Exponential smoothing

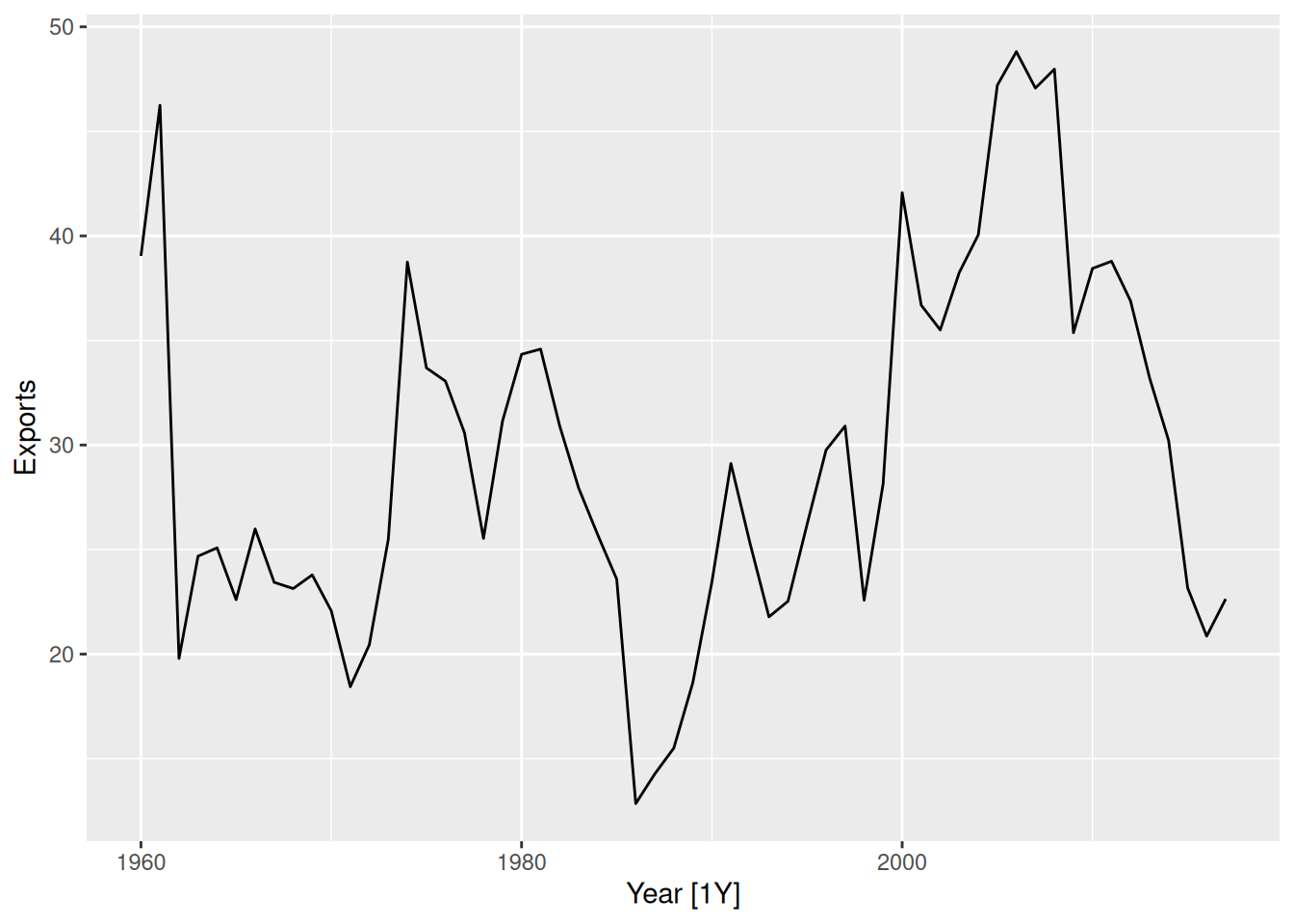

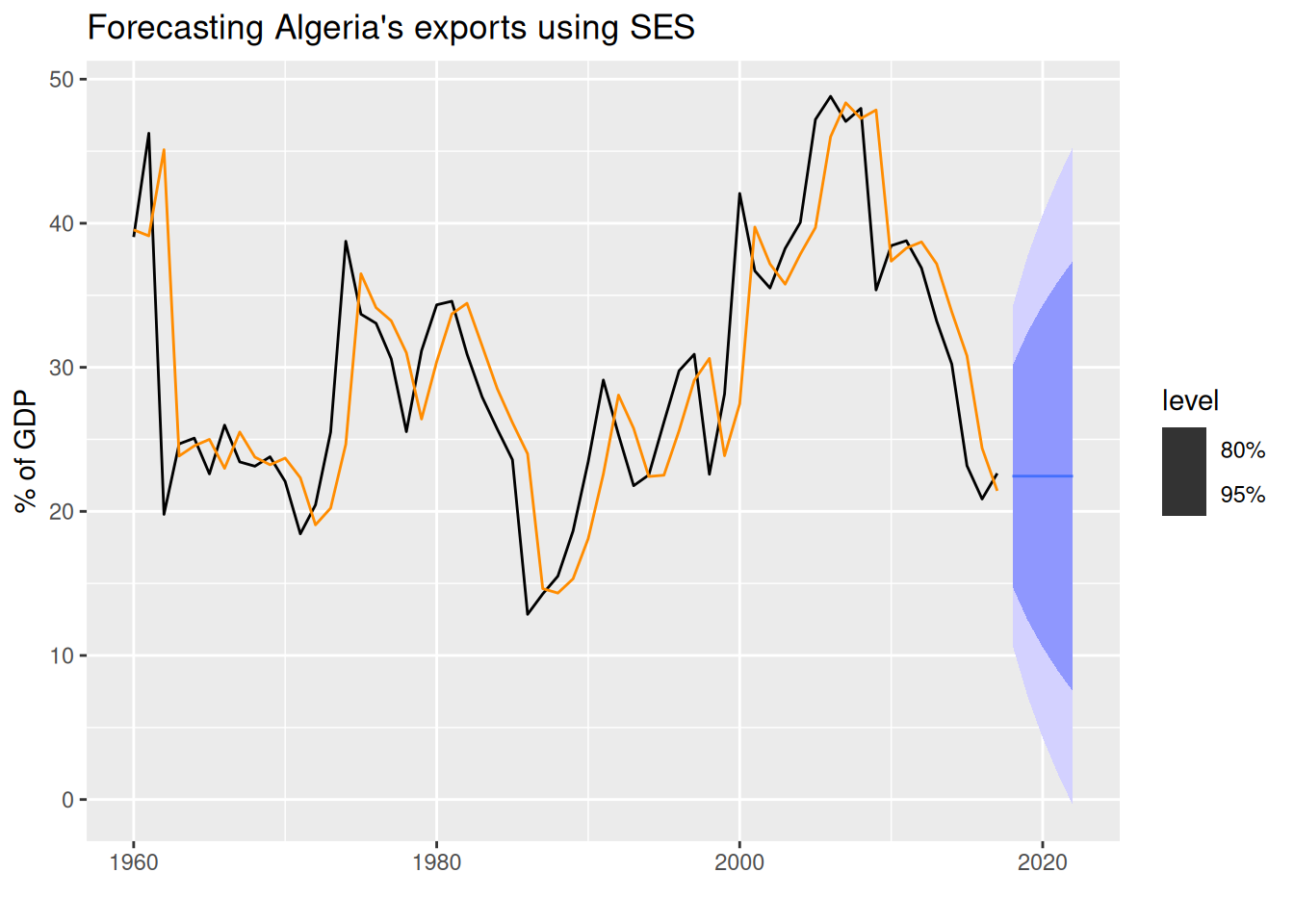

Example: Forecasting Algeria’s exports

- 1

-

We specify

trend("N")andseason("N")to indicate that we want a simple exponential smoothing (SES) model, which assumes no trend and no seasonality. The model will estimate the smoothing parameter \alpha automatically.

Obtaining the report() of a model

- 1

-

The

report()function allows us to see a model’s report (the time series modeled, the model used, the estimated parameters, and more). It needs a 1 \times 1 dimensionmable1.

Series: Exports

Model: ETS(A,N,N)

Smoothing parameters:

alpha = 0.8399875

Initial states:

l[0]

39.539

sigma^2: 35.6301

AIC AICc BIC

446.7154 447.1599 452.8968

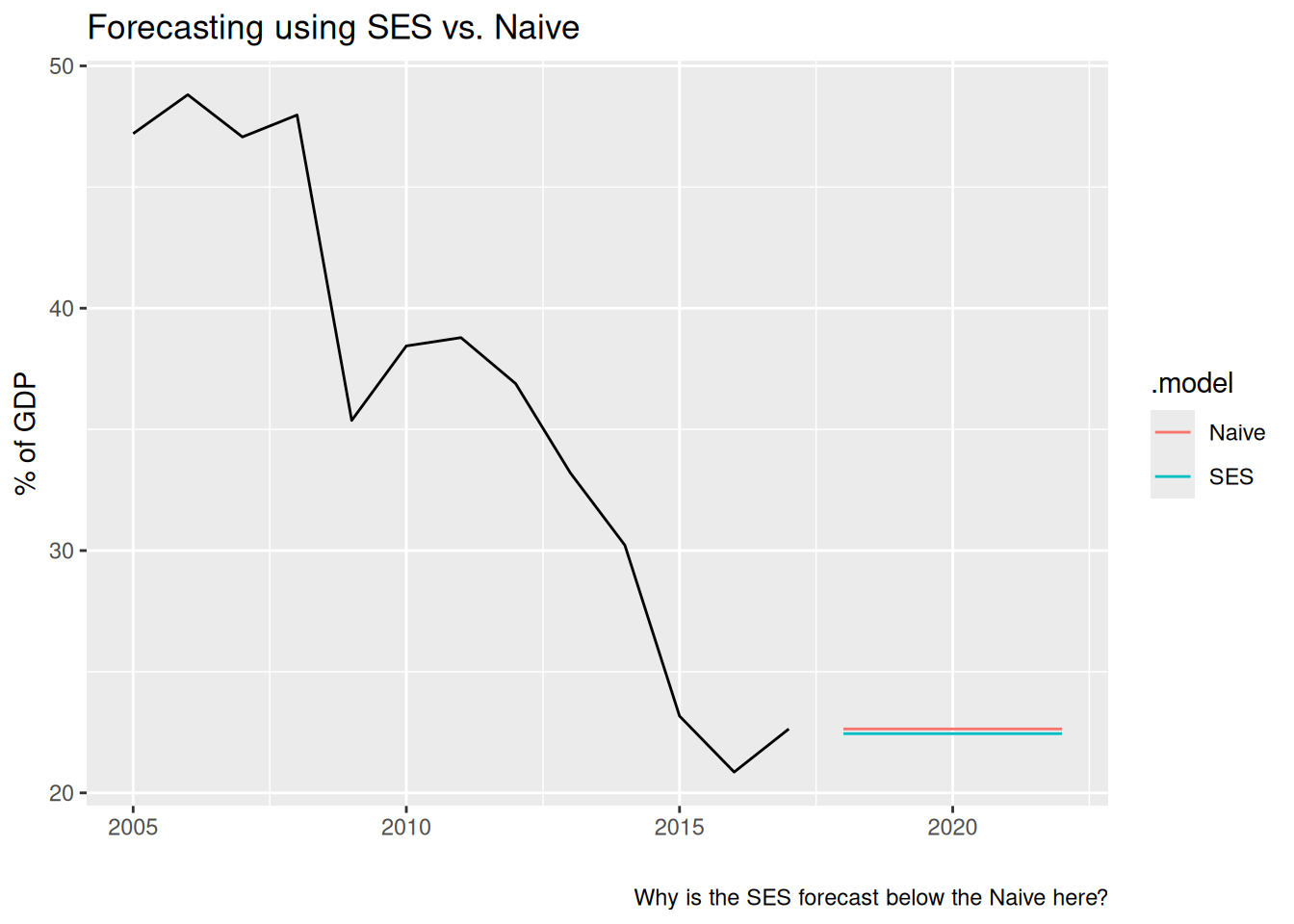

Comparing the SES and Naive forecasts:

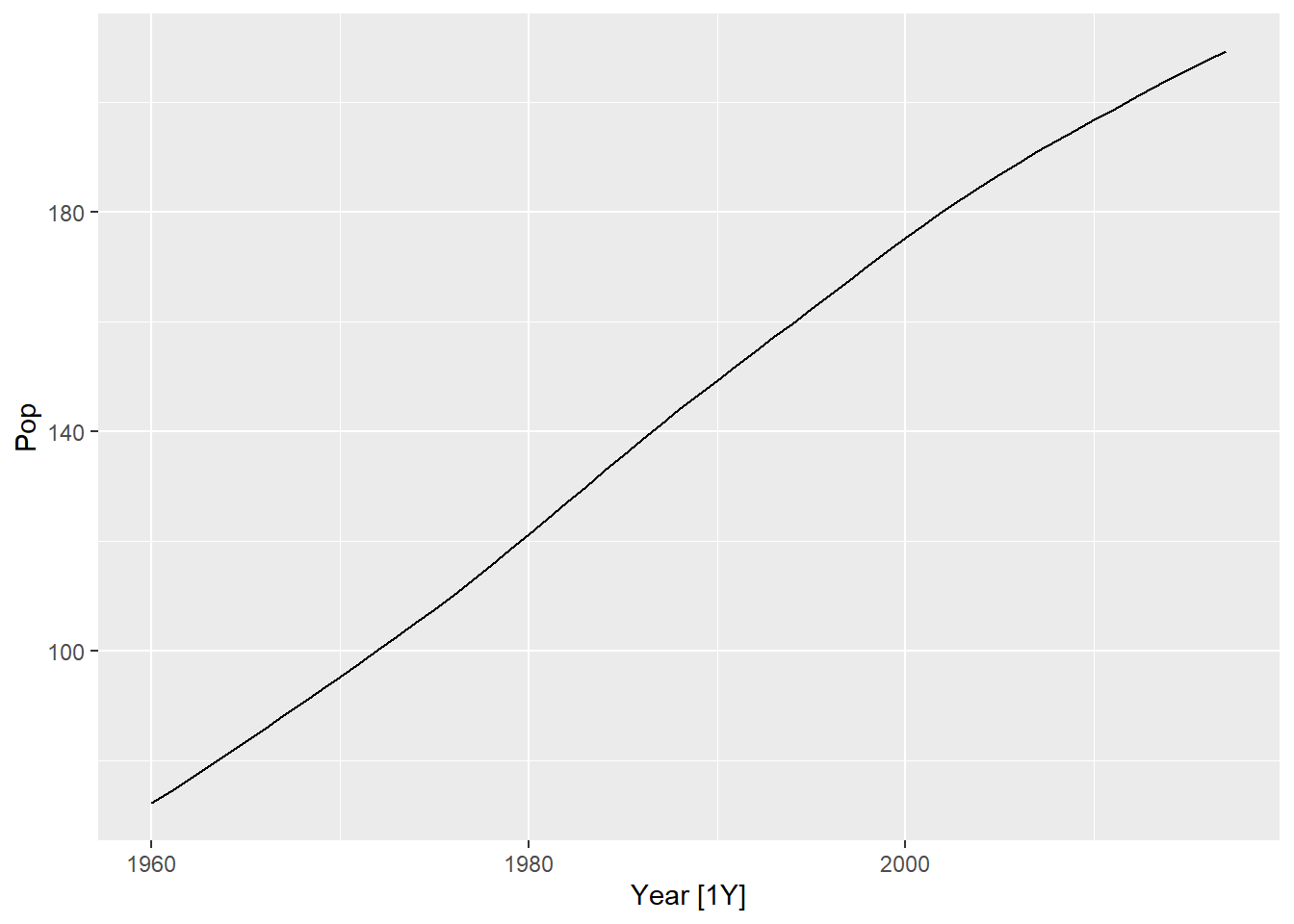

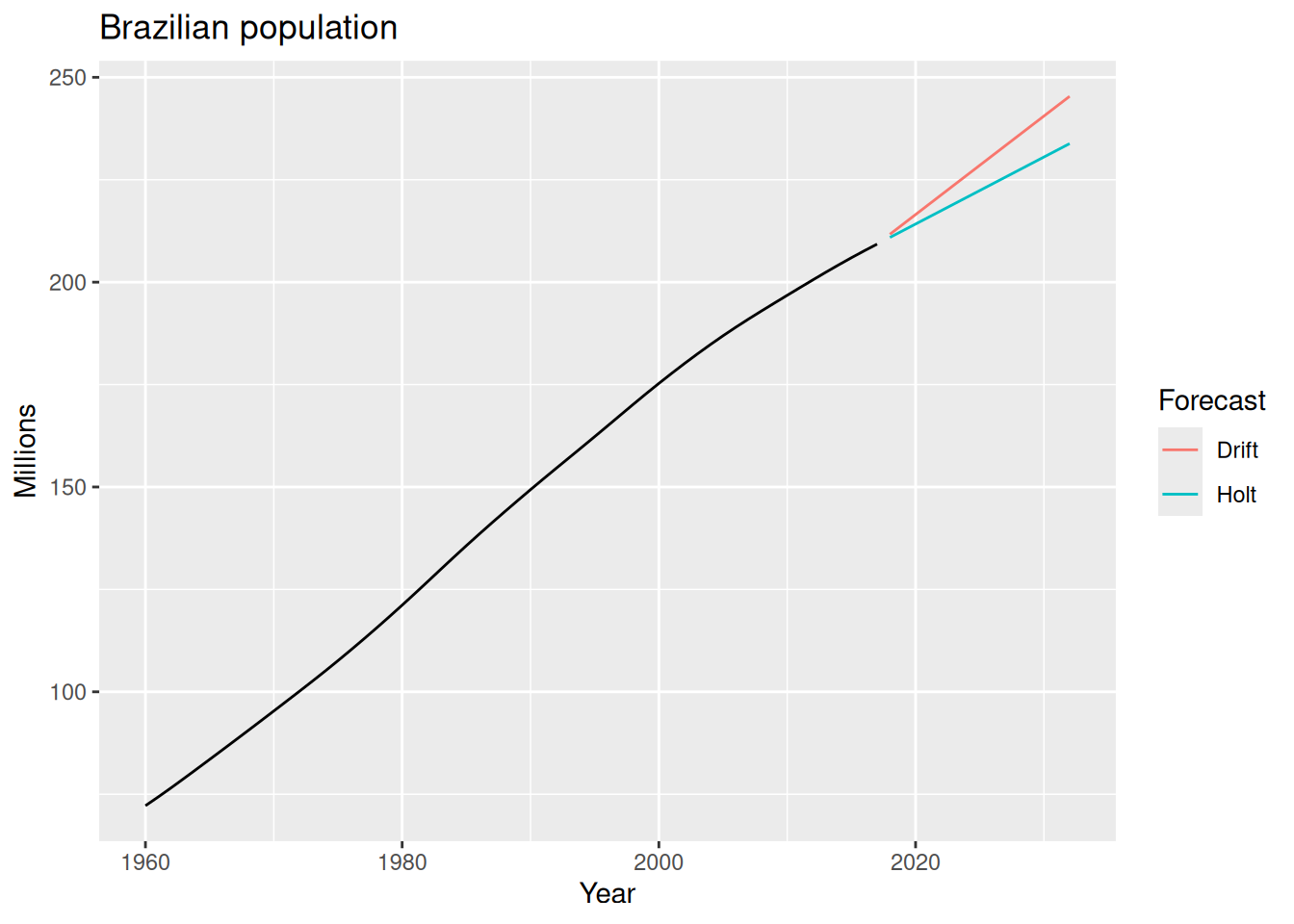

Example: Forecasting Brazil’s population

Example: Forecasting Brazil’s population

bra_fit <- bra_economy |>

model(

Holt = ETS(Pop ~ error("A") + trend("A") + season("N")),

Drift = RW(Pop ~ drift())

)

bra_fit |>

select(Holt) |>

report()

bra_fc <- bra_fit |>

forecast(h = 15)

bra_fc |>

autoplot(bra_economy, level = NULL) +

labs(title = "Brazilian population",

y = "Millions") +

guides(colour = guide_legend(title = "Forecast"))- 1

-

We specify

trend("A")to indicate that we want a linear trend. The model will estimate the smoothing parameters \alpha and \beta^* automatically.

Series: Pop

Model: ETS(A,A,N)

Smoothing parameters:

alpha = 0.9999

beta = 0.9998999

Initial states:

l[0] b[0]

70.06297 2.132884

sigma^2: 0.0021

AIC AICc BIC

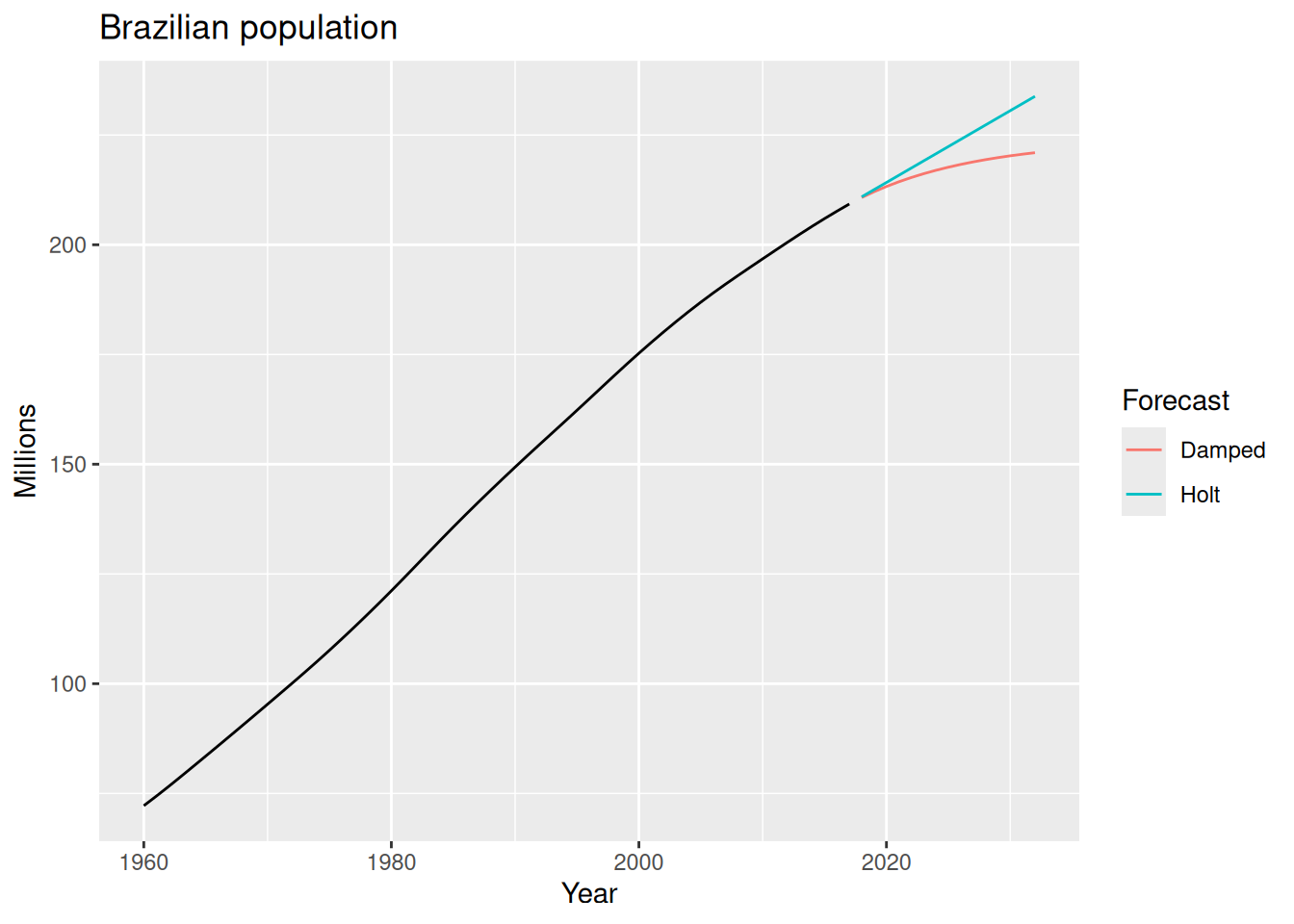

-115.2553 -114.1014 -104.9531 Example: Forecasting Brazil’s population (continued)

bra_economy |>

model(

Holt = ETS(Pop ~ error("A") + trend("A") + season("N")),

Damped = ETS(Pop ~ error("A") + trend("Ad", phi = 0.9) + season("N"))

) |>

forecast(h = 15) |>

autoplot(bra_economy, level = NULL) +

labs(title = "Brazilian population",

y = "Millions") +

guides(colour = guide_legend(title = "Forecast"))- 1

-

We specify

trend("Ad")to indicate that we want a damped trend, andphi = 0.9sets the damping parameter to 0.9. We could also let the model estimate \phi automatically by omitting thephiargument.

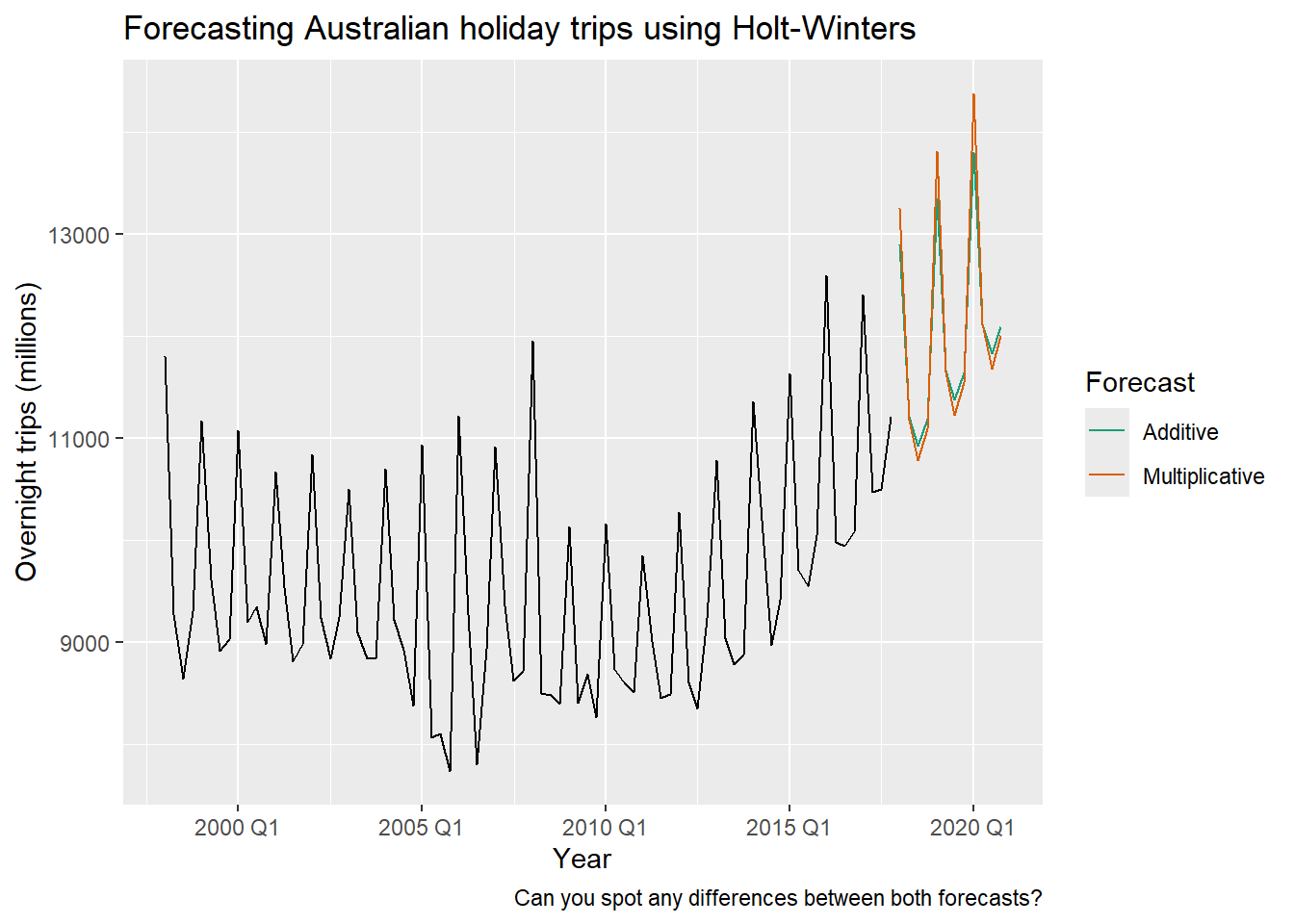

Example: Forecasting Australian holiday trips

Example: Forecasting Australian holiday trips

aus_fc |>

autoplot(aus_holidays, level = NULL) + xlab("Year") +

labs(

title = "Forecasting Australian holiday trips using Holt-Winters",

y = "Overnight trips (millions)",

caption = "Can you spot any differences between both forecasts?"

) +

scale_color_brewer(type = "qual", palette = "Dark2") +

guides(colour = guide_legend(title = "Forecast"))

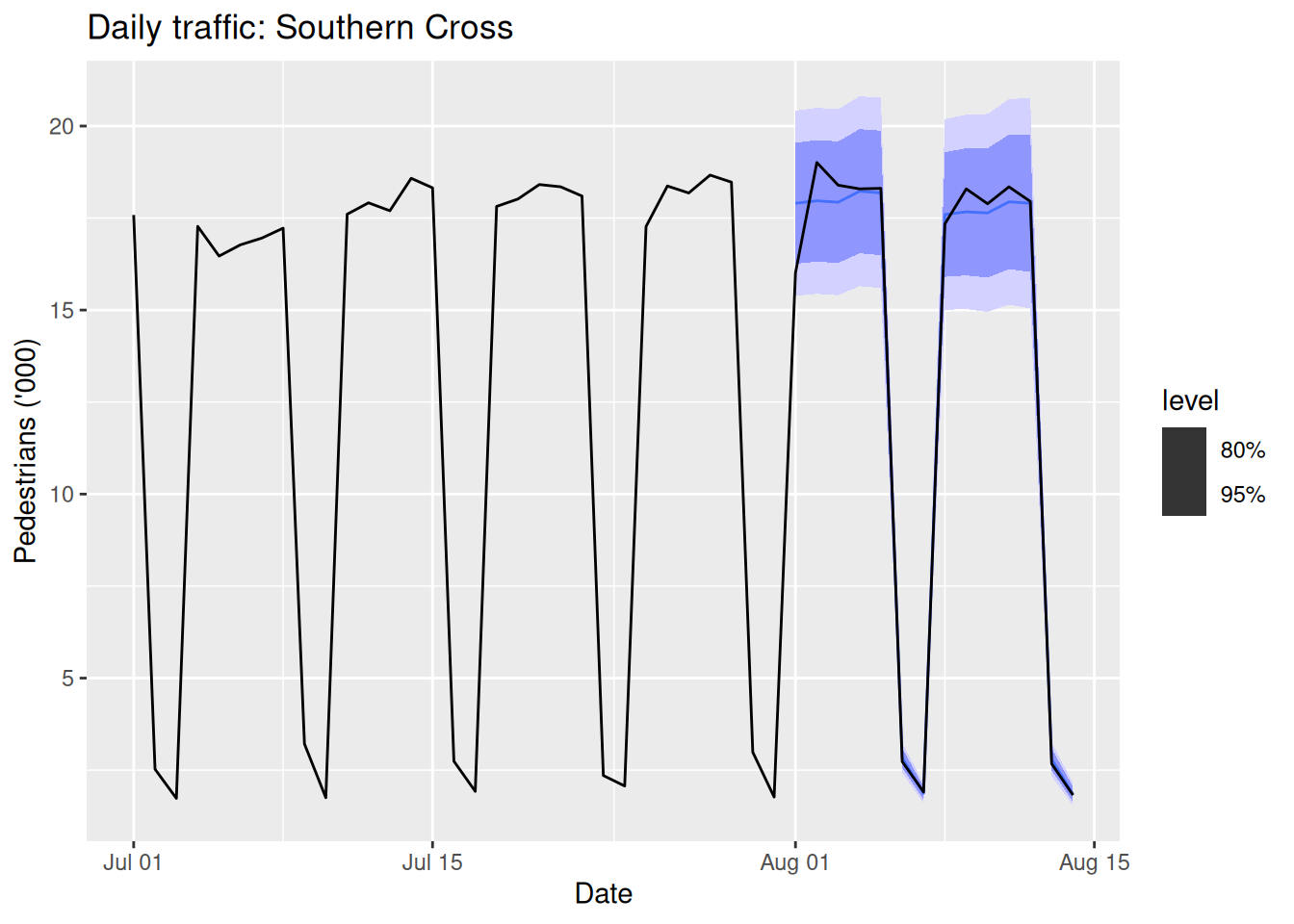

Example: Forecasting daily pedestrian traffic

sth_cross_ped <- pedestrian |>

filter(Date >= "2016-07-01",

Sensor == "Southern Cross Station") |>

index_by(Date) |>

summarise(Count = sum(Count)/1000)

sth_cross_ped |>

filter(Date <= "2016-07-31") |>

model(

hw = ETS(Count ~ error("M") + trend("Ad") + season("M"))

) |>

forecast(h = "2 weeks") |>

autoplot(sth_cross_ped |> filter(Date <= "2016-08-14")) +

labs(title = "Daily traffic: Southern Cross",

y="Pedestrians ('000)")

The setup ETS(y ~ error("M") + trend("Ad") + season("M")) is often a robust choice for seasonal data with trend.

Footnotes

(i.e., a

mablecontaining only one model and one time series.)In practice, we restrict 0.8 \leq \phi \leq 0.98 because the damping effect would be too great for smaller values than 0.8 and almost non distinguishable from a linear trend for greater values than 0.98.

e.g., m=4 for quarterly data, m=12 for monthly data, …

as the decomposition method

for the seasonally adjusted series

for the seasonal component