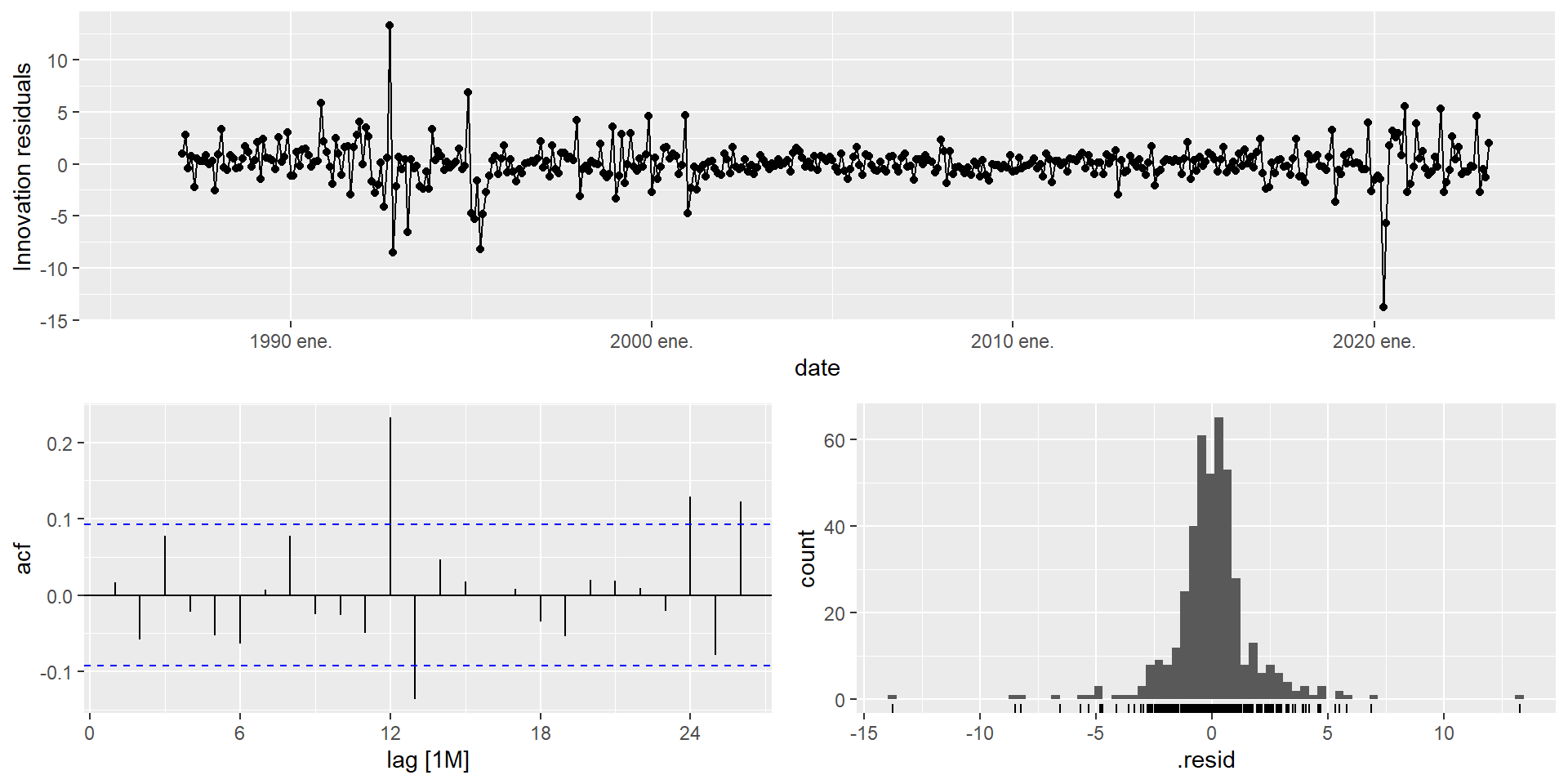

Series: y

Model: ARIMA(3,0,1)(0,1,2)[12] w/ drift

Transformation: box_cox(y, lambda)

Coefficients:

ar1 ar2 ar3 ma1 sma1 sma2 constant

0.2930 0.3114 0.3143 0.3671 -0.6877 -0.0956 0.0931

s.e. 0.1848 0.1454 0.0521 0.1975 0.0526 0.0534 0.0274

sigma^2 estimated as 3.303: log likelihood=-879.31

AIC=1774.62 AICc=1774.95 BIC=1807.22

- 1

-

dofis computed dynamically as p + q + P + Q for the fitted model, so it always reflects the actual order selected by the exhaustive search.

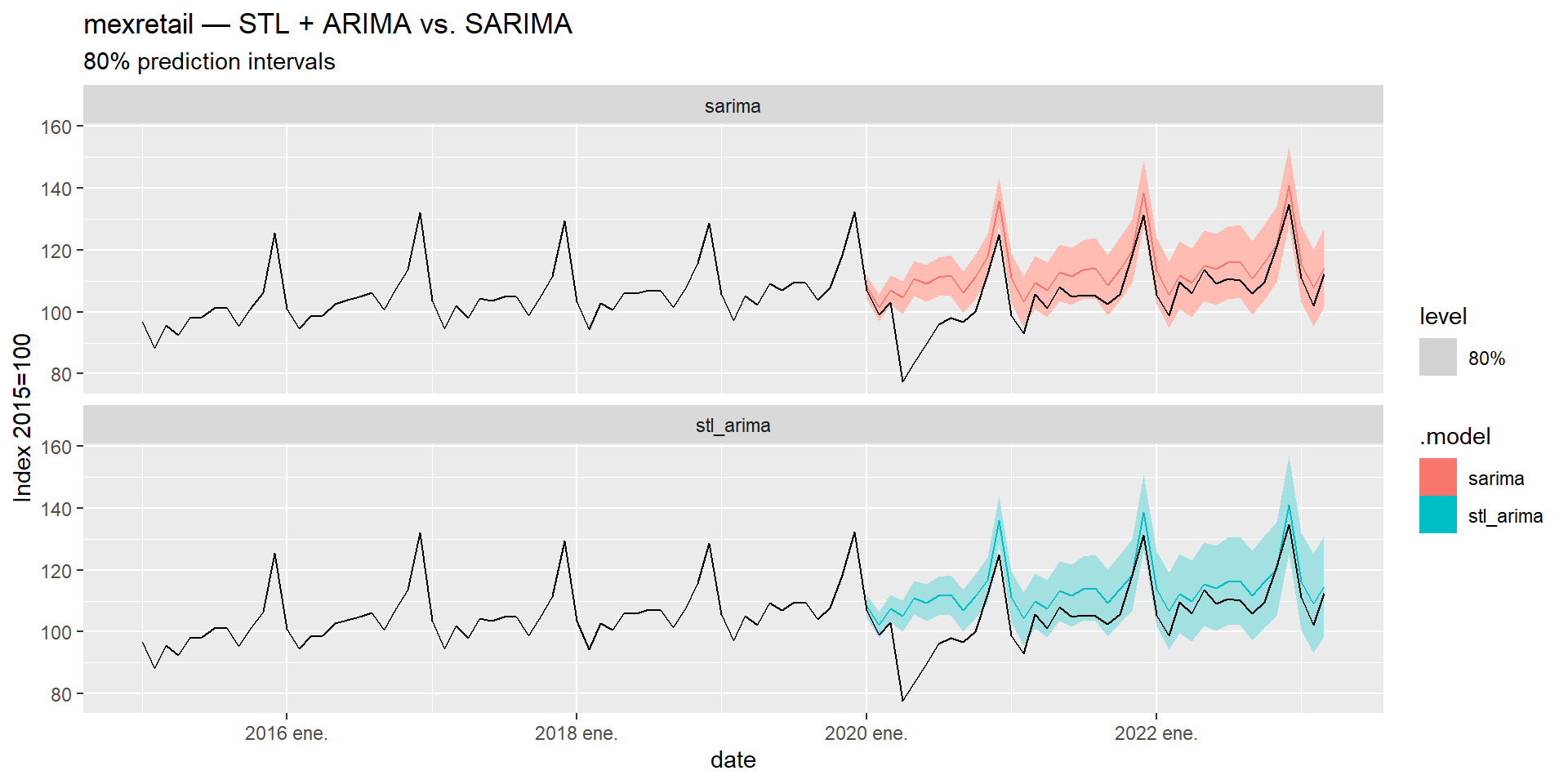

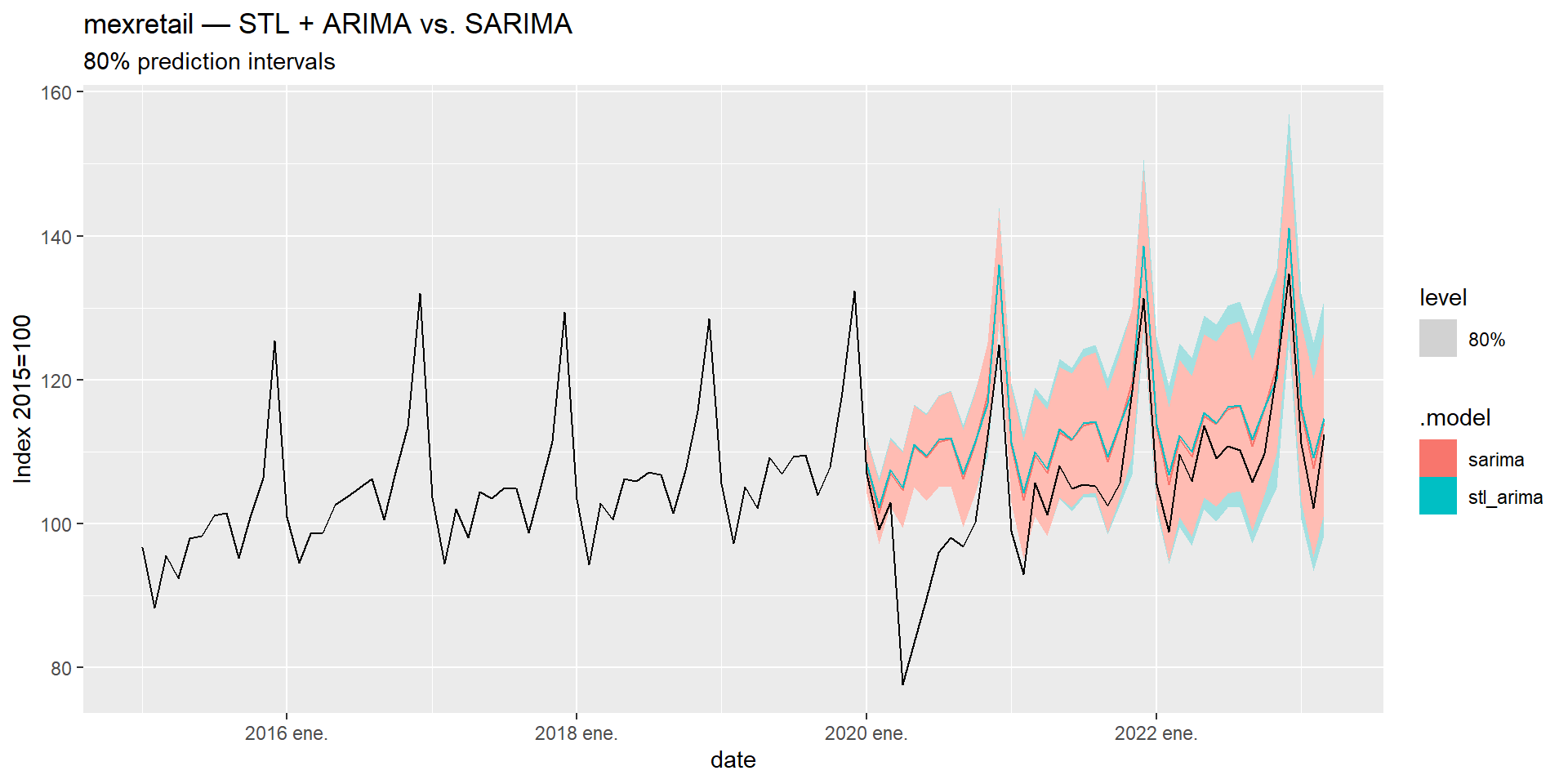

Comparing Both Strategies

Both approaches are valid for seasonal series. Let’s compare them on mexretail using a train/test split:

When to use which

| STL + ARIMA | SARIMA | |

|---|---|---|

| Seasonal pattern | Flexible — can change over time | Fixed structure |

| Outlier robustness | High (with robust = TRUE) |

Lower |

| Interpretability | Decomposition is visible | Single compact model |

| Multiple seasonality | Handles it naturally | Difficult |

| Parsimony | Two models in sequence | One unified model |

Neither approach dominates universally. Let the data and the accuracy metrics guide the choice.